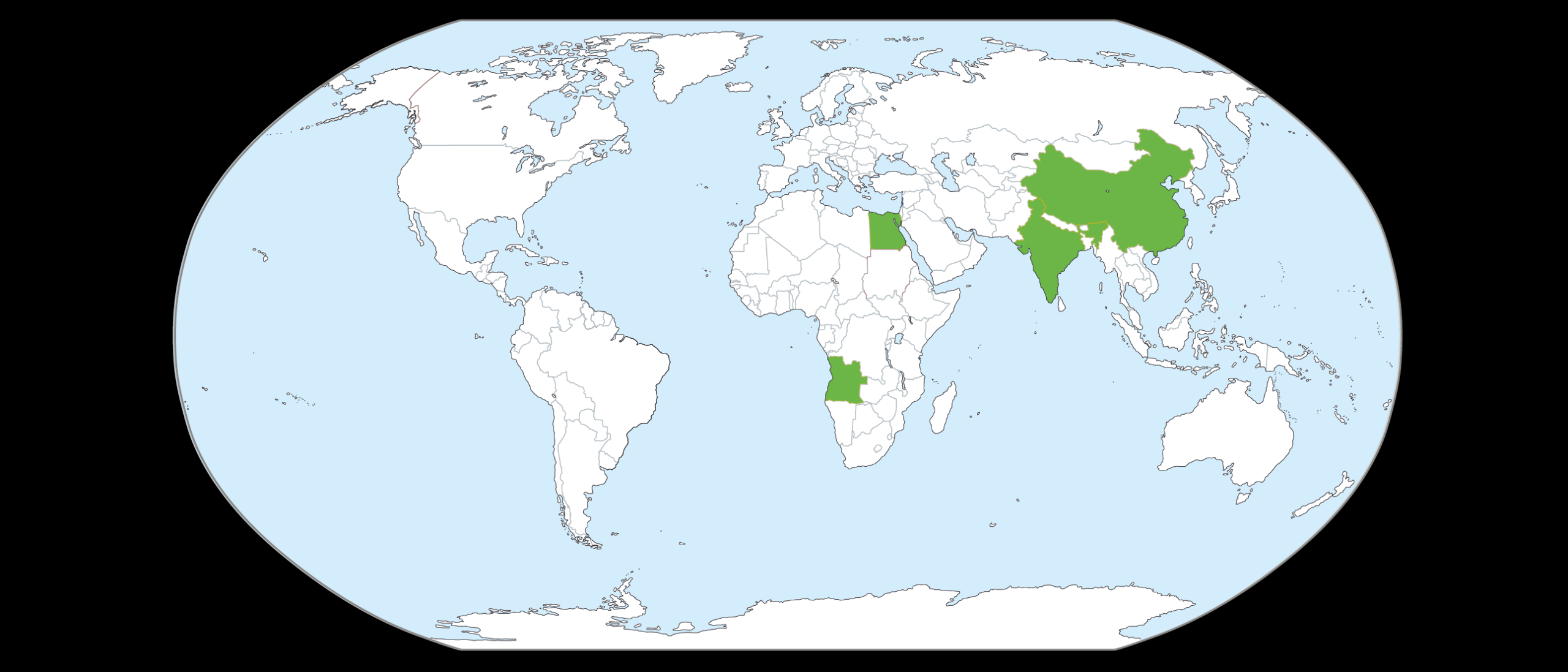

Asia and Africa Investment Dominate Early 2014

Egypt

Both the Egyptian General Petroleum Corporation (EGPC) and the Egyptian Natural Gas Holding Company (EGAS) launched international bid rounds early in January 2014. EGPC is offering 15 exploration blocks comprising five offshore Gulf of Suez blocks and 10 onshore in the Western Desert. EGAS is offering seven blocks in the Mediterranean Sea and Nile Delta Basin. In both cases the bid round closing date is set for 19 May 2014.

After the mid-January election, Egypt is facing an economic and investor crisis as it continues a period of turbulent political transition, with basic issues over its political system and electoral future still unresolved. With decline rates at mature oil fields and problems with natural gas availability both supporting the argument for an increased role for foreign investors, the lack of regulatory stability is seen as a major stumbling block. The award process has been shortened in an attempt to retain investor interest but other issues still linger, gas prices in particular. Nonetheless, BP, Eni, BG, and Apache remain major players and neither Egypt’s level of production nor the Suez Canal was significantly affected by the 2011 revolution. Oil consumption has increased at an average of 3% per year over the last decade and has exceeded the production rate since 2010, while gas consumption climbed an average of 11% per year since 2001.

China

China National Offshore Oil Corporation (CNOOC) is offering foreign operators a chance to partner it in 25 blocks offshore China, covering over 100,000 km2. Of the blocks on offer, two are located in Bohai Bay; three lie within both the East China Sea and South Yellow Sea; 10 are in the eastern South China Sea while the remaining seven are located in the western South China Sea. Notably, this is the first time that CNOOC is making blocks in the South Yellow Sea available for foreign company participation. This region is underexplored, and while an understanding of petroleum systems needs to be improved, there is a good deal of optimism regarding its potential. The bidding closes on 30 April 2014.

This round offers a significant amount of offshore acreage, testifying to efforts to boost domestic exploration and production as well as a strategy to bring in foreign investors to buttress territorial claims to acreage in the South China Sea. As yet, no opposition to the round has been mooted by neighbouring countries.

Angola

Following the approval of the strategic framework for the licensing of 15 onshore blocks in the Kwanza and Lower Congo Basins, Sonangol is proceeding to hold its first major onshore concession tender. The decree includes the granting of five onshore blocks exclusively to Sonangol for initial assessment; if they are successful, interested parties will bid on the acreage at the development stage, with Sonangol retaining a participating interest. It is understood that four of the blocks are in the Kwanza Basin and one in the Lower Congo Basin.

For the remaining 10 new concessions, national and international interested parties are invited to compete for three blocks in the Lower Congo Basin and seven in the Kwanza Basin. It is believed the decree specifies that Sonangol will retain a 50% share in four of the Kwanza Basin blocks. It is also reported that the state will provide financial support to encourage private domestic companies to bid on the onshore blocks to increase local content in the industry, which only employs about 1% of Angolans, while investing about US$20 billion a year. The authorities intend increasing domestic production from 1.75 MMb/d to 2 MMb/d by 2015, a target that seems unlikely given the delays in launching the round.

India

At the Petrotech 2014 conference in January the Indian government announced that 46 blocks have so far been finalised for inclusion in the 10th round of the New Exploration Licensing Policy (NELP X) which will be launched in February. According to Petroleum Minister, Dr Verappa Moily, the total numbers of blocks to be offered may reach 60 if the government can secure additional environmental, defence and other permit clearances. The 46 identified blocks, with a total area of 166,053 km2, have received all statuary clearances from relevant ministries and include 17 onshore, 15 shallow water and 14 deepwater blocks. It is understood that they will be offered under ‘completely revamped terms’ based on revenue-sharing rules and new gas pricing. Revenue sharing will be determined in a competitive bid process with the bidder offering different percentage revenues for different levels of production and price levels. The proposed new regime is yet to be approved but analysts are sceptical, believing that revenue-sharing models only really work in areas of significant oil reserves, which India does not have.