Unconventional Oil and Gas in Mexico

Mexico’s Tampico-Misantla Basin is potentially one of the richest unconventional oil and gas resources in the world. The development of these resources could significantly increase Mexico’s daily production of oil and gas, and bring in enough income to rejuvenate the national oil company, PEMEX, and help get the economy back on its feet.

Mexico’s Tampico-Misantla Basin is potentially one of the richest unconventional oil and gas resources in the world, with reserves of at least 90 Bbo and 40 Tcfg. Development of these resources could significantly increase Mexico’s daily production of oil and gas, bringing in enough income to rejuvenate the national oil company, PEMEX, and help get the economy back on its feet. Perplexingly, little is being done to bring these resources into production.

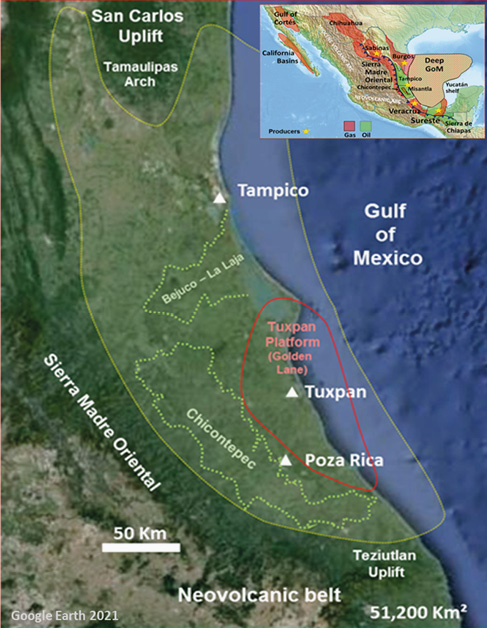

Figure 1: Mexico’s oil and gas basins. Tampico-Misantla is one of only two that produce oil.

The Tampico-Misantla Basin

The Tampico-Misantla Basin is in east-central Mexico, bounded by the Tamaulipas Arch in the north, the Gulf of Mexico in the east, the Neovolcanic Axis and Teziutlán uplift in the south, and the Sierra Madre Oriental Fold Belt to the west.

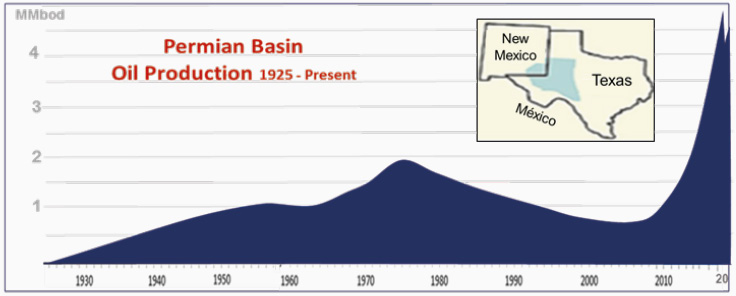

In 2016, IHS Markit analysts developed the super basin concept and proposed the Permian Basin of West Texas and Eastern New Mexico as the epitome of a super basin. They also identified the Tampico-Misantla Basin as a super basin that has very similar characteristics to the Permian Basin, recognising it as an excellent candidate for rejuvenation (Fryklund and Stark, 2020; Sternbach, 2020; Guzmán, 2021).

The Permian Basin started production in the 1920s from reef- and shelf-limestone reservoirs that rim the Delaware and Midland Sub-basins. It reached 2 MMbopd production in the mid-1970s, declining steadily thereafter until by 2010 output had declined to less than 1 MMbopd, when the advent of horizontal drilling with multiple hydraulic fractures allowed oil and gas to flow economically from silts and shales previously overlooked as producible reservoirs. This resulted in exponential production growth that in only 10 years reached a staggering 4.8 MMbopd and 18 Bcfpd. In 2020 the Covid-19 pandemic hampered growth, but by early 2021 it had resumed, albeit at a slower rate. The basin’s resource estimate of 30 Bboe in the early 2000s was reassessed in 2018 to be 150 Bboe recoverable.

Tampico-Misantla has four main conventional oil plays that were the focus of upstream activity in Mexico until the 1980s. The first reservoirs were discovered in the early 1900s in fractured carbonates of the prolific Ébano-Pánuco-Cacalilao Province west of Tampico, followed a few years later by the Golden Lane to the south. In the 1930–40s the Poza Rica trend and the southern extension of the Golden Lane were discovered, followed by the offshore Golden Lane and Jurassic reservoirs in the 1950–60s. In the 1960–70s low permeability sands in Chicontepec were tested at the same time as similar rocks of the Spraberry Formation in the Midland Basin were beginning to be developed. As production started from oil shales in the USA, in 2010 Mexico began successfully evaluating the rich organic shales and marls of the Tithonian and Turonian. The Kimmeridgian and Oxfordian marls, rich in mature organic matter, also appear to have production potential.

Figure 2: Rejuvenation of the oil production of the Permian Basin. Source: EIA, IHS Markit.

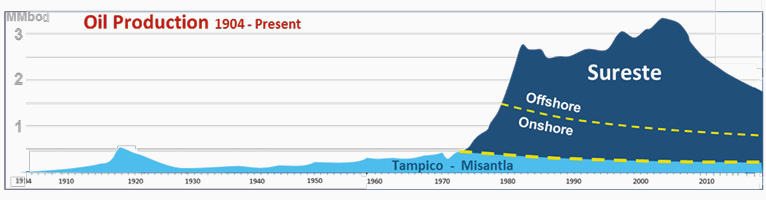

From 1975 to 1982, following the discovery of oil in the Mesozoic of the Sureste Basin, oil production grew from 0.5 to 2.7 MMbopd and reserves increased from 6.3 to 72.5 Bboe. As a result of this success, the authorities decided that there were sufficient oil and gas reserves to sustain output for at least 25 years and reduced the NOC exploration budget from approximately US$2 billion in 1981 to $400 million by 2001, concentrating most of the resources in the Sureste Basin.

Tampico-Misantla, where the fields were entering a mature stage, wells were less productive and producing oil from tight rocks was much more expensive, was all but abandoned and has had little further exploration.

Times Change

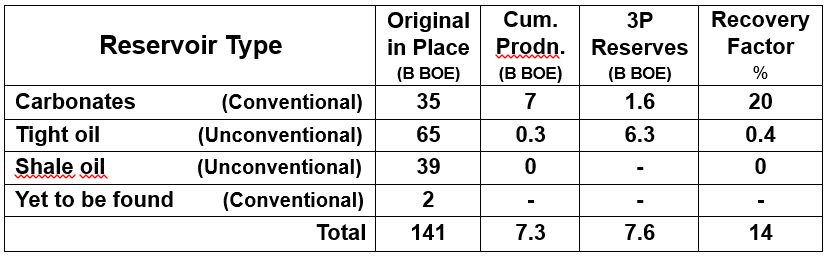

Circumstances have changed, however. Today the Sureste Basin has few undeveloped reserves, no unconventional resources, and although there is good potential for yet-to-be-found reservoirs, these are elusive with new discoveries requiring expensive facilities. By comparison, the total resources in the Tampico-Misantla Basin are huge (Table 1), with unconventional in-place resources estimated to be over 100 Bboe and in similar reservoirs to those that allowed the Permian to multiply its oil output sixfold in less than ten years. Not only do the two basins have similar reservoirs but they also have similar resource volumes. These unconventional resources are in relatively shallow reservoirs and can be developed as economically as conventionals – faster, more easily and with less geologic risk.

Table 1: Oil and gas resources of the Tampico-Misantla Basin. (National Hydrocarbon Commission).

Chicontepec Tight Oil Play

The richest and easiest resource to develop is the tight oil in the foredeep fill formed by the Sierra Madre uplift that was incised in the Late Palaeocene – Early Eocene by a long (120 km by 25 km) paleo-canyon named Chicontepec. A similar feature, the Bejuco-La Laja paleo-canyon formed in the north side of the Tuxpan Platform (Figure 1).

Earliest drilling in Chicontepec took place in 1926, but the wells had low productivity and there was little interest in their development, although a few isolated wells went into production in the 1940 and 1950s. In the late 1970s, interest was renewed by improved productivity and some scattered reservoirs were developed. Initial flow rates were highly variable and declined rapidly, so the wells needed to be fracture-stimulated to be able to flow or pump at commercial rates and were directionally drilled from central locations to minimise environmental impact and produced into centralised facilities. Oil gravities in the paleo-canyon vary from very light in the north (> 40° API) to very low in the south (10° API).

Between 40 and 90 wells a year were drilled in Chicontepec between 1973 and 1982, raising the output to over 12,000 bopd. In 1978 DeGolyer and Macnaughton certified the reserves, reporting that the paleo-canyon had 106 Bbo in place. All 29 fields were determined to belong to a single, contiguous giant oil field covering over 3,000 km2 and at the time it was considered that over 16,000 wells would be needed to develop the field, with 11 Bboe being recoverable.

Production Crisis

Oil production in Mexico during this period was less than 0.5 MMbopd, insufficient for the country’s needs, so Chicontepec appeared to be a solution, but just before the project was started the highly productive giant oil fields of the Sureste Basin were discovered, and all the available resources were dedicated to developing these. Over the next 30 years, small efforts were made to develop Chicontepec, and some of the reservoirs with better permeabilities came on stream despite their low productivity, including the Soledad-Coyotes, Miquetla, Agua Fría-Coapechaca-Tajín, and Presidente Alemán fields.

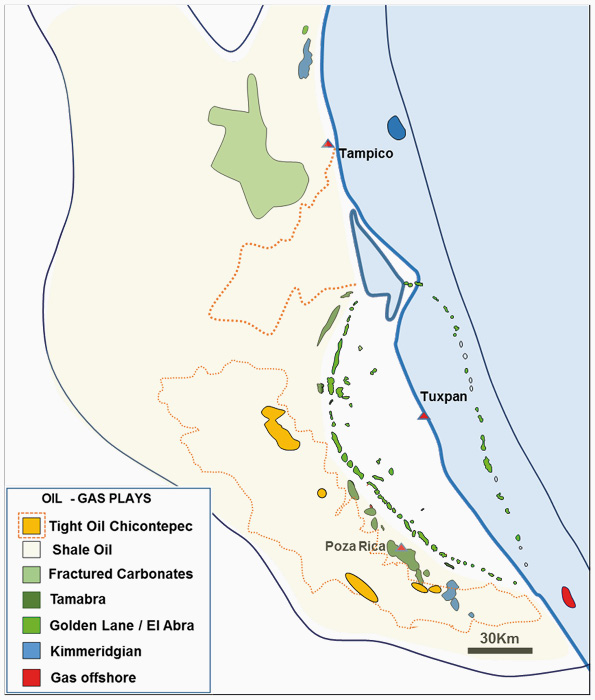

Figure 3: Legacy and unconventional plays of the Tampico-Misantla Basin. Source: National Hydrocarbon Commission.

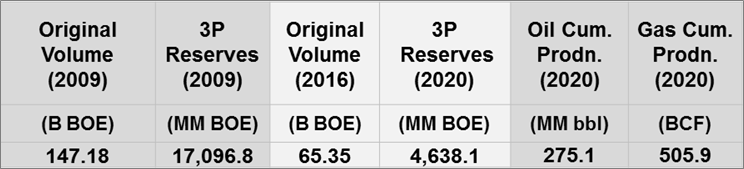

In the early 2000s a new attempt was made to fully develop these reservoirs. Their volumes were recertified by both DeGolyer and Macnaughton and Netherland and Sewel, who confirmed the order of magnitude of the volumes certified 30 years earlier. Better drilling and completion techniques were applied, such as commingling, larger hydraulic fractures, PDC bits, better subsurface models and more efficient facilities. This new effort was predicated on a certified resource base of 137.3 Bbo in place and 63 Tcfg and 17.1 Bboe of 3P reserves.

Output increased from a few thousand bopd to over 30,000 bopd over a short period and supported a 10-year plan that recommended an extensive drilling campaign to raise production to over 600,000 bopd. The Chicontepec Integral Project became very important as the offshore Cantarell field (2.2 MMbopd) had started declining (and with it, Mexico’s oil production) and the only important undeveloped reserves that could replace the lost production were offshore Campeche in Ku-Maloob-Zaap with 10–12° API oil – and Chicontepec. The over $60.00/bo break-even cost and enormous CAPEX requirements remained a challenge, but at the time the oil price was soaring and, after a slow start, Chicontepec output increased to more than 70,000 bopd. But when the oil price collapsed in 2008, the government decided to suspend production.

Technology Opportunity

When the price started to recover and the technologies to extract oil from low permeability rocks at economic rates became a reality, a new attempt to develop Chicontepec was made, this time through what were termed Integral E&P Contracts (IEPCs). The objective of these was to incorporate new technologies, best practices and new investors, but since the Mexican Constitution at the time precluded third parties from participating directly in exploration and production, the contracts were awarded with the developments being designated as services. These contracts did not result in a significant increase in output, as the companies’ incentives were in the services provided and not in increasing production or the reserves, and by 2012 the government was considering implementing an energy reform that would allow private participation in upstream projects. The authorities decided to outsource most of the Chicontepec development as new E&P profit/production-sharing contracts by ‘migrating’ the previous service IEPC’s to this new contractual form once the reforms were implemented.

Figure 4: Historic oil production of the oil basins of Mexico.

A new reserves certification conducted at the time downgraded the Chicontepec volumes so the official numbers by 2017 were 59 Bo and 31.5 Tcfg (in place) with 3P reserves of 6.3 Bboe (National Hydrocarbon Commission (CNH), 2017). The CNH (2020) official numbers are 65.35 Bboe but with only 4.6 Bboe of 3P reserves. Downgrading of these unconventional 3P resources at a time when most reserves in other basins are being revised upward is surprising, but it is possible that the new technologies and concepts that can render very tight, uneconomic, or marginal resources recoverable were not taken into consideration.

Since 2018 there has been a moratorium on outsourcing new projects and the use of hydraulic fracking and the IEPC contracts have not migrated, so the Chicontepec development has not been outsourced and with PEMEX operating only the small fields, the play is almost abandoned. In the meantime, the price of oil could sustain unconventional projects because operators have managed to reduce costs below break-even and they continue developing the Permian, the Bakken, the Eagle Ford, and others in the USA, and the Vaca Muerta in Argentina.

The original oil and gas volumes reported for all 29 fields, albeit downgraded, are still staggering. Less than 0.5% of the resources have been extracted: if only a small fraction of these oil and gas reserves were produced, it would have a huge impact on the upstream industry and economics of Mexico (Table 2).

Table 2: Original volumes and 3P reserves for the Chicontepec fields (before and after downgrade) and 2020 cumulative production. (PEMEX/National Hydrocarbon Commission).

The Shale Oil Plays

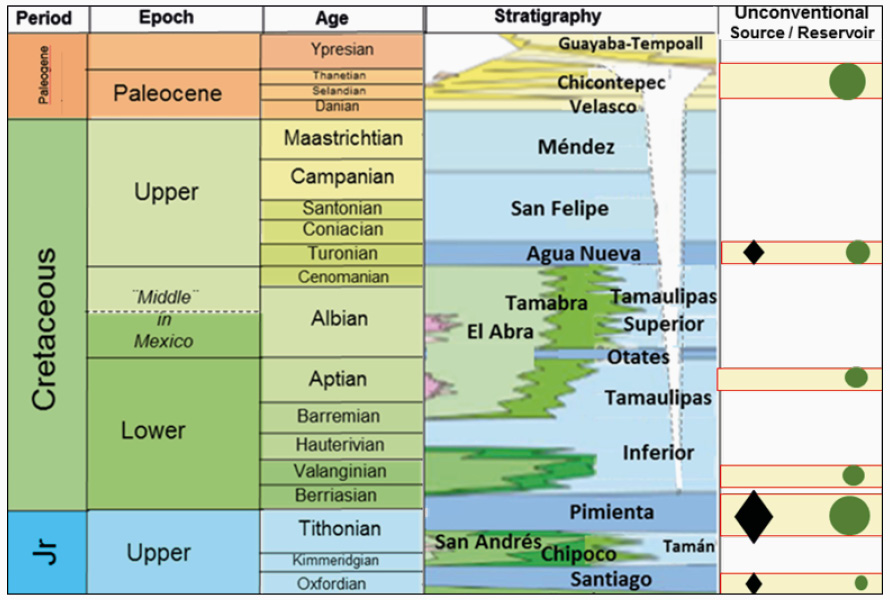

In the last decade, the shales in several Mexican basins have been extensively studied and their oil and gas potential tested. There are several shale and marl units in the basin which are rich in mature organic matter, and three of them – the Turonian Agua Nueva, the Tithonian Pimienta and Oxfordian Santiago Formations – have oil and gas that can be produced. In addition, the Kimmeridgian Tamán Formation has source rock characteristics, although its potential to produce has yet to be fully evaluated. These shales are widely distributed in northern and eastern Mexico (Figure 5).

The Tithonian Pimienta Formation, present in most of the basin and in the southern Burgos Basin, appears to be the most prolific. Several authors have concluded that it has excellent characteristics for oil and gas generation based on its good total organic carbon (TOC) values, hydrogen indices, and vitrinite reflectance. The kerogen type, which is indicative of mature, oil prone, marine organic matter, and the fact that these formations are rich in carbonate content, indicates very good potential as an unconventional resource.

Figure 5: Distribution of oil and gas in shales in Mexico.

Jarvie and Maende (2016) present a compelling case for the Upper Jurassic in the Tampico-Misantla Basin and conclude that there is very high potential for unconventional shale oil production due to the large volumes of retained petroleum, favourable rock properties, maturity that favours liquids, and high net thickness. They estimate about one billion barrels per 12,000 acres (48.6 km2) in the Upper Jurassic and conclude that the Tampico-Misantla Basin is potentially one of the best in the world. They also consider that the total petroleum generation potential for the Tithonian in the basin is 840 bo per acre-foot (for shale at 1.00% vitrinite reflectance), better than the Eagle Ford, the Woodford and the Vaca Muerta shales, although not as good as the Bakken, or the Bazshenov shales in Russia.

In the Tampico-Misantla Basin the Tithonian shale has a widespread distribution, being absent only over the Tuxpan Platform, the Tamaulipas Arch and the Teziutlán High. Several studies have established the Tithonian shale to be in the oil window and to have 1–8% TOC, kerogen type II/III and low structural complexity. The Turonian marls have 0.5–8% TOC, type II kerogen and are in the oil and gas windows.

Figure 6: Stratigraphic column showing distribution of the major reservoirs and oil and gas in shales in Mexico.

Recent studies of the Pimienta Formation in the Tampico-Misantla Basin address its petrology, mineralogy, geochemistry, petrophysics, resources and production potential. To date these resources remain untapped despite the very significant recoverable reserves identified (Table 3).

Untapped Potential

Development of the unconventional resources of the Tampico-Misantla Basin together with the exploration of the basin with new concepts and technologies and the optimisation of its legacy reservoirs, could put Mexico back on the list of the top oil-producing nations. The Tampico-Misantla Basin has the oil and gas resources and conditions required to be a super basin. It has the necessary infrastructure, access to markets and field services providers. It could be rejuvenated just as the Permian Basin was, thanks to its huge tight oil shale potential and its lack of exploration over recent decades.