The two major northern European oil and gas producers appear to be on slightly different trajectories when it comes to their approach to future exploitation of their continental shelves.

APA 2021

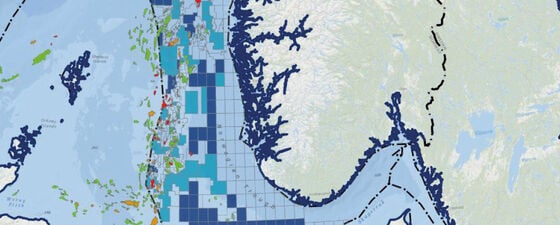

Norway APA 2021 North and Norwegian Seas. Credit: NVenturesIn Norway this year, the Ministry of Petroleum and Energy launched the annual licensing round, seeking bids for mature areas in the Norwegian Continental Shelf (NCS). The country’s Awards in Predefined Areas 2021 (APA 2021) licensing round offers oil companies a total of 84 blocks located in the North Sea and the Norwegian and Barents Seas. The round included new blocks south-east of Bear Island, halfway between the Arctic Svalbard Archipelago and mainland Norway. Norway introduced the predefined area rounds in 2003 to promote exploration in the most geologically known parts of the Norwegian continental shelf and has expanded the predefined areas with each round.

Norway APA 2021 North and Norwegian Seas. Credit: NVenturesIn Norway this year, the Ministry of Petroleum and Energy launched the annual licensing round, seeking bids for mature areas in the Norwegian Continental Shelf (NCS). The country’s Awards in Predefined Areas 2021 (APA 2021) licensing round offers oil companies a total of 84 blocks located in the North Sea and the Norwegian and Barents Seas. The round included new blocks south-east of Bear Island, halfway between the Arctic Svalbard Archipelago and mainland Norway. Norway introduced the predefined area rounds in 2003 to promote exploration in the most geologically known parts of the Norwegian continental shelf and has expanded the predefined areas with each round.

The deadline for interested companies to submit their applications was 8 September 2021, with the government aiming to award new production licences during the first quarter of 2022. Although the expected size of discoveries from the mature areas is smaller, they could be feasible and profitable when developed in conjunction with other discoveries and by utilising the existing, or planned infrastructure. This latest round has attracted bids from 31 oil companies including Equinor, Aker BP, ConocoPhillips, and Lundin Energy among others.

The Norwegian government is under harsh attack from environmental organisations, as well as a growing number of foreign countries, for its continued drilling in Arctic waters. 70 of the 84 blocks are in the northern Barents Sea. At the end of 2020, Norway’s supreme court approved government plans for oil exploration in the Barents, rejecting a lawsuit by environmental groups who claimed the oil licences breached an article in the Norwegian constitution and would also be contrary to the 2015 Paris climate accord.

Despite the increasingly vocal environmental lobby in Norway, it remains the case that the government’s expected total net cash flow from the petroleum industry in 2021 is huge, estimated at NOK 154 billion. (US$18 billion). Total employment in the petroleum sector was around 200,000 in 2019, which, for a population of around 4.5 million, remains significant. The export value of hydrocarbons in 2020 was 42% of the total of Norway’s exported goods, which highlights the continuing importance of the industry.

Recent parliamentary elections in Norway resulted in a decisive victory for the centre-left opposition and Labour is now expected to lead the next government, which is likely to be formed in mid-October. It is therefore likely that they would be responsible for making the eventual awards of acreage early next year. The Labour Party has said that any transition away from oil will be gradual and that in the meantime exploration for oil and gas will continue.

In the United Kingdom, the other major player in this industry, the Government in September last year carried out a review of the policy on oil and gas licensing to ensure it was compatible with its climate change objectives. Accepting the continuing role of oil and gas on its path to net zero, the British Government will introduce a new Climate Compatibility Checkpoint on future oil and gas licensing rounds to ensure they are compatible with wider climate objectives, including net zero emissions by 2050. This checkpoint will use the current evidence at the time, considering the UK’s demand for oil and gas, projected production levels, increasing prevalence of cleaner technologies such as offshore wind and carbon capture, and the sector’s continued progress against its emissions reduction targets. The Department for Business, Energy and Industrial Strategy (BEIS) has stated that design of this checkpoint will be completed by the end of 2021.

In parallel, the Offshore Petroleum Regulator for Environment and Decommissioning is conducting a new Offshore Energy Strategic Environmental Assessment which will underpin future licensing rounds. The Oil and Gas Authority (OGA) will run another licensing round for oil and gas exploration on the completion of this assessment.

32nd Offshore Licensing Round

UK 32nd Offshore Licensing Round. Credit: NVenturesIn the meantime, the 32nd Offshore Licensing Round, launched in July 2019, resulted in the OGA offering for award 113 licence areas over 260 blocks or part-blocks. This round offered blocks in mature, producing areas close to existing infrastructure, under the flexible terms of the Innovate Licence which enables applicants to define a licence duration and phasing that will allow them to execute the optimal work programme.

UK 32nd Offshore Licensing Round. Credit: NVenturesIn the meantime, the 32nd Offshore Licensing Round, launched in July 2019, resulted in the OGA offering for award 113 licence areas over 260 blocks or part-blocks. This round offered blocks in mature, producing areas close to existing infrastructure, under the flexible terms of the Innovate Licence which enables applicants to define a licence duration and phasing that will allow them to execute the optimal work programme.

There were 104 from 71 companies ranging from multinationals to new country entrants. Most of the licences will enter the Initial Term (Phase A or Phase B exploration stage), and 16 of the awards are for licences that will proceed straight to Second Term, either for potential developments, or redevelopments of fields where production had ceased, and the acreage had been relinquished.

No Further Licensing Rounds in Denmark

At the other end of the spectrum, Denmark (a producer since 1972) has introduced a cut-off date of 2050 for oil and gas extraction in the North Sea and has cancelled all future licensing rounds. Last year a broad majority in the Danish Parliament reached a deal on the future of oil and gas production in its waters, leading to the cancellation of the 8th licensing round and all future rounds. The deal also establishes a final phase-out date for hydrocarbon extraction by 2050, outlining plans for a transition of impacted workers. Denmark is currently the largest oil producer in the EU and will now become the biggest producer worldwide to establish a final phase-out date. Other countries to have done so all produce significantly less oil and gas than Denmark.

Denmark is a long-time leader in wind energy and a prominent exporter of wind turbines, with wind now producing over 40% of Denmark’s total electricity consumption. Their direction of travel is clear.