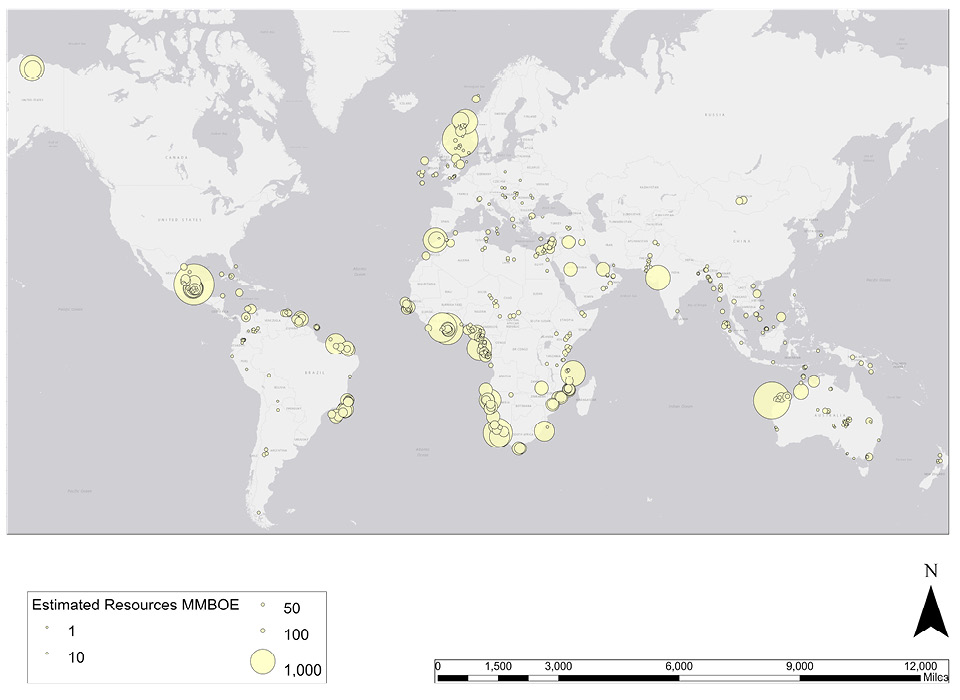

The extended impact of uncertain oil prices, combined with the Covid-19 pandemic and dwindling investor sentiment for hydrocarbons, have affected the exploration drilling scene in 2021, with a number of already deferred wildcat wells being further delayed and, in some cases, shelved. Notwithstanding the overall sentiment, 2021 had some significant exploration successes and early 2022 has followed strongly. A global review of wells to watch by reserves added (see map) indicates strong potential in the Gulf of Mexico, Atlantic margins of South America and western and southern Africa, North Sea (UK / Norway), eastern Mediterranean, west coast India, and Australia’s North West Shelf (NWS). Onshore, significant reserves increases are possible in Kurdistan, Saudi Arabia, UAE, North Slope Alaska and eastern Africa.

The deadline to net zero committed to by various countries and companies, will in some cases preclude exploration in frontier basins, as the timeframe from basin evaluation through prospect maturity and drilling – to development and production – will be simply too long. While deepwater prospects drilled by the majors and larger NOCs stand most chance of adding significant reserves, there is a strengthening interest in targeting onshore, shallow water and infrastructure-led exploration prospects in emerging or mature basins and junior players are showing their niche abilities here.

Global wells to watch by estimated reserves. © NVentures.

Drilling deferrals from 2020 continued into 2021, such that some long-awaited wildcats such as TotalEnergies’ Venus-1 well in Namibia and OVL’s Kanchan-1 in Bangladesh are still ongoing in early 2022, and their outcomes are keenly awaited. Early 2022 is expected to see the spud of high-impact wells Apus-1 and Pavo-1, in NWS Australia, targeting the Triassic Dorado trend. Meanwhile, Sasanof-1 is planned near the giant Scarborough gas field, also in NWS Australia and Timpan-1 is scheduled in the North Sumatra Basin, Indonesia. In the eastern Mediterranean, there is no news on timing for the TotalEnergies planned Block 9 Lebanon well and Energean’s Zeus prospect offshore Israel is still in the planning stage. São Tomé and Príncipe will host its inaugural exploration well with Shell and Galp, Jaca-1, in Block 6 in the deepwater west of Equatorial Guinea. Several wildcats are planned for Guinea Bissau and Ghana in the West Africa margin, with relatively little activity in the onshore basins.

Guyana and Suriname continued to build on a notable run of exploration successes in 2021, particularly in the sweet spot of the Stabroek block offshore Guyana, with Longtail-3, Whiptail-1 and -2 and Cataback-1 all proving additional oil reserves in deeper Cretaceous targets and continuing into 2022 with Fangtooth-1 and Lau Lau-1. In Suriname, TotalEnergies are drilling Krabdagu-1, on trend with previous successes in the block, despite disappointment with Bonboni-1. Other appetites remain lukewarm, with Tullow planning to exit Suriname, having had a presence there since 2007.

While reserves additions in the Asia-Pacific region are relatively modest, the drilling success rate throughout 2021 was between 50–60%, reflecting the maturity of the region but also the appeal of lower risk, higher return, exploration.

Turkey’s 2020 Black Sea discovery, Sakarya, underwent various follow-up exploratory and appraisal operations, all of which appear to have increased reserves and highlighted the Black Sea potential, though possibly aggravating geopolitical issues in the region.

Despite a shortening timeline for the future of exploration, as the energy transition gathers pace, several countries are starting 2022 with bid rounds ongoing or opening. The appetite for companies’ exploration dollars and commitments remains. If this can generate a spate of discoveries like those of early 2022, the health of the industry is more robust than it is generally presented.

Author: Madeleine Slatford, NVentures

Author: Madeleine Slatford, NVentures