So far, the increase in oil price has not brought back the level of confidence to M&A activity that was expected, which is very apparent when looking at exploration opportunities. The industry has been and remains very cautious, but we expect with more robust 2022 budgets being set in the final quarter of 2021, that next year will be livelier. Meanwhile, the recovery in oil price has brought buyers and sellers closer in terms of deal value, after disconnected expectations in recent years. After a quiet 2020, the jury remains out as to whether the region is turning a corner, and, as analysts suggest, if 2021 will in fact be the ‘bumper year’ they predict.

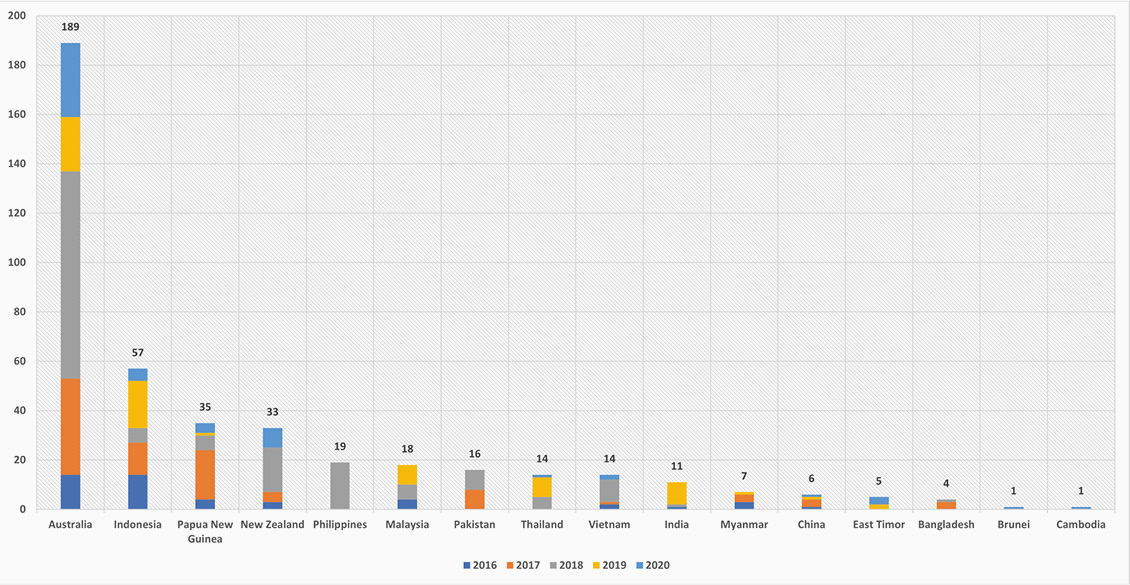

The graph below shows how Australia dominates the Asia-Pacific region, presenting the number of transactions Moyes has captured by block and not the dollar value between 2016 and 2020. It should be noted that deals completed in the likes of New Zealand and the Philippines tend to be relatively small in value with the threat of field abandonment costs driving value down. Despite 2020 being seen as poor in terms of deals done, the Moyes data shows it was in fact a better year than 2016. The busiest year in this period was 2018, thanks to over 80 permits being the subject of M&A activity in Australia. Transaction activity remains strong in Australia with its excellent fiscal framework, transparency, and ability to conclude deals quickly. Asian countries should take note of this if they wish to attract investment.

Asia-Pacific transactions: 2016–2020. Source: Moyes and Co.

With a lack of reliable data points in the region, it is hard to put a value on the opportunities available in the vast Asia-Pacific region. Estimates in the media range between US$10 to US$20 billion, with the opportunity of more significant packages being added notably by the major oil and gas companies. The ongoing divestment processes include ExxonMobil in Malaysia, Chevron in Indonesia and Australia, Shell in Malaysia and Indonesia, and ConocoPhillips in Indonesia. Lack of industry appetite has resulted in packages being taken off the table, and this includes ExxonMobil’s Bass Strait, offshore south-east Australia.

With such a large number of deals available, the question is who are the potential buyers? The majors are eliminating themselves as they are largely in retreat to ‘best-inclass’ with the odd exception. Private Equity has had its fingers burnt in the region, and we are not seeing the level of interest that these firms have in places like the UK offshore, which offer reserves and production in stable regimes. Special Purpose Acquisition Companies, or SPACs, which were launched as far back as 2011 in Malaysia with mixed success, could be new buyers in the market. The Asian National Oil Companies (NOCs) are potential players as they have pulled back their horns in the region after some have suffered disappointments ‘overseas’, and we may see more NOC partnerships develop. The local companies often struggle to find the funds required for bigger deals and to continue operations if these do not go to plan. Some of the more successful in securing deals are the ‘late life specialists’, as they are known. These include Jadestone Energy and Hibiscus Petroleum, and it will not be a surprise to see other niche players join them in the hunt for assets, particularly in the South East Asia part of the region.