Private Equity Firms Drive UK Oil and Gas Activity

Despite a drop in new exploration and appraisal drilling in the UK offshore sector, the industry remains very buoyant compared to other parts of the world.

Since the first hydrocarbons were produced on the UK Continental Shelf at BP’s West Sole gas field in 1967, there have been many prophecies of when production from the province would eventually end. To use that well-known phrase from the oil industry, ‘it is a hydrocarbon province that keeps on giving’.

With such prolific source rocks, notably in the Jurassic and Carboniferous, we can expect more surprises in the offshore basins. The industry can also expect many oil and gas fields will outlast their prognosed depletion dates and be the subject of redevelopment in the future.

Despite a drop in new exploration and appraisal drilling in the UK offshore sector, the industry remains very buoyant compared to other parts of the world. Bid rounds continue to be healthy with new block awards, and we also see robust deal flow. London itself has taken over from Houston as the global hub for international oil and gas deals.

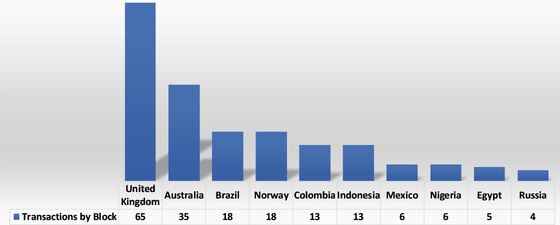

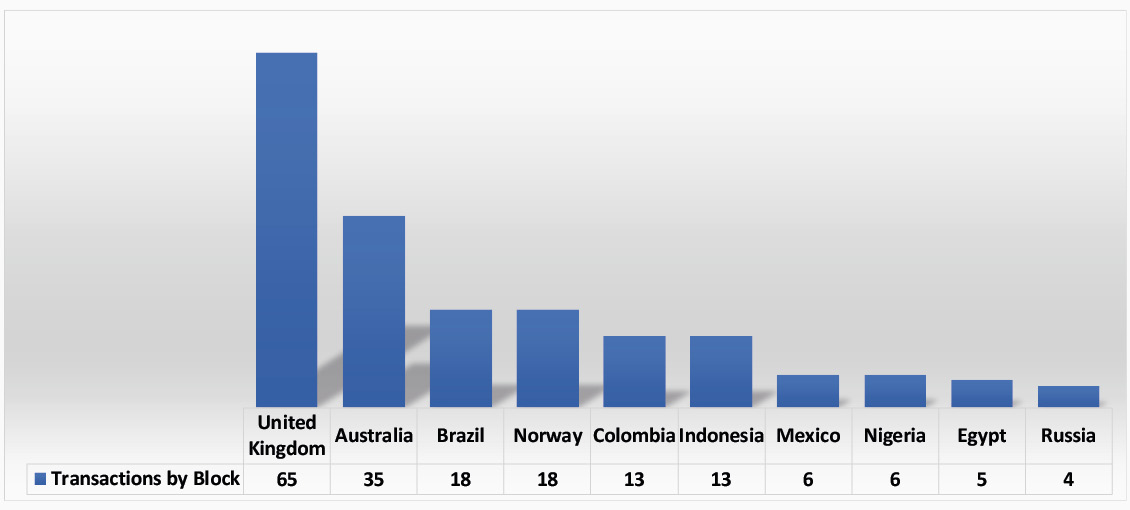

Figure 1: Global oil and gas transactions, 2016–2020.

Figure 1 shows the number of contract areas which have been the subject of a transaction between 2016 to 2020. The UK has been the most active place in the world outside of North America with 2018 and 2020 being the busiest years in the UK. Much of this has been driven by Private Equity (PE) involvement which started its drumfire in 2015.

The main PE firms are the Carlyle Group, HitecVision, Quantum Energy Partners, Blackstone Group, CVC Capital Partners, Blue Water Energy, Kerogen Capital, Riverstone and EIG Partners. Oil companies backed by these firms include Siccar Point, Chrysaor (now Harbour Energy), Neptune Energy, NEO Energy and Waldorf Production.

In addition, there are numerous divestment opportunities available in the UK offshore. In fact the UK has the second largest number of upstream opportunities available in the 2018–2021 period after Australia. This highlights the competition companies face when seeking farmout partners or the sale of assets in the UK.

The quality of technical work on these assets for divestment is extremely high, and is combined with positive government energy policies managed by the Oil and Gas Authority (OGA).

Success in several high-profile wells scheduled in 2021 will increase interest in a number of these divestment opportunities. These include Shell’s Edinburgh Prospect in the Central North Sea and its Pensacola Prospect on the Mid North Sea High, and Equinor’s Tiger Lily Prospect in the Central North Sea.

Despite the mature nature of its fields, the UK still generates a lot of cash, making it attractive to investors with break-even in the US$30 to US$50 range. We see deal flow continuing to be very active going forward, but with the pool of buyers getting smaller, capital is going to fight for good trade terms. It also remains to be seen what the exit strategy is for PE firms, or will they stay and maintain their cash flows?