West Africa, Sierra Leone. Photo: Sha Jaman/Wirestock via Adobe stock.

The Supermajors are scaling up, are you?

With an upsurge in frontier exploration worldwide, supermajors are developing new strategies. Where some basins have been ignored for a decade, a new frontier phenomenon is playing out, super-scaled exploration by the supermajors. West Africa in particular is centre stage for this new strategy, where the biggest oil companies are seeking basin-scale dominance

In the noughties and 10s, wildcat exploration, the fierce frontline of the E&P sector, was characterised by small ambitious pioneers, testing new plays in large basins, with the large caps and majors usually playing the role of “fast followers” when the drill bit turned heads. The likes of Hardman, Sterling, Ophir, the “Azi” group of companies, White Rose, Vanco and Black Star brings powerful memories to most exploration veterans. These outfits took up hugely ambitious positions, funded early-stage exploration, and traded their reputation and shareholders’ dollars on a prospect’s chance of success.

Whilst the industry waits with bated breath to welcome back this latent cohort of plucky pioneers, the majors and supermajors have taken matters into their own hands. The “supers” have taken large multi-block reconnaissance and PSC positions in frontier basins, to establish basin-scale footprints where they plan to invest. This strategy allows well resourced companies to screen whole basins before committing, or not, to intense exploration campaigns.

Establishing the new order

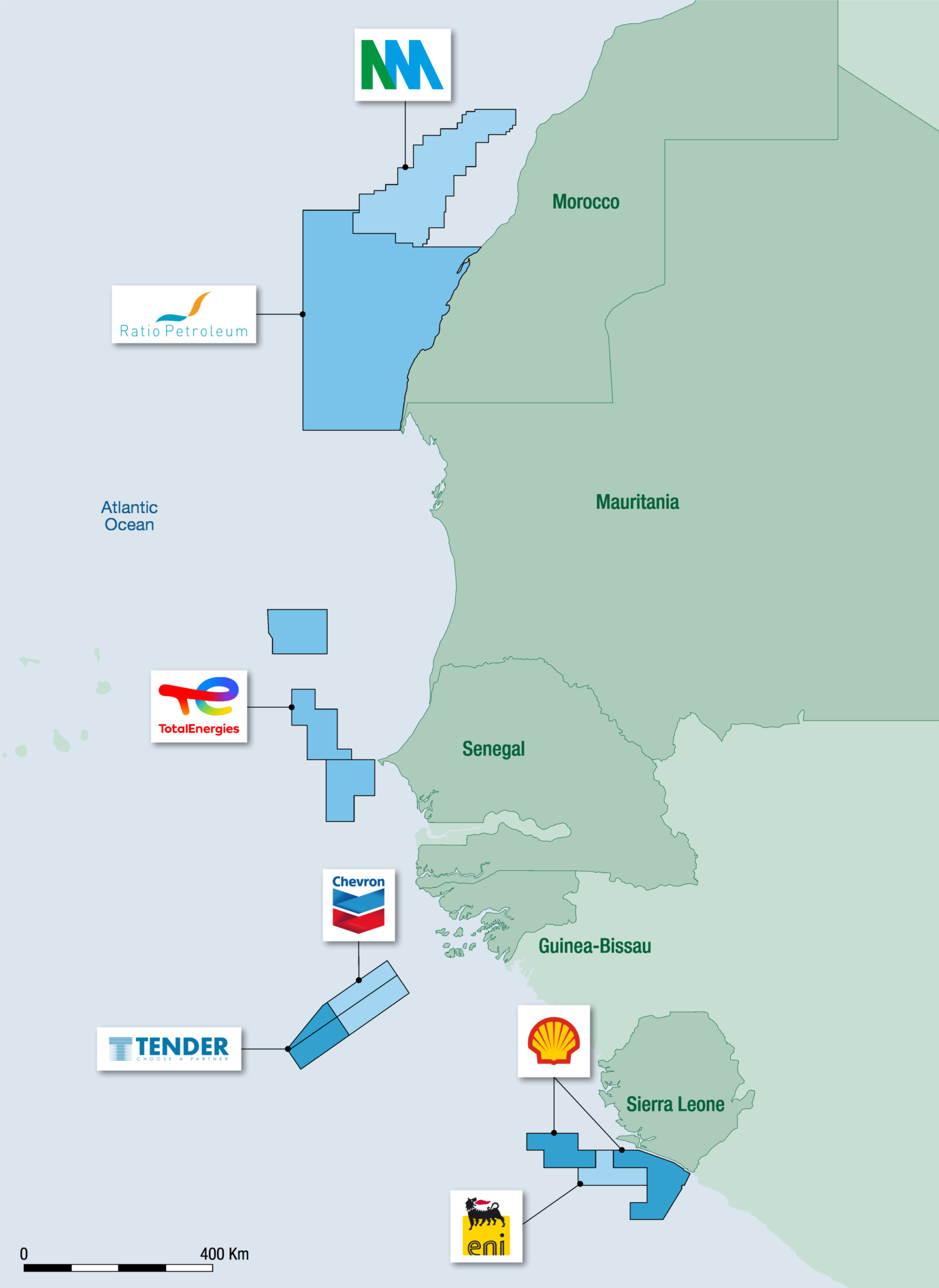

Early signs of this new approach were flagged in the MSGBC in 2016. NewMed took a large position at Boujdour in 2016, followed by compatriot Ratio in 2018 with a large PSC at Dakhla Atlantique, both offshore southern Morocco. In 2018, TotalEnergies chose to push the envelope on the Sangomar/FAN trend, with a large PSC over Rufisque Deep and Ultra Deep Offshore (UDO), an early sign that the supers wanted to explore basins, not blocks.

Fast forward through an oil price crash, poor investor sentiment on the back of climate change fears, a global pandemic, and the Prize is back in focus in the 2020s. The biggest oil companies are revving up new ambitions with basin-scale access once again. What appears to connect this new exploration theme are competition, scale, and capturing the top of the creaming curve early with the largest prospects. This represents a pragmatic shift to affordable work programme commitments through reconnaissance geology and geophysics, before major drilling commitments.

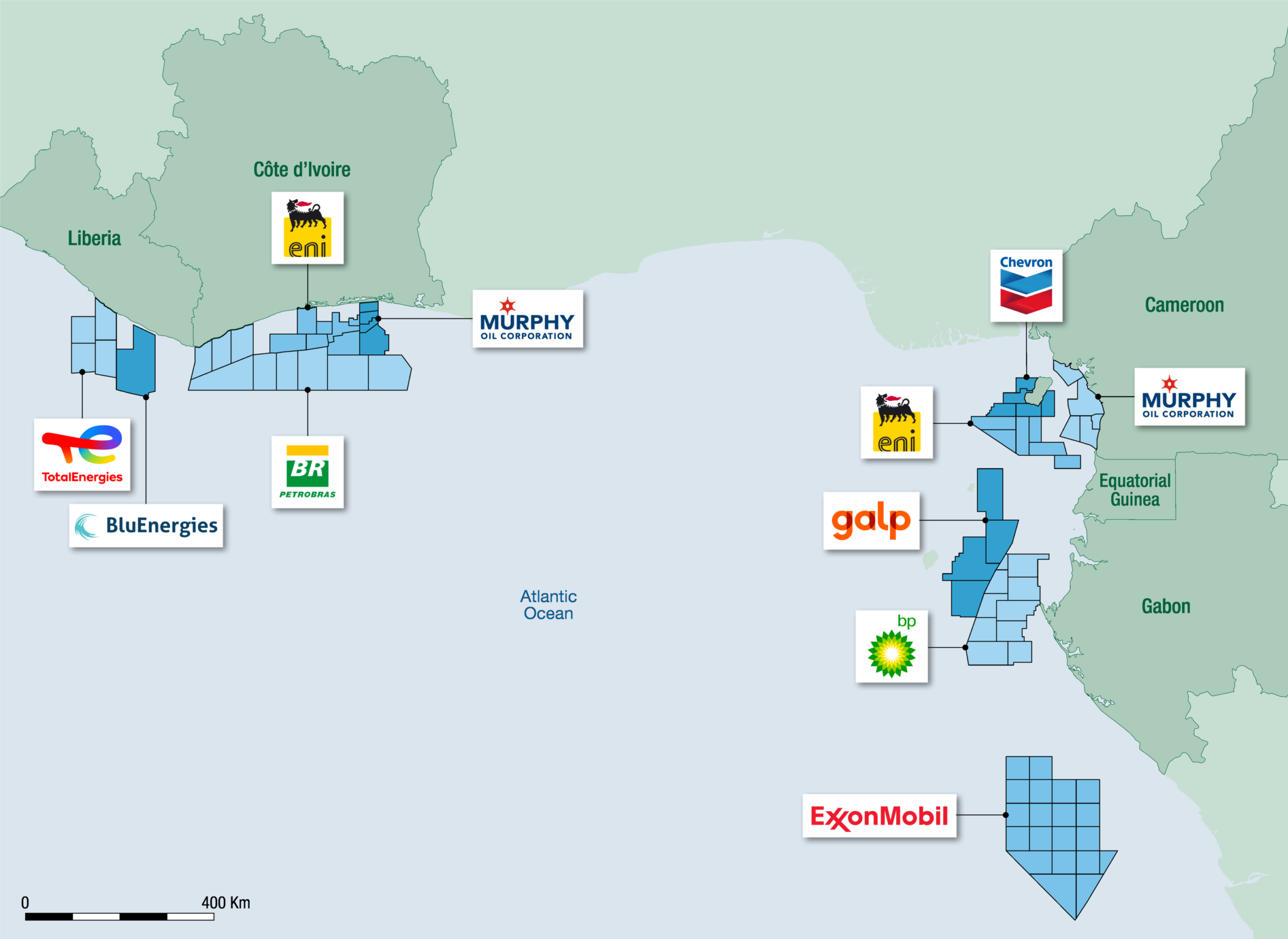

In 2024, Petrobras were reported to be evaluating around 50,000 sq km offshore Côte d’Ivoire, covering at least 8 deepwater blocks. An award has yet to materialise, while Murphy did take a major 5-block position with full PSC terms and a three well commitment between the Baleine and Baobab trends. The industry awaits the results of their third wildcat there, Bubale -1X.

This signalled the start of a major renaissance across the Transform margin, sparked in part by Eni’s billion barrel blockbuster at Baleine and the availability of country-wide exploration acreage. Eni itself took a large 7-block position to protect the wider Calao trend soon after Baleine was discovered.

Liberia took the lead next, with exploration junior Blu Energies working a new plan to build a large exploration position that would fit the super’s new strategies, with low capital exposure utilising reconnaissance-style commitments. In 2024, Blu was awarded a 3-block tract over the Harper Basin, a shrewd move that took advantage of good quality existing multiclient 3D, and new play theories that extended the offshore envelope to deep marine basin floor fan style targets. In 2025, they were rewarded with a Joint Study Application Agreement with TotalEnergies. TotalEnergies saw the model, saw the data and, perhaps galvanised by success in ultra deepwater Namibia at the Venus basin floor fan play, concurrently signed up a further four blocks to seal a major PSC to the west of the Harper Basin. Oranto took three blocks adjacent, reinforcing their long-term strategy of real estate positioning.

The work programmes on these reconnaissance-style multi-block areas and joint application deals appears to hinge mainly on reprocessing seismic, applying modern QI techniques, and taking time to develop a new petroleum play fairway model for these high-risk offshore basins.

Sierra Leone, with a similar recent history to Liberia for intense but short-lived exploration campaigns in the 2010 to 2015 era, saw an opportunity to build on this renewed appetite for frontier acreage. Petroleum Directorate of Sierra Leone (PDSL) started a major drive for new investment, utilising all available data and providing access to acreage to well-qualified companies. After assigning a large PSC to FA Oil, the promotional data room efforts of PDSL attracted Eni to take a 6,790 sq km 5-block spread over the heart of the offshore basin, under Reconnaissance Licence terms. Most recently (in April 2026), Shell has followed suit, taking a huge 19-block tract (about 21,000 sq km) to capture a lot of the remaining acreage, again under relatively easy reconnaissance terms. Marginal Energy of Nigeria signed a large PSC adjacent to Shell at the same time.

As we go to press, Eni appears to have captured the entire offshore Guinea Conakry estate, in a move reminiscent of the original full-scale basin strategy of Hyperdynamics in 2006.

Protection Acreage

Established petroleum provinces in West Africa are enjoying this new wave of attention from the supers. In Equatorial Guinea, Eni has taken a 21 month Recognition Agreement with the government, on the back of a technical evaluation and training programme, covering 6 blocks across the central petroleum province, with the Rio Muni/Ceiba play to the south. Chevron have negotiated a multi-block reconnaissance permit over 6 or more blocks covering the northern swath of open acreage in the country. Chevron are already busy at Aseng and Alen, moving from oil to gas production, and will chase potential oil plays in the Cretaceous and Tertiary systems there. Galp have taken three large blocks between Chevron and Eni in the same Cretaceous Equatorial Guinea play fairway.

Murphy continues its resurgence in West Africa with four contiguous blocks awarded with full PSC status offshore Cameroon.

Offshore Gabon, bp have taken a reconnaissance-style agreement over 10 blocks in the North Gabon basin, extending exploration efforts back up to the borders with São Tomé and Equatorial Guinea. In the South Gabon deepwater basin, ExxonMobil has signed an MOU to evaluate 20 contiguous blocks, with preferential rights to negotiate PSC terms should their mapping reveal significant potential.

São Tomé itself has seen its fair share of multi-block exploration evaluation from the likes of Galp, Kosmos, bp, Shell and Petrobras.

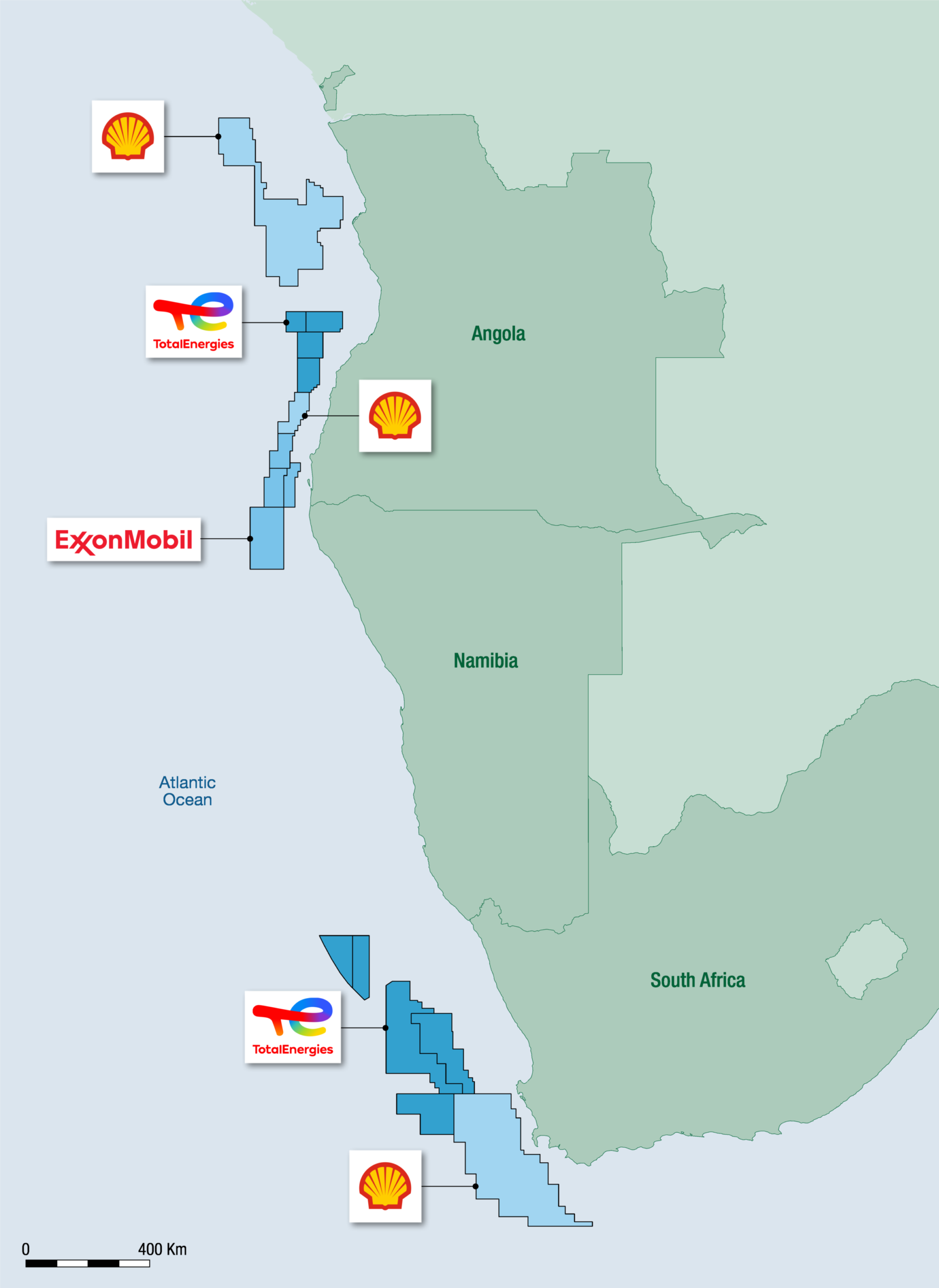

The upstream regulator in Angola has made great efforts in recent years to help the country attract further investment for frontier exploration. After the halcyon days of super-production with the supermajors, ANPG see a clear opportunity to encourage new exploration efforts with large exploration tracts, large contiguous modern datasets and improved fiscal terms for high-risk exploration. Some of the long-term players there, such as ExxonMobil and Equinor, have taken new frontier blocks in the Kwanza, Namibe and Benguela basins on the back of improved fiscal terms and extended tenures in the traditional Block 15 to 17 producing heartlands of the Lower Congo Basin. Most recently, ANPG has agreed “Principles” with TotalEnergies and ExxonMobil for four large, underexplored blocks in the Benguela and Namibe basins. Furthermore, Shell have an MOU with ANPG for a vast area of unexplored deepwater acreage, west of the established exploration trends, from Block 72 in the north to Block 54 in the Benguela Basin to 19/11 in the East.

ExxonMobil has already captured the bulk of the Namibe Basin, with around 8 contiguous PSCs spanning north and south of the Angola-Namibia border.

In South Africa, TotalEnergies had already built an extensive tract of frontier acreage from deepwater Orange Basin (adjacent to the Namibia Orange Basin asset) and Orange Basin Deep and 3B/4B, through to Block 5/6/7 and 11B/12B in the Outeniqua Basin. TotalEnergies have since left the latter two blocks, leaving Shell with a commanding position on 5/6/7.

Large basin-wide campaigns are not unheard of onshore either. Several firms have taken basin-scale positions in Angola, Zimbabwe and Tanzania, with ReconAfrica picking up onshore acreage in southern Angola as an example. The migration of this strategy to deep offshore tracts reflects a renewed confidence in exploration at scale, driven by advances in seismic acquisition, processing and interpretation, and the strategic need to tie up an entire play fairway before the spoils can be divided.

The price of dominance

Of course, the typical terms for these recent MOUs, Principle Agreements and Reconnaissance Permits differ across jurisdictions, but the trend is to assign non-exclusive access to the acreage and data for 1 to 3 years, with work commitments including 3D reprocessing and re-mapping oil and gas fairways. New plays are being introduced by innovative new ventures teams, where they may have been ignored in the deepwater, for example basin floor fans on the abyssal plain, and carbonate reservoir plays. New seismic acquisition is often included, along with modern geophysical screening. Governments cannot expect major signature bonuses, but data and interpretation bring new value to old plays, lifting the lid on completely new plays, and local content and skills transfer benefits are often built into the agreements.

There are clearly pros and cons to this burgeoning tradition of large-scale basin-wide exploration. For the supers, these licences provide an opportunity to screen entire basins whilst keeping a competitive advantage. Work commitments can be relatively lenient, moving drilling commitments into the future and allowing for detailed G&G work. Both the government and oil companies can take advantage of existing good quality multiclient 2D and 3D, which otherwise would be gathering dust. The oil companies also effectively secure large areas on which to commit their severely diminished resources, without being sidelined by ambitious minnows taking new contracts. The ability to capture large areas clearly supports multi-year campaigns with little chance of competition.

Conversely, governments, regulators and NOCs, whilst encouraging new investment, have to acknowledge that major tracts of acreage are effectively locked up. Whilst reconnaissance-style agreements can be non-exclusive, the door may appear tightly shut to smaller low-budget players looking to pick up on new plays. Will the scaled-up blocks lead to scaled-down wildcat drilling over time? Difficult to argue after the collapse of wildcatting between 2016 and 2024, but individual PSC blocks would have attracted individual work programme commitments. The reality is large tracts of frontier acreage are waiting for expensive exploration campaigns from a shrinking community of large oil and gas exploration firms. Exploration companies and regulators await the completion of these mega-exploration deals, with the return of exploration acreage and often new data. On completing the reconnaissance work, will the supermajors’ exits discourage further investment? One thing is for sure, as the world finally comes to terms with its reliance on the natural resources of the subsurface, demand is set to remain.