Ridges and valleys of the Zagros Mountains in southern Iran. Photography: NASA.

Frontier exploration – Are we seeing a revival?

On the back of numerous announcements, press releases and social media posts, there seems to be momentum behind a return of frontier exploration. More acreage is being awarded, and companies are more vocal about their exploration portfolio again. But at the same time, it is good to be aware that if the tide indeed turns, the inflection point is still positioned at a genuine low in the overall market. The number of exploration wells has been very depressed over the past few years. A look at how the seismic acquisition sector has fared also demonstrates the impact that this lull in activity has had on the service sector as a whole. In this article, I will try to grasp this exploration revival a little more through conversations with experts on the matter, combined with some personal observations. But before we get to the main topic of the article, let’s take a look at a very recent announcement in the exploration arena that has rocked the boat

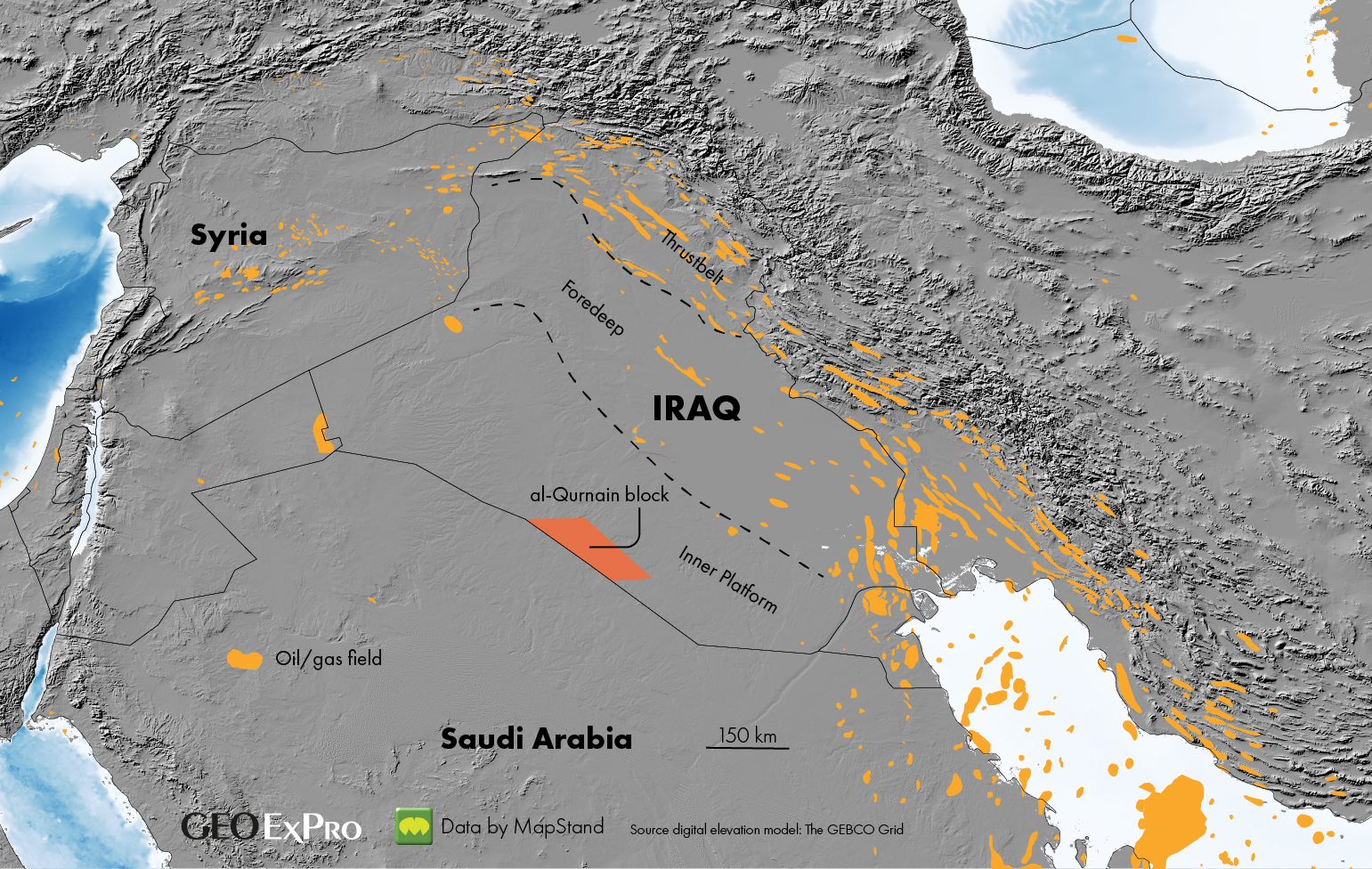

As I started writing this story, a contact in Iraq messaged me about a new well recently completed in the west of the country, near the border with Saudi Arabia. It is a well that was drilled by Zhenhua Oil, a state-owned Chinese company, under the local subsidiary name Qurnain Petroleum. This well, which was mistakenly named Shams-11 instead of Shams-1, made a discovery of around 8 Bbbl of oil.

Of course, it is early days, and as Jonathan Brown voiced as a response to our LinkedIn post dedicated to the discovery, it is too early to make such a detailed estimate of the field’s size after drilling just one well. That is a valid remark indeed. But still, even if this discovery turns out to be smaller, it is still something to take note of.

Why is that?

It is because of the location of the discovery in the western part of Iraq. When looking at the map, the location of the licence where the discovery was made is far away from the classic fold and thrust belt and foreland petroleum plays that characterise the northern and eastern parts of the country.

Instead, the Qurnain discovery lies in the area that is interpreted as the “Stable Platform”, or the Tethys passive margin. Hardly any oil fields have so far been found in this structural domain in Iraq. That’s why this find can be regarded as a play opener. At least for the country of Iraq, because in neighbouring Saudi Arabia, the play is well known.

Mohammed Al-Mahmoud commented on LinkedIn: “Basin-wise, the discovery location is similar to the Jurassic oil fields in Saudi Arabia. It is on the western flank of the Mesopotamian basin. The Saudi major oil fields are on the western flank of the Arabian basin. On a more regional perspective, the Mesopotamian and Arabian basins are, geologically, not segregated from each other. Likewise, their western flanks are geologically connected. Hydrogeological studies in both Saudi Arabia and Iraq indicate hydraulic continuity of the rock units, which means that western Iraq and northern Saudi Arabia are likely one regional hydrocarbon play.”

Have the Chinese unlocked a major new oil province? This is clearly something that we need to keep a close eye on. And I’m sure that all the international majors do too. Especially when you realise that the largest discovery of 2025 was made in Iraq, in the East Baghdad field – a supposedly 2 Bbbl find – also made by Zhenhua Oil.

All this is worth mentioning because it seems to be the Chinese who prove the volumes that the Western IOCs are craving for. And where one can argue that the East Baghdad find is very near-field, the Qurnain discovery is surely in a new play, at least for Iraq. The Chinese have therefore shown that more frontier exploration is also part of their playbook. That then begs the question: when do we see the IOC’s make discoveries of the same nature again?

Is the world on the cusp of an exploration revival?

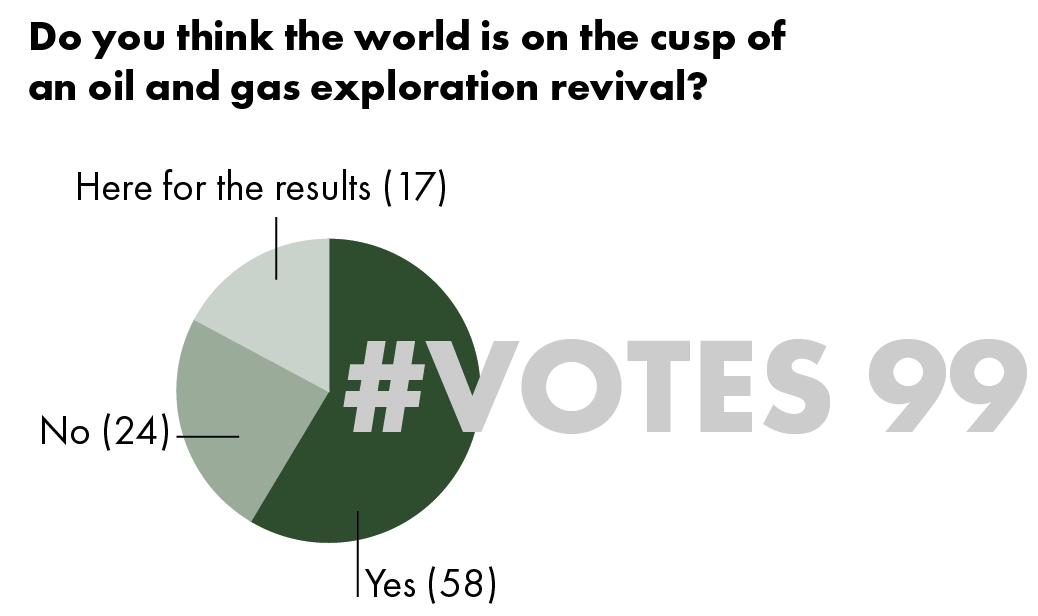

Let’s dive into this question a little more. First, we asked our followers via a LinkedIn poll. As can be seen in the graphic here, most of those who cast a vote do indeed believe that something is happening in the exploration space. As ever, there is a good number of folk who are just keen to see the statistics without revealing what they think. However, the poll still serves its purpose.

I also asked a number of people from different parts of the world this question personally, in an attempt to gain a more nuanced understanding of what is happening in frontier exploration.

Simon Molyneux, who runs an E&P consultancy company in Perth, Australia, writes: “We’ve seen signs over the last 12 months or more that exploration is returning. We feel the driving force behind this is a realisation amongst corporates and private capital that new sources of oil and gas are needed over the long term to meet societies’ growth in energy demand and replace declining legacy sources of oil and gas.”

Graeme Bagley from Westwood Global Energy in London adds that over the last five years globally the industry has only found ~11 % of what has been produced by conventional high impact exploration, whilst demand for hydrocarbons continues to grow – currently. Whilst several of the large IOCs have only found less than 25 % of what they have produced.

From Houston, Luis Carlos Carvajal Arenas writes: “I have had the chance to be involved with global exploration for six years now, and I can say that I see an upturn in exploration at multiple levels. The world changed after COVID by accelerating the Energy Transition. Many companies decided to defund traditional energy and move towards New Energy projects. However, many energy transition pioneers are now stepping back because they faced the crude reality; many of the new energy projects delivered low ROIs or the projects were negative.”

But apart from the observation that there is a desire to ramp up exploration activity, are there concrete examples of this really happening?

Graeme does not fully align with the narrative. “Whilst there is a lot of talk of an exploration revival, it has not translated into more spending or more wells being drilled. What we are seeing currently is more like a land-grab,” he says. “Lots of new licences are being taken up, but generally at low commitment levels.” Luis Carlos agrees with that. The new frontier licences picked up are what is called “technical evaluation agreements” or “recognition agreements”, which can be shifted into exploration agreements if the company finds something encouraging to test,” he writes.

Andrew Latham from Wood Mackenzie describes it in this way: “There’s a lot more noise around exploration, but it’s not yet much more than that. The majors and other big explorers are several years into a high-impact acreage reload, but much of this new acreage represents relatively low-cost options, with minimal signature bonuses and few firm drilling commitments. Most has yet to be drilled and is still held with high operator working interests that may need to be farmed down first. That said, we are seeing a bit of a trend of more big exploration wells being drilled at 100 % equity or some-thing close.”

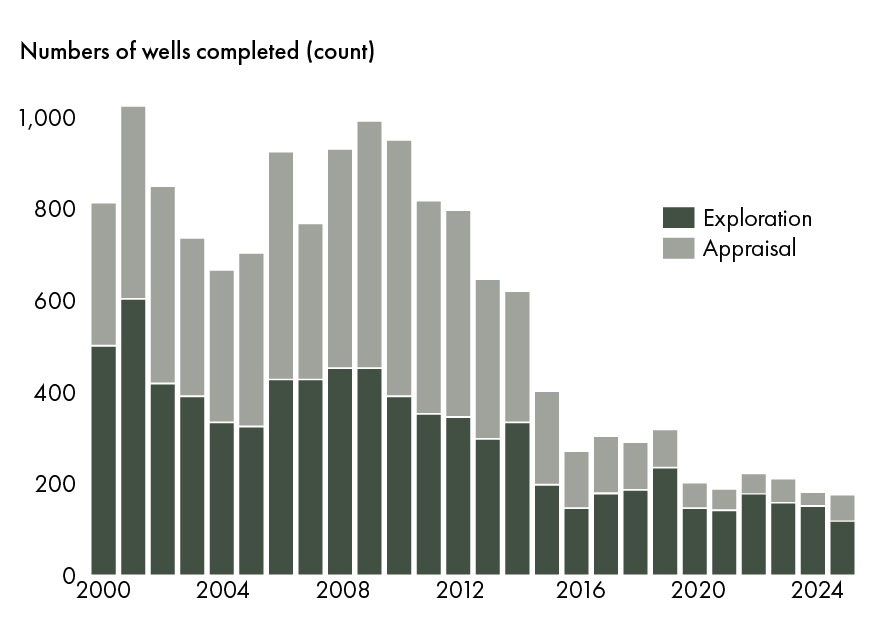

The lack of genuine commitment to wells is also reflected in the number of high-impact exploration wells drilled. 2025 saw the fewest high-impact wells completed since 2015, with no clear upturn in sight. “Maybe we will see that in two or three years,” Graeme says.

There’s a lot more noise around exploration, but it’s not yet much more than that – Andrew Latham

Simon adds: “There is no wild exploration spirit yet. Exploration spend is still very small compared to the heady times of the late 2000’s and early 2010’s. Opportunities have to be compellingly large and de-risked, with substantial acreage positions that can be executed at scale and pace, ideally with follow‑up. But much of the world is not like Guyana. Available positions are fragmented, permitting is challenging and modern data is not readily available. Innovative players will navigate around these challenges.”

Graeme still sees companies prioritising on shareholder returns and debt reduction over investment in exploration, resulting in capital discipline that does not necessarily align with a more bullish exploration strategy. The opportunities for exploration success at scale are becoming more limited, and companies are also looking to develop discoveries that have sat on the shelf for a long time,” he says. bp’s Tiber and Kaskida developments in the Gulf of Mexico are good examples of this.

Joe Versfelt from Houston, says that many small to medium-sized American companies have significant debt to service versus cash flow and shareholder dividend expectations to meet. “I think ILX will still dominate, combined with a robust portfolio optimisation – especially in the Lower 48 US unconven-tional space.”

Another example of ways to ramp up production for which no exploration drilling is required is the decision by ConocoPhillips and partners to re-open three formerly abandoned gas fields in the Ekofisk area in the Norwegian Southern North Sea, as demand for gas in Germany and the UK remains strong. Luis Carlos adds that Egypt is also focusing on ILX projects in the Nile Basin as the Egyptian market requires new reserves for internal consumption quickly.

In other words, based on these conversations, there is surely a first movement into the exploration space, but there is equally a cautious approach without too many commitments.

WHO’S INVESTING IN PROJECTS THAT ONLY START GENERATING CASH IN 20 YEARS?

One reason why the industry may be slow or indecisive when it comes to drilling frontier wells is the prospect of a long lead time between discovery and first oil. Earlier this year, I was in Houston before the conference I was attending kicked off. An ideal moment to meet with some industry veterans. I met one of them for a beer to catch up on what he saw happening in the exploration realm. One of the main points he made was that the industry is no longer interested in projects that have a twenty-year gap between identifying a prospect and the start of production. “My father had to process a couple of 2D lines for Conoco in the 1980s,” he said, “and it turned out to contain a whopping prospect.” But it took a sale to another operator and more than twenty years before the first oil was achieved. “The industry can’t do anything with lead times like that.”

This is something I have heard before. In light of the discussion about peak oil as well as pressure to move away from hydrocarbons, it is not a surprise that in boardroom conversations, there is less of an appetite to move into projects that have decades-long timelines.

That’s also why the discussion around speeding up the time from discovery to first oil is an ongoing conversation. In Norway, where lead times are still very high, state-player Equinor is becoming more serious about cutting down the time it takes to move from stage gate to stage gate.

But whatever an operator does to minimise delays, increasing red tape can still put the brakes on projects. I spoke to an American onshore wildcatter who said that due to all sorts of legislation and regulation, it takes significantly longer these days to get the bit in the ground onshore in the USA. In other words, companies can talk about how they will accelerate developments, but we also need changes on the regulatory side to reduce time to first oil. That is the other side of the coin.

WESTERN COUNTRIES HAVE BECOME MORE UNRELIABLE

An important aspect that has changed the overall global exploration outlook is how Western countries have positioned themselves towards continued drilling activities. Where in the 1970s, majors moved into the North Sea to find a very attractive basin with major potential, this cycle has started to come to an end. That’s not only because of the maturity of the basin; it is also because many Western nations have shown themselves to be critical of continued oil and gas exploration. Denmark, Spain, New Zealand and the UK have all been vocal about either banning exploration altogether, or putting on the regulatory brakes.

The recent news about bp now openly contemplating a UK North Sea exit is surely partly driven by the lack of government support.

This does is to create less clarity for companies to invest, as we see in the UK sector, where Apache may be the best example of the response in corporate decisions to these measures. They stopped drilling development wells on the Forties and Beryl assets overnight when the government imposed a tax hike, and is now in the process of decommissioning these major North Sea fields.

Meanwhile, New Zealand has already returned to welcoming explorers again following a ban imposed by the previous government, but even though the energy agency has already received two new applications on the back of the reopening, the question everybody asks is how long this welcoming regime will last, given that there will be a round of elections at sometime in the near future.

Political uncertainty remains the big ticket item that many Western countries don’t have a solid response to, because it will always go against the foundations of what these democracies stand on. Even in Norway, which is a country many see as a symbol of stability in regard to continued support for oil and gas exploration across party lines, an exploration manager I interviewed a while ago admitted that state player Equinor put the brakes on drilling for a few years on the back of more scrutiny from parliament. Even Norway is not immune.

In conclusion, many western countries — most notably the UK North Sea — have reached a mature stage of exploration, leaving limited scope for further investment. Political shifts and associated policies towards E&P companies have further curtailed the scope for continued exploration spend.

Rig market

The rig market is also a good indicator of the state of play in the exploration domain, and how this market has consolidated just as much as the operator landscape. An informative post on LinkedIn from Dan Fortser makes a few good points. “The offshore drilling sector consolidated more in 18 months than it did in the previous decade,” he wrote.

Transocean is acquiring Valaris, Noble has absorbed Diamond Offshore, and ADES has aquired Shelf Drilling. “This leads to a situation where the top three floater contractors now control roughly half the global fleet, and all these deals were struck when oil was $60 – 70.”

With oil being back above $100 with no near-term end in sight, Dan sees a rig market that is getting “very hot”. At the same time, he describes cost-cutting targets across these mergers mean headcount cuts to shore-based teams who manage procurement, maintenance programmes, and vendor qualification. “When the operational surge hits, and it will, the people who support them won’t be there.”

“It’s not just a supply problem any-more,” he concludes. “It’s a concentration problem. Fewer entities control the assets, the workforce, and the pace of reactivation. The bottleneck isn’t just rigs and people anymore. It’s who owns the rigs and employs the people.”

The sorry state of the service sector supporting the exploration business

Due to the lack of drilling activity, especially in drilling exploration wells, I see a lot of people who are very skilled but are waiting for the job market to pick up again. Likewise, there are companies that are just hanging in there, with some people indicating that it won’t be long until they falter. I met someone just the other day, representing a small outfit that helps operators drill their wells safely. The geologist attended a conference for the first time in his life, clearly because so far, there had never been a need to do so; the work came to them through their network. Now that the direct route seems to have dried up, he decided to venture to the conference arena. Another indication that the entire service sector in this space is contracting is the decline number of exhibitors at conferences. Over the past few years, this downward trend has become increasingly apparent.

Putting the money where your mouth is

At times of unlimited access to short and bite-sized news and post feeds, it is easy to be convinced of the arrival of a new wave of exploration drilling. And whilst there is indeed a real increase in acreage uptake, and countries opening up (again), it is still early days to conclude that we have entered a new phase of increased activity. The limited commitments that come with the award of new licences are a testament to that, and there is no indication that we are on the verge of a hiring spree.

These observations show that even when we are at the start of a new exploration cycle, the overall setting has changed. Western countries, especially the European ones, have shown themselves to be unreliable when it comes to political support for oil and gas exploration, whilst their own resources are depleting.

Meanwhile, China seems to be more successful in finding oil. Quietly picking up acreage in Iraq, it has not only discovered the largest oil field last year; if the recently announced find in their Qarnain licence in Western Iraq is indeed true, they have a good chance of yet again claiming the price in 2026.

We are now waiting for the IOC’s to make discoveries they badly need to bump up their reserve replacement ratio. And that doesn’t come with picking up licences alone.