Rebound in Africa?

Encouragement that we may see a modest rebound in Africa as we go into the final quarter of 2021 with Egypt and Angola leading the charge in M&A activity.

The lack of in-person conferences and ability to have face-to-face meetings has certainly slowed down deal-making globally. However, there is encouragement that we may see a modest rebound in Africa as we go into the final quarter of 2021 with Egypt and Angola leading the charge.

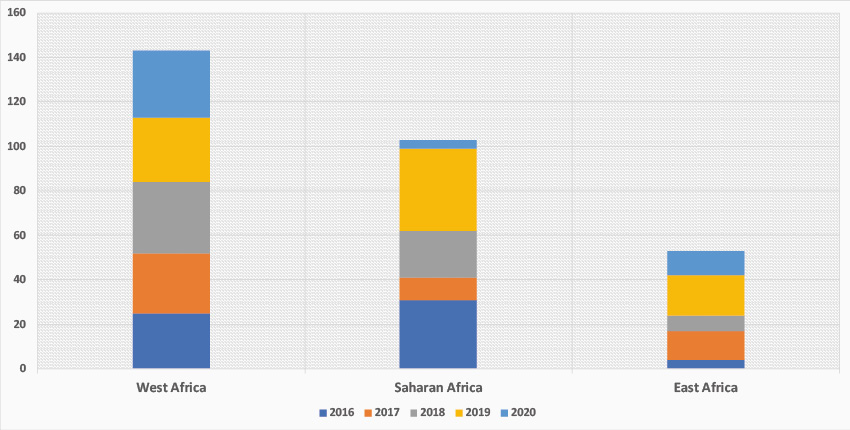

There are different ways to measure M&A activity and we have used individual block count from the Moyes transaction database for the period 2016 to 2020. As can be seen on the graph, West Africa dominates and generally activity has been quite steady in this sub-region. Saharan African saw a significant drop in 2020 after a blockbuster 2019. This spike in 2019 can be explained by several deals done in Egypt. Buyers of the Egypt assets include Pharos Energy, Dragon Oil, Noble Energy, BP and United Oil & Gas. Activity in East Africa, the quietest of the sub-regions in this period, was also boosted by a busy 2019 with Kenya and Mozambique seeing deals going over the line.

A word of caution! It should be noted that while deals are recorded as being completed in 2019, the incubation period may have been over the prior years, when much of the hard work and decisions would have taken place. There is a time lag that will give the impression of certain years being busier than they actually are, or vice versa.

Looking in more detail at the period 2016 to 2020 (and to date in 2021), most M&A activity reported has taken place in Egypt, which can be considered the region’s hot spot. This is followed by the hydrocarbon-producing countries of Angola, Nigeria, Tunisia and Gabon. Most of the transactions seen in Africa involve production, development, or low risk appraisal assets.

Africa: Transactions by Block: 2016–2020. Credit: Moyes & Co.

Exploration M&A activity has been slow, although the Orange Sub-basin, which straddles the Namibia – South Africa border, will play host to three high-impact exploration wells within the next nine months. These are TotalEnergies’ Venus-1, Shell’s Graaf-1 and Azinam’s Gazania-1. All the upcoming wells will test different plays within the frontier province. Success in any of these will encourage M&A activity within the Late Jurassic to present-day sub-basin where several partnering opportunities are currently open.

By some distance, TotalEnergies has been the biggest investor in the African region as its focus has shifted from other parts of the world such as Asia-Pacific. Other players that continue to move forward in the continent include Eni and Qatar Petroleum (QP). Stateowned QP is a partner in almost all the upcoming high-impact wells in Africa through partnerships with Eni, ExxonMobil, TotalEnergies and Shell.

Private Equity (PE) firms have largely focused on countries where they are comfortable with above-ground risk such as the UK, USA, Canada and Australia. In Saharan Africa, Egypt has attracted private equity investment such as the Carlyle and CVC Capital-backed Neptune Energy, which acquired assets from Engie E&P. While in West Africa, the Carlyle-backed Assala Energy acquired Shell’s onshore assets in Gabon, and the Warburg Pincus-backed Trident Energy acquired Hess’s offshore interests in Equatorial Guinea.