Operations at Christian Dohse’s Waxwing Energy prospect during the drilling of a new well in the South Texas brush country. Photo: Christian Dohse

The American small independent operator – A unique blend of geology and entrepreneurship

This year, I went to the NAPE Exhibition in Houston for the first time. NAPE stands for North American Prospect Expo, and has served as a platform for American operators to market their prospects and find investors since 1992. NAPE is different from other industry events because the majority of stands on the exhibition floor are taken up by small operators showcasing their drilling opportunities. In many cases, you will be able to negotiate on the spot and buy yourself an interest in a drilling project. What makes this event so fascinating is that many of the people on these stands are the geologists who worked up these prospects themselves, and also organise everything else required to make drilling and production happen. It is a genuine mix of geoscience and entrepreneurship that is so unique to America. This article introduces you to a few of these entrepreneurs I met in Houston in February, telling their stories of how they ended up doing what they do.

HOW NAPE EVOLVED

The NAPE show has evolved a lot over the years. “Thirty years ago, it was a room full of tables in what is now the Galleria area of Houston,” says Tom Armstrong, who was there from the very start. “A prominent feature of the room was the line of cell phones that potential buyers could use to discuss matters with the head office before making a deal.”

Someone else told me that NAPE used to be much bigger than it is today, up to three times as big. That’s incredible, because I found the size impressive even this year. The number of attendees has also come down, I was told. Nowadays, it is around 6,000-8,000 people, whilst it was around three times as many years ago. “You couldn’t walk through the aisles quickly,” someone said.

Most people agree that an important factor explaining why NAPE has become smaller is the arrival of unconventional players. They had big stands, surrounded by financial firms. That seems to have calmed down now, as people have figured out that even when there is less geological risk in unconventionals, there is still a financial risk.

Today, NAPE is more than a prospect show, with many service companies exhibiting as well. But there is no way to escape the trend that the number of people representing the small players, something the conference was always intended for, has come down over the years. That’s what almost everybody tells me. And it is visible from a demographic point of view too; most exhibitors promoting their prospects are men who are either retired from their corporate jobs or are close to doing so altogether.

Is the end of the small independent near? From what I have seen and heard, it looks like the independent American producer is indeed a slowly disappearing species. I would say the shale boom is an important factor there. Geologists who have worked their careers in shale are not familiar with the type of risk-taking that comes with drilling conventional wells, which means that there is a major gap in the influx of people wanting to get their hands dirty. On top of that, there is the increasing pressure of permitting, which is slowing processes down.

It is a shame, because from what I have seen, these small independents, even when they don’t produce so much when added up, this group of people harnesses so much practical experience that they also transfer to the people they work with. In that sense, they are still a foundation of what the American oil and gas industry represents: Entrepreneurship, willingness to take risks, and a willingness to get your hands dirty at the same time.

“As many people in this business, I’m a risk-taker” – Jeff Swanson

Jeff is a striking figure. “I played basketball when I was young,” he says. After completing a business degree at Southern Methodist University, Jeff didn’t really know what to do first, so he initially continued his basketball career in Europe. Then his dad called for help. He was a geologist working for a big corporation – the family had moved fourteen times as Jeff grew up.

When his dad decided to start working for himself, he asked Jeff if he wanted to join. “Playing basketball was more fun, but I realised that I needed to change careers and become a bit more serious,” says Jeff.

So, he joined his dad’s start-up reservoir description company, which took them to Venezuela for four years, principally consulting for PDVSA and its affiliates.

But it was not only reservoir description work that Jeff and his dad were offering as a service. They were also instrumental in developing software that enabled users to build what is now known as 3D geocellular models.

Under the name Stratamodel, the team built the software from first principles, also patenting the workflows along the way. It caught the attention of the major oil and gas service providers, ultimately leading to a merger with interpretation platform Landmark. And with Landmark being acquired by Halliburton less than a year following the merger, the software is still being used today.

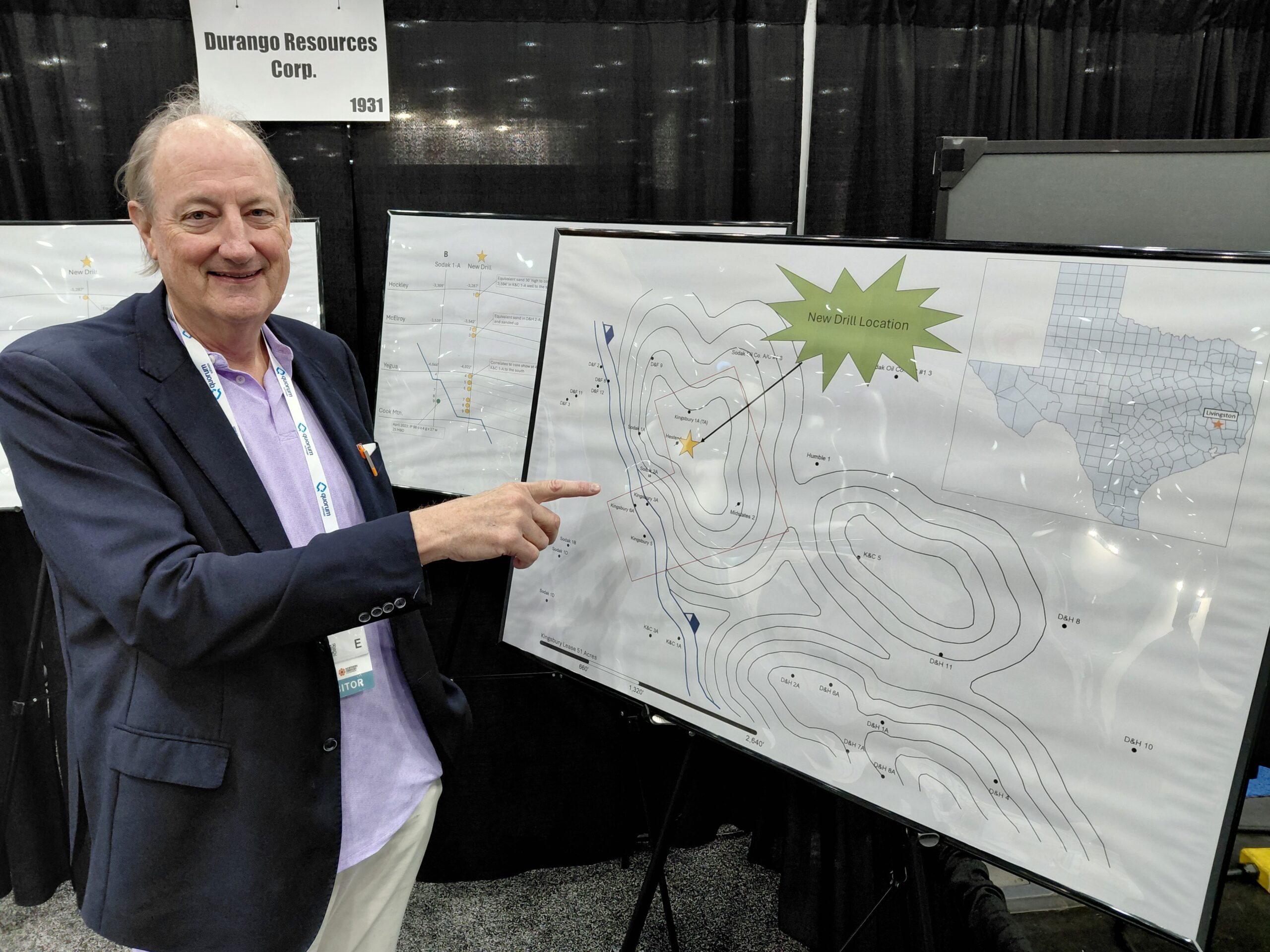

Whilst the people who had developed the software joined Landmark, Jeff decided to move on. It was in those years that he decided to set up his own oil and gas producing company, Durango Resources. “We focus on acquiring producing assets and try to optimise production through workovers and infill drilling.

“As many people in this business, I’m a risk-taker,” he says. “I’ve made a lot of money, but I’ve lost a lot too.”

Investing in new wells is obviously the most expensive part of the business, and if these wells don’t work, they become a burden to a project. “We had two expensive horizontal wells drilled on one of our assets,” says Jeff, “and neither of them produced as much as we expected. We spent years investigating what could have gone wrong, but we never fully got to the bottom of it.”

Jeff is at NAPE to find investors for a new prospect on one of his leases. It is a small but typical old-school, structural Gulf Coast prospect at a depth of around 5,000 ft. “We identified it because our neighbours to the south perforated the same target sand and achieved an unexpectedly good result,” says Jeff.

“We never paid too much attention to this interval because old log data from the area suggested that the quality of the reservoir wouldn’t be that great,” he continues. “Then it turned out that another company operating to the west of where we are also found the same reservoir, being more productive than anticipated, so it became quite obvious to us that there was something to be tested. That led us to identify a prospect in time-equivalent strata in our lease as well.”

“It’s a fairly low-risk prospect,” continues Jeff, “but obviously, there is always a chance that the trap has been breached by some of the numerous faults – some of which are sub-seismic – or that a legacy well produced from the reservoir without there being a report about it. That happens in an area with a long history of oil production; there is always the chance that things go unreported.”

With drilling costs under $1 M, Jeff’s prospect has an estimated return of 5:1. Even though he did not sell an interest on the spot, the conversations he had at the event have already led to some follow-ups. He is therefore hopeful of progressing the project soon.

“You might not think there is land south of New Orleans, but there is” – Bo Sibley

Bo Sibley worked in Southern Louisiana during his entire career. “I would not be comfortable drilling a well in Western Texas,” he says.

When he retired from his corporate job as a petroleum engineer, he felt he wasn’t done yet and found a broker offering a producing asset in the area he is so familiar with.

“It is south of New Orleans, Bo says. “You might not think there is land south of New Orleans, but there is.” The area where his asset is situated is surrounded by levees of the Mississippi River, in a green and lush environment.

The lease consists of six wells, of which only one was producing at the time Bo made his purchase. But still, it meant that he was generating income straight away.

Then it turned out that the producing well experienced sanding issues. “We had to do a workover and install a sand screen to get rid of the issue,” says Bo. “So, we went in, but then it turned out that the casing had collapsed, preventing us from installing the screen.”

The well is now shut in, and a decision has been made to side-track the parent well and penetrate the reservoir with a new hole. It is the financing of the side-track that Bo is finding investors for at the NAPE conference. “It is worth drilling the side-track, Bo says, “as I expect there to be around 200,000 bbl of oil left to be produced.”

Bo obviously hopes to find investors at the conference, but he also reiterates that you don’t want to have too many stakeholders in a single project. “Three or four partners is a good number,” he says, “otherwise it will get too crowded with too many cooks.”

“I was young and had too much energy to sit at a desk in downtown Houston the whole day” – Christian Dohse

“I grew up in the Corpus Christi area and was fascinated by the pump-jacks I saw in the landscape from a very young age,” says Christian Dohse when I meet him at his stand in the George R. Brown Convention Center. “It triggered my interest in geology, wanting to know what happened in the subsurface.”

As such, Christian went to study geology when he left secondary school, and was lucky enough to land a job with Hess in Houston. However, it didn’t suit him as much as he had thought. “I was young and had too much energy to sit at a desk the whole day in downtown Houston,” he says.

He was lucky enough to find part-time roles with two small companies in the Corpus Christi area, which meant a lot more hands-on work and a much more flexible schedule. One of the jobs was with a gas producer, whilst the other company produced oil. However, as time moved on, and the shale gas boom started to manifest itself, the gas operator was pushed out of the market, so Christian had just one employer left. However, that also came to an end when the pandemic hit, and Christian decided to venture into something different for a while.

But the industry still appealed to him, and at some point a few years ago, Christian started looking at obtaining a lease in the South Texas area. He started pulling together well and seismic data to look for a prospect that he could get his hands on.

“I mapped a prospect on a plot of land that wasn’t under lease yet,” he says. “The landowner, a rancher who is into bird watching, was happy to lease me the mineral rights and because it was my first lease, I decided to name my new company after one of the local birds that would frequently visit my yard – Waxwing Energy.”

Christian drilled his first well, and now has production from the field he discovered.

He is at NAPE to find investors for another conventional oil prospect he wants to drill. Looking at the map he’s got at his booth, it is clear that this onshore trend of the South Texas Gulf Coast has seen a lot of drilling before. The petroleum system is therefore proven; it is a matter of testing valid traps in upthrown fault blocks. The closure Christian has identified is in Eocene sands of the Yegua Fm, and could hold up to 441,000 bbls of oil and 250 M ft3 of gas if the prospective reservoirs are present and hydrocarbon-bearing.

In an email conversation following the conference Christian shared that he has now placed all the interest in the prospect and that he will be drilling the well later in spring or summer.

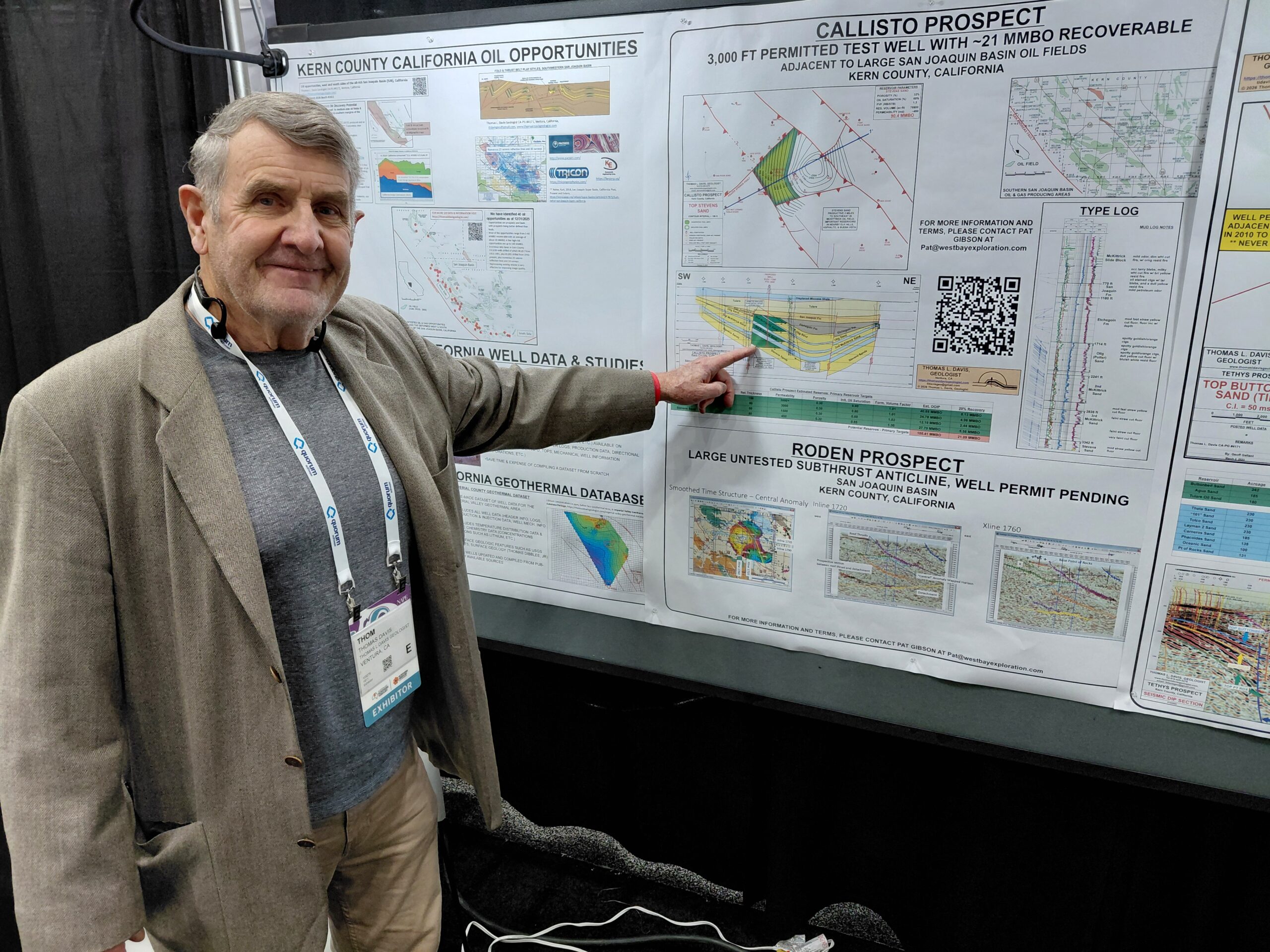

“Having a little oil production ticking away in the background is a great way to generate some income” – Thom Davis

“I don’t want to live from project to project all the time, as so many consultants do,” Thom Davis tells me when we meet on the NAPE exhibition floor, where we both have a little stand in the same aisle. “Instead,” he says, “having some oil production ticking away in the background is a great way to generate some ‘passive’ income to cushion the periods when there is little project work around.

Passive is a relative term here, as it takes considerable effort to get a new drilling project up and running, especially in California, where Thom works and lives. “The state has not been easy about permitting,” he says, “for reasons we all know. But the mood is changing, and we believe a more welcoming regime may be returning,” he says.

It took around four years to get the regulatory approvals for the Callisto prospect that West Bay Exploration Company and Thom want to drill. It is also a project that Thom is trying to find investors for in Houston. “Geoff Gallant, a geologist on my team, and I have eyed this opportunity for nearly 20 years,” Thom says.

When we are in between consultancy jobs, Thom and Geoff have the habit of going through old wells drilled in the San Joaquin Basin, and by doing so, they have found several opportunities, especially when combined with reprocessed legacy seismic.

“The San Joaquin Basin is considered a Super Basin, with 5 Bbbl still to recover,” says Thom. He also leads field trips and Geo-hikes in southern California, which is a fold and thrust belt bisected by the San Andreas fault, with many good outcrops and panoramas. His Geologic Maps Foundation digitises legacy geological maps from the region and makes them freely available to the public.

The estimated dry hole costs are just less than $1 M plus $300,000 to complete for the 3,000 ft well that Thom aims to drill on the Callisto prospect. If all four individual sandstone reservoirs come in, the prospect might contain 20-25 MMbbl of oil. The prospect relies on an element of trapping against a fault, well known for trapping several hundred million barrels just to the south, as well as trun-cation trapping.

The cross-section Thom is pointing at in the photo illustrates the trap configuration of the Callisto prospect. It is also interesting to see the number of wells that were used to put the cross-section together; it clearly shows that the basin has already been extensively explored, with dry wells located on either side of the prospect.

But nevertheless, it is great to see that there are still people who are chasing the opportunities that no doubt remain. 25 MMbbl is not a volume to sniff at if you realise that some prospects being marketed at NAPE are only a few hundred thousand barrels large. If successful, Thom might even need more than just one well on Callisto, and maybe he can also take a longer break from his consultancy work and preserve more legacy maps.

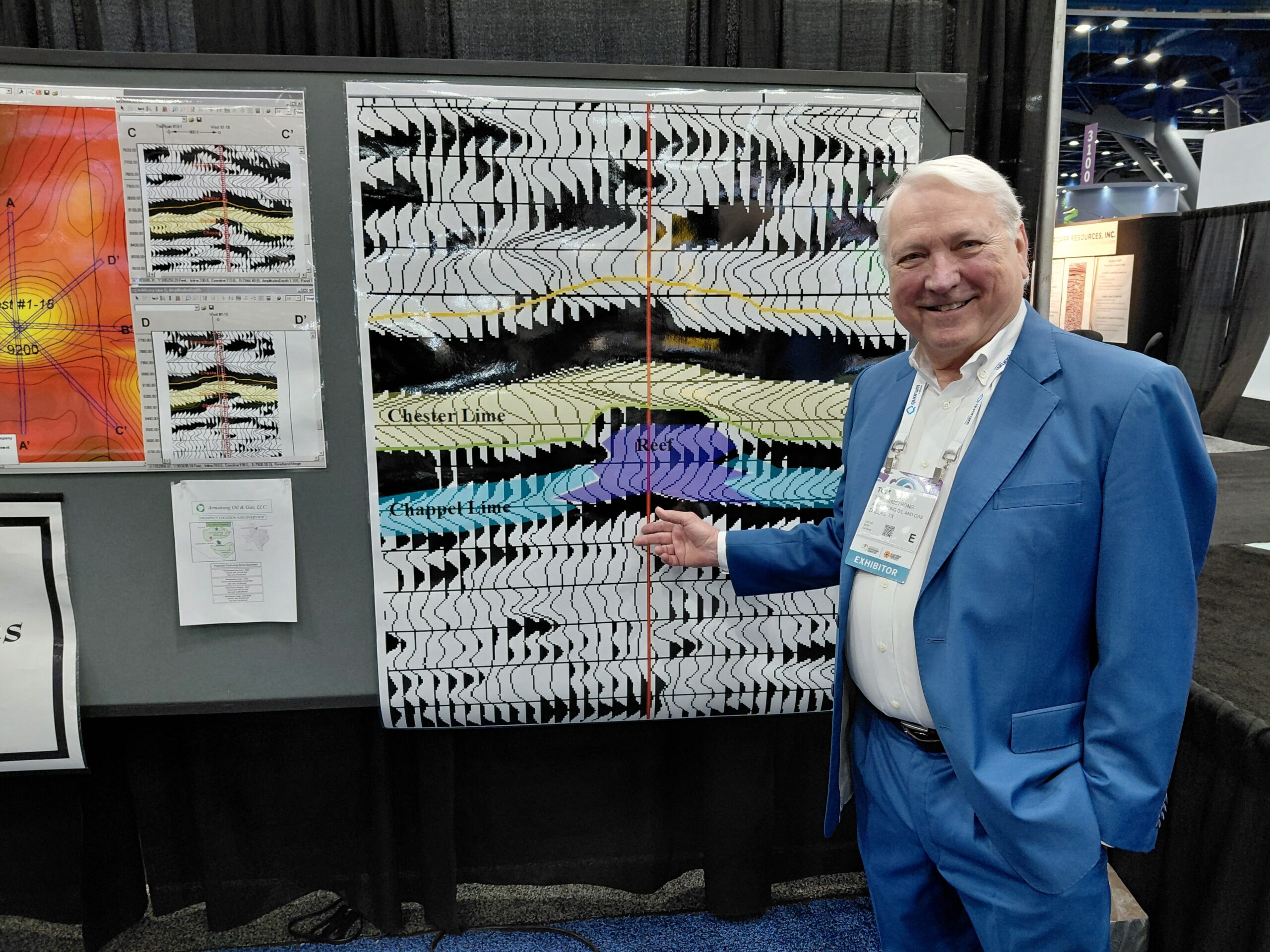

“Conventional oil production like this is much less sensitive to fluctuations in oil price than unconventional oil production” – Tom Armstrong

“I sat my first well as a well-site geologist in 1978,” Tom Armstrong of Armstrong Oil & Gas says. “And it was a two-million-barrel discovery straight away.”

Ever since, he has worked in the same area that straddles the boundary between Texas and Oklahoma, a place that is part of the Hardeman Basin. Here, Lower Carboniferous mud mounds form the target for most wells. Tom has an interest in 24 wells in the basin at the moment.

“It is a seismic play,” says Tom. “We analysed a large group of wells drilled in this play before and found that the most successful wells were the ones that had the most condensed unit directly overlying the reservoir. I don’t have a direct explanation for this, but the statistics clearly point this out,” he says. “As such, mapping prospects using seismic data is key.”

The areas of elevated porosity and permeability are also hard to predict in these carbonate mud mounds. “We are currently reprocessing seismic for that reason,” says Tom, “but it remains a risk for all wells we drill; a ‘dry’ hole in one position on the structure may be a successful one a little further away on the same closure. That’s the risk of the game.”

The prospects in the area are mostly small, with volumes less than 1 MMbbl being the rule rather than the exception. For that reason, the Hardeman Basin is a good place for small operators. “We pay around $200 per acre,” Tom says, “which is a price that works.”

Some years ago, Apache picked up acreage in the area and offered land owners a lot more per acre, remembers Tom. “It ruined the stability we had in the area, but they drilled a dry hole and left again after, so that was only a brief period after all,” he says.

“I have sold a 20 % share in the prospect already, but I’ve had cases where someone came to me and said, take the posters down, this prospect is mine.” That may not happen this time around, but there has been decent interest so far, and Tom shared later that he had a list of eleven companies wanting to meet up with him after NAPE to discuss his prospect.

The estimated cost of drilling the well on Tom’s West #1-18 prospect in the north of the Hardeman Basin is around $1.5 M. If the well turns out to be a success, and the volumes come in as expected, the rate of return could be as high as 25:1 when assuming an average oil price of $60.

“Conventional oil production like this is much less sensitive to fluctuations in oil price than unconventional wells,” says Tom. “I return a profit at $20 oil, whilst the main unconventional players in the Permian Basin will struggle to make money at $55 oil. That’s why there is still music in this type of work, even when the risk profile is different from the shale gas sector.”