Pandemic Affects Oil and Gas Licensing Plans

The upstream part of the oil and gas industry has been particularly disrupted with the global impact of the pandemic massively reducing the demand for oil and gas during 2020 – resulting in an almost unprecedented collapse in exploration activities globally.

A worldwide pandemic impacts all aspects of life and over the last 18 months the oil and gas business, as well as all other industries, has had to adapt. The upstream part of the industry has been particularly disrupted with the global impact of Covid-19 massively reducing the demand for oil and gas during 2020. The resultant fall in the oil price has produced an almost unprecedented collapse in exploration activities globally. Although we are now seeing a rebound in prices due to OPEC+ production limits and drawdown of stored oil supplies, hydrocarbon licensing – the ground-floor driver of exploration for new reserves – remains disrupted, if not stalled.

Governments use considerable human resources and capital to organize licensing rounds, whether it be in mature or frontier basins. Data packages which underpin these licensing activities include expensive items such as 2D and 3D seismic and other datasets and crucially the timing of the announcement of the round must be at the optimal moment to maximize the likelihood of sufficient bidding interest.

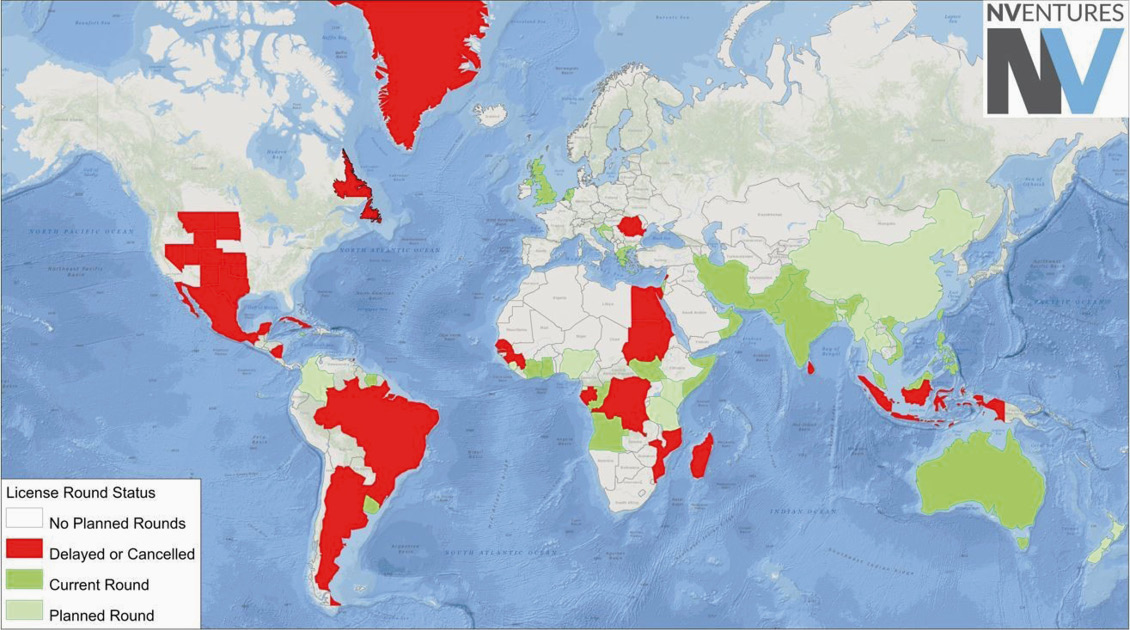

Licensing round status 2021.

Predicably during the pandemic, we have witnessed a decline in the number of licensing rounds and delays in several already announced. If we look at the countries which have delayed or rescheduled rounds, we note nations such as Senegal or Brazil which have prospective, but deepwater environments or others like Sudan and Lebanon, which remain relatively underexplored. In all cases, the potential exploration opportunities in these areas are attractive but expensive, and it is not surprising that governments have delayed deadlines in the hope of a market recovery. Overprinting all of this uncertainty is an accelerating energy transition, which means, for example, that some IOCs (or IECs) have mandated no new exploration in countries where they do not already have a footprint.

As we navigate our way out of the current crisis, it is highly probable that we will witness fewer rounds with smaller acreages on offer, requiring higher investments and some countries may see a switch from competitive bidding to direct negotiations. For 2021, rounds that will be important as barometers of exploration interest will include Malaysia and Egypt. Another major event will be Brazil’s 17th offshore licensing round, scheduled for October 7.