Illustration: Hurca! via Adobe Stock.

Europe versus US oil majors

Why economics, not ethics, drives the energy divide

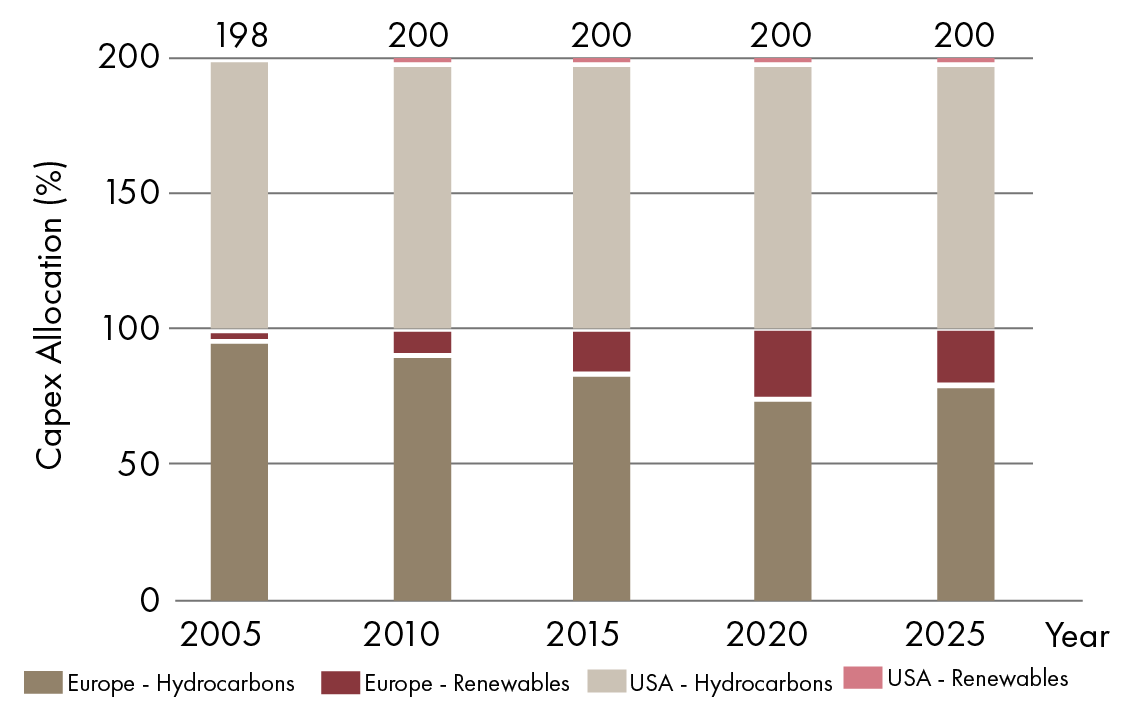

European oil majors face a structural dilemma: How to balance near-term hydrocarbon revenue with long-term renewable ambitions under relentless shareholder and public scrutiny. While USA peers largely doubled down on hydrocarbons, European companies spent two decades allocating billions to offshore wind, hydrogen, and other low-carbon ventures. This divergence created a widening performance gap and exposed a business model under stress as macroeconomic conditions shifted.

By 2020, European majors directed roughly 25 % of capex toward renewables, compared to near-zero for US firms. Policy pressure and ESG mandates drove this divergence, while US companies maintained a value-first approach. However, cracks emerged as renewable projects failed to deliver competitive returns, highlighting a strong financial and operational divide.

Economics under strain

Offshore wind economics have deteriorated sharply. Rising interest rates, inflation, and supply-chain disruptions inflated costs and eroded margins. High-profile cancellations signalled further distress, making financing unpredictable. Hydrogen faces similar headwinds: Weak unit economics and uncertain policy frameworks have stalled projects on both sides of the Atlantic. These setbacks underscore the vulnerability of capital-intensive technologies to macro shocks.

Renewables often appear cheaper based on Levelized Cost of Energy, but this metric excludes critical system-level costs like grid integration, storage, and backup capacity. When these are factored in, the economics shift dramatically. Financing dynamics compound the challenge – renewables require heavy upfront capital, making them highly sensitive to interest rates. Recent hikes disproportionately hurt offshore wind and hydrogen compared to hydrocarbons, which offer faster breakeven payback cycles. It should also be noted that costs are just half of the revenue calculation. The other half is the value of fossil fuels, nuclear and other dispatchable energy sources is greater than that of intermittent renewable energy. Therefore, the former can generate more revenue, even if they have greater production costs.

Shareholder value dynamics

Cancelled projects aren’t necessarily unprofitable – they are simply less profitable than hydrocarbons under current conditions. Boards under pressure to maintain dividends and credit ratings prioritise projects with the highest risk-adjusted returns. This pivot reflects a mandate to maximise shareholder value rather than a wholesale rejection of renewables.

Most European majors have reintroduced upstream drilling programs to arrest declining production and stabilise reserve replacement ratios. This turn reflects a recognition that without hydrocarbons, providing the required capital for the energy transition becomes increasingly constrained.

Even with the best intentions, incumbent energy firms face competing interests between transition goals and profitability. New capital structures may be required, including creating daughter companies with separate governance that are insulated from short-term profitability pressures.

This is not about ethics but economics. Until offshore wind and hydrogen regain predictable economics, hydrocarbons remain the most reliable source of cash flow to fund future transition projects. The key question going forward is: Will we see larger energy corporations deploying significant capital into renewables within the current or five-year outlook?