South America’s upcoming floater projects could help sustain fabrication yards that are struggling to keep their doors open, with FPSO developments driven by Brazil and Guyana.

While the rest of the global oil industry copes with the consequences of the Covid-19 crisis, South America seems to be pulling through with announcements of major floating production, storage and offloading (FPSO) projects to be tendered. These projects should bring much-needed orders to fabrication yards that are struggling to keep their doors open. Approximately 40% of offshore deepwater and ultra-deepwater contracts to be signed in the next five years come from FPSO developments, driven by Brazil and Guyana, thanks to lower breakeven prices, thus promising major deals in the fabrication and subsea sectors.

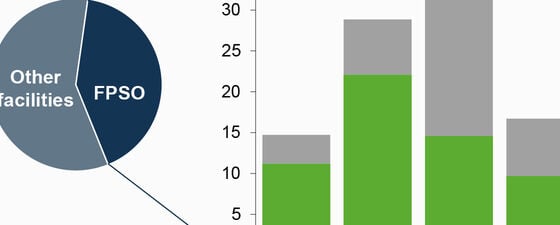

Offshore deepwater and ultra-deepwater contract awards between 2021 and 2025. Source: Rystad Energy ServiceCube, July 2020.

Fabrication jobs for floaters destined for Latin America have become a significant source of revenue for many yards, both local and international. Last year was remarkable as five out of nine global projects came from this continent. Winning contractors including Modec, SBM Offshore and Yinson have carried these prizes across the globe, offering jobs to yards in Asia. The projects awarded last year have resulted in $2.3 billion in construction and installation contracts, $2.6 billion in equipment contracts and $4.9 billion in contracts for subsea equipment, umbilicals, risers and flowlines.

The industry’s high expectations for 2020 were dashed by the double shock of faltering prices and demand, which has pushed many projects into the future. Major Latin American projects, including Equinor’s Bacalhau and Petrobras’s Mero in Brazil and ExxonMobil’s Payara in Guyana have been postponed, leaving few orders to compete over. Contractors have also been pressured to cut prices on ongoing contracts, adding to the challenges brought on by the dearth of new contracts.

Oil and Gas E&P in Latin America Bounces Back

Such a low level of activity was also seen in 2016, when no new floater-related contracts were awarded. However, the market was quick to bounce back with 12 new awards over the next three years. History should repeat itself as another 12 new awards are now lined up in just the next two years, representing close to $8.8 billion in construction, installation and equipment contracts and $8.5 billion in subsea contracts. Petrobras is in talks to finalize FPSO lease contracts for Mero 3 and Parque das Baleias and has already hit the market for new floaters to be deployed in the next phases of the Mero and Buzios pre-salt developments. In the long term, the state-controlled player is looking to deploy around a dozen FPSOs under the fourth phase of its pre-salt development plan, remaining a key driver for the world’s offshore sector.

While current orders will help yards stay afloat until the market settles down, South America will contribute significantly to the next wave of orders that will help these yards remain open in the future. Current low prices being offered in a very competitive environment should also incentivize operators to begin tendering processes and lock in these contracts before prices rebound.

Recent exploration awards in the Latin American region have also piqued the interest of the seismic and G&G (geological and geophysical) market, potentially attracting new surveys. However, activities are now moving at a cautious pace as many operators have cut back on exploration costs due to the downturn. This has not deterred seismic players like WesternGeco and CGG from planning multiclient surveys in Brazil’s prolific plays, given that operators are bound to return and resume exploration activities. Brazil’s National Petroleum Agency has also scheduled four licensing rounds in 2020 and 2021, indicating an improved environment for the seismic and G&G market in the coming years.