When Lord Cornwallis surrendered his British forces to the Yankees after the siege of Yorktown, ending the Revolutionary War, his band played ‘The World Turned Upside Down’ – an old English ballad of the day. Nothing could be truer for the US and Canadian domestic E&P community over the last year: a symbolic negative oil price blink, rig counts and production rates plummeting, a new US administration slapping moratoriums on federal land and waters while appointing ‘greens’ to high positions. In Canada, a liberal government, now emboldened by newly aligned policies south of the border, continues to invoke the ire of Alberta with restrictive measures. Meanwhile Texas, the energy capital of the world, is shivering in the dark, just like those bumper stickers told New Englanders to do a couple of decades ago. Traditional producers touting carbon-neutral barrels sold and endorsing a carbon market. All in all, an upstream world turned upside down.

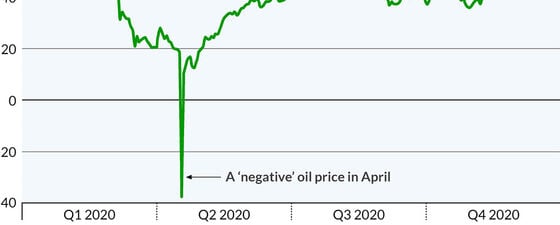

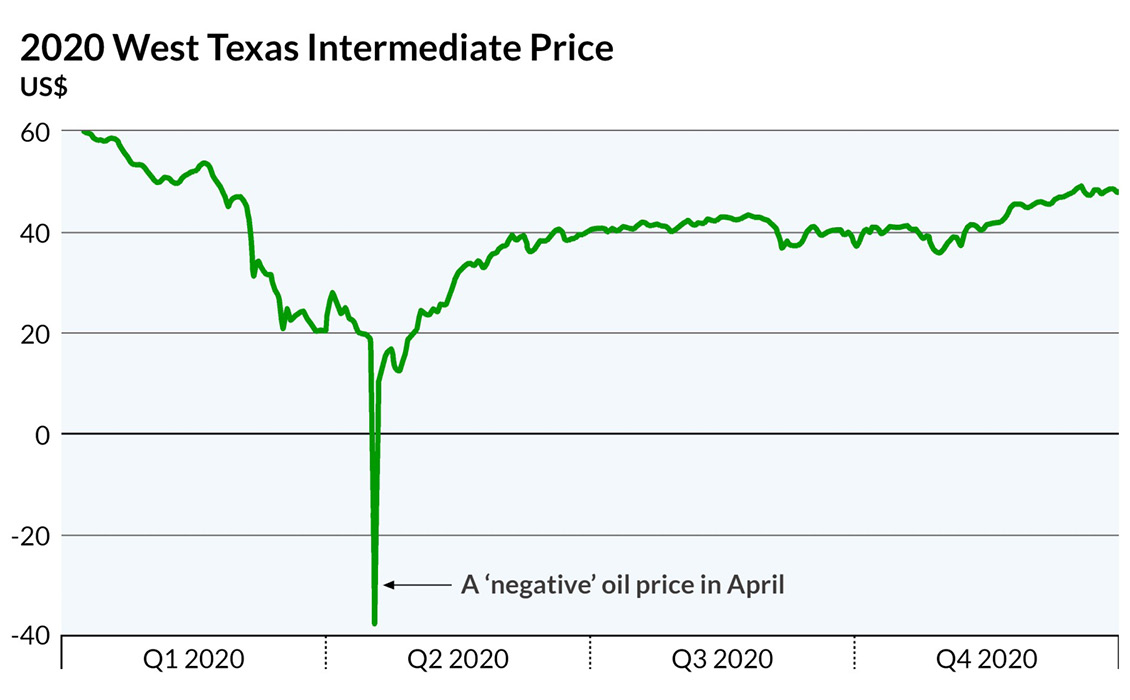

West Texas Intermediate Oil Price, 2020 showing negative oil price as the future contracts for May delivery tumbled to minus $37.63 a barrel. © NVentures.

The US and Canadian domestic upstream business has weathered many a calamity in the past, like the price shocks of Spindletop, the Depression, supply gluts and supply squeezes from overseas, and the ‘shale glut’. The vibe in upstream these days is different, however. It evokes the ‘end of oil’ debates brought on by Hubbert’s peak oil research of the mid-1950s and resultant majors’ (now obviously) premature efforts to diversify. This time, however, the threatened end to life as the upstream knows it, is anthropomorphic, not ‘natural’. There is plenty of oil and gas left to produce with ever-improving technology, but a heightened concern for how long demand will support this major industry. The upstream vibe is not, however, predominately doom and gloom. Upstream has the most brilliant and positive people of any industry who see challenge and opportunity in the events of the past year, as much as problems and obstacles. The shale ‘revolution’, enabled by innovation within this community, demanded unprecedented adaptation in domestic US and Canada, more than anywhere else on Earth. Geoscientists and engineers were defiantly able to meet these challenges. A looming ‘end of carbon’ moniker will not defeat this crowd.

So the past year has seen a strident move from the largest major to the smallest independent to cut carbon emissions in production and transmission and to rapidly ramp up investing in and co-venturing with start-ups in direct air carbon capture and sequestration through injection (a proven technology for enhanced oil recovery) and subterranean mineralization. Additionally, investment has been made in planning for a nationwide network of CO2 pipelines from capture points to injection points and investment in new geothermal technology to increase the applicability of this technology. Other initiatives include ‘solarizing’ power generation for upstream facilities and leverage offshore technology by moving into offshore wind farms. To follow the lead from Europe, majors are also investing in Green Hydrogen in a much more substantive way. Perhaps most significantly, major oil companies are now advocating carbon trading, possibly with a view that this will be a new profit center with all the technology they can bring to bear.

And of course, with all this adaptation through resilience and innovation, activity continues. In conventional action, a busy winter drilling campaign started on Alaska’s north slope by Australian and UK independents, 88 Energy and Pantheon, based on wonderful sequence stratigraphic work in Cretaceous traps with some quick success. This is tempered, however, by further major exits (BP, Shell), a legal impediment to ConocoPhillips’ development work, and a lackluster showing in the last lease sale of the previous administration in the leasable portion of the Arctic National Wildlife Refuge. In the deepwater Gulf of Mexico, operators are keeping a few exploratory wells going, including Kosmos touting their short-cycle, infrastructure-led exploration near existing facilities in oil prone areas, but offshore Labrador-Newfoundland activity has ground down to bare-bones development work. On a closing note to activity, the super-resilient shale movement is holding firm in activity and production across the board, with at least talk of higher efficiencies and murmuring the old refrain “Lord, please let there be another boom … I won’t mess up again.”