Image: jroballo via Adobe Stock.

When the lithium cycle bites back

Why are prices rallying in China at the start of 2026?

Commodity cycles rarely announce their turning points. They emerge quietly, through inventory data, project pipelines, and subtle shifts in physical markets – long before consensus catches up. The lithium price rally unfolding in China in early 2026 fits this pattern. It’s almost like a textbook.

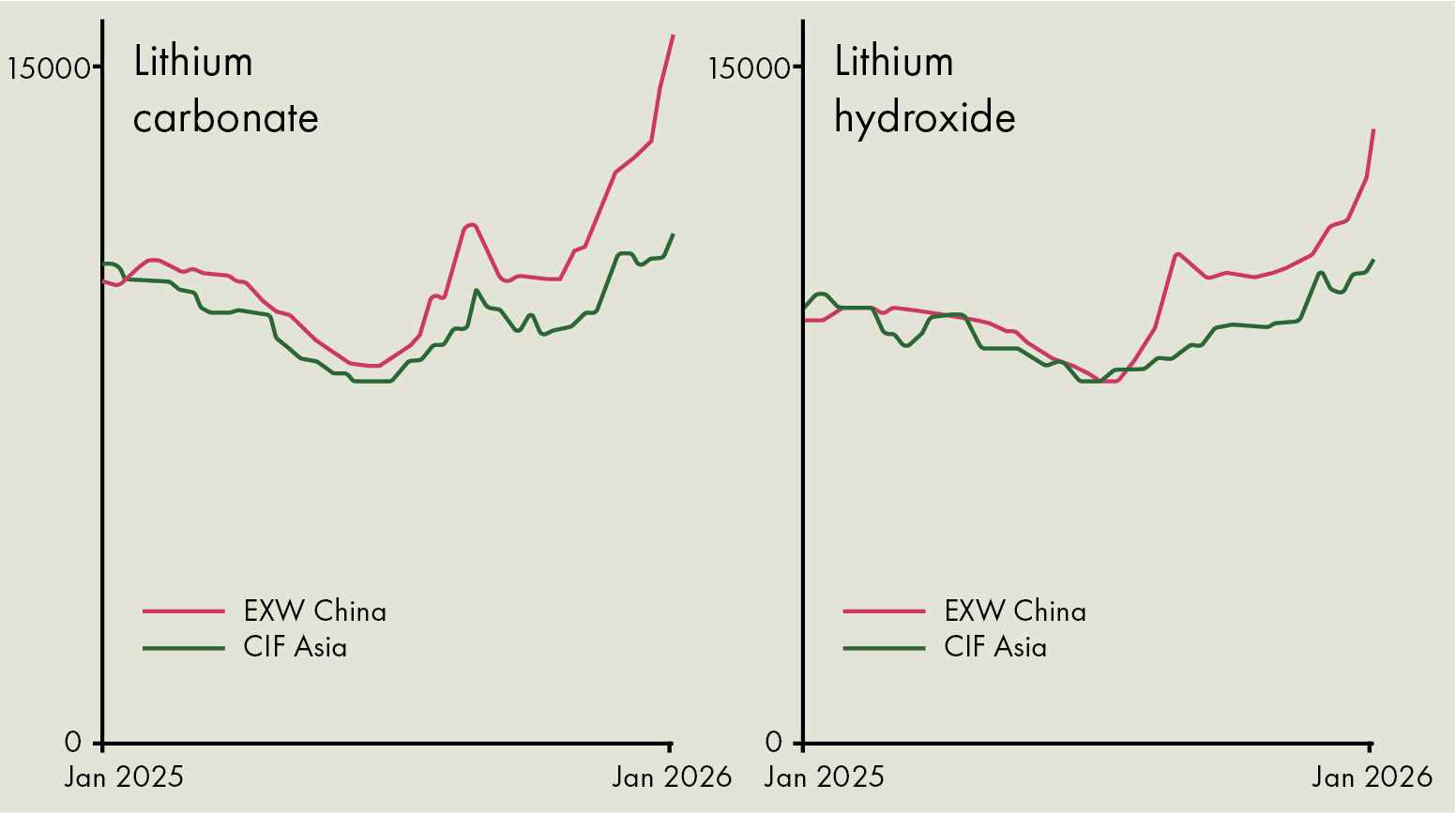

What looks, at first glance, like a sudden spike in lithium carbonate and hydroxide prices is in fact the delayed response of a system that has been quietly tightening for more than a year.

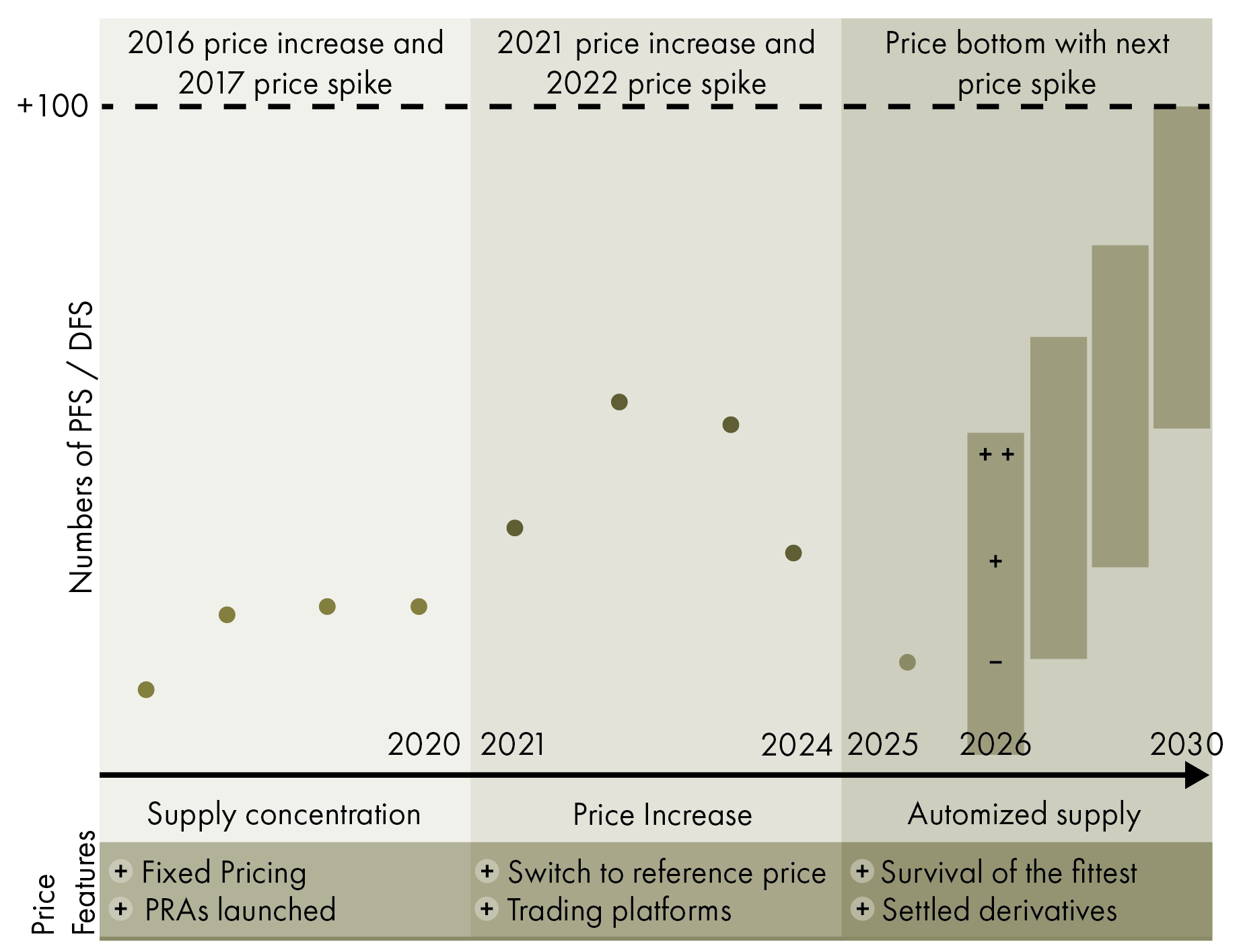

Based on SCI (Figure 1) and Benchmark Intelligence data (Figure 2), the most important early warning came from project development information. During the 2021- 2023 boom, more than 50 lithium projects globally progressed to feasibility studies. Following the sharp price correction of 2023-2024, that pipeline collapsed. By 2025, the number of feasibility studies and Final Investment Decisions had fallen to historic lows. Capital withdrew, boards delayed sanctioning, and the industry effectively chose to wait out the downturn.

For lithium, this decision carries structural consequences. Even the fastest lithium developments – brines, brownfield expansions, or DLE pilots – require several years to reach commercial scale. When feasibility work dries up, future supply is quietly removed from the system. The impact is not immediate, but it is inevitable.

While investment stalled, demand did not disappear. Battery-grade lithium carbonate and hydroxide continued to be consumed by electric vehicles, energy storage systems, and industrial users. According to market data, inventories in China have been steadily drawn down since September 2025 and entered 2026 at their lowest levels of the year. Once inventories thin, the market’s behaviour changes. Prices no longer move gradually; they react sharply to even marginal shifts in sentiment or procurement.

Crucially, the price recovery did not require a surge in demand. It only required the demand to stop falling. By late 2025, EV growth in China stabilised, energy storage deployments absorbed additional carbonate volumes, and downstream players shifted from destocking to cautious restocking. In a market already stripped of inventory buffers, that was enough to trigger a rapid repricing.

From an energy-geologist’s perspective, the current lithium rally looks less like a surprise and more like a delayed inevitability. The industry responded rationally to low prices by cutting investment. The subsurface responded, as it always does, by refusing to accelerate on demand.

Lithium, like oil, copper, or uranium, are reminding markets of a fundamental rule: You cannot shortcut time in the subsurface / sanction supply retroactively. By the time prices signal scarcity, the development gap is already locked in, and when that reality finally shows up in inventories, prices move first and fast. Questions get asked later.