New Technologies Unlock Value

In the wake of Covid-19, oilfield service providers are turning to new technologies based on digitalisation and automation.

With an increased focus on remote operations, productivity, and cost efficiency by operators in the wake of Covid-19, oilfield service providers are turning to new technologies based on digitalisation and automation. With remote drilling operations having gained traction and becoming the new normal, innovation within the drilling and well services segments has also gained momentum as both major well service companies and smaller players develop new technologies and niche product lines to fill the gaps to capture market share.

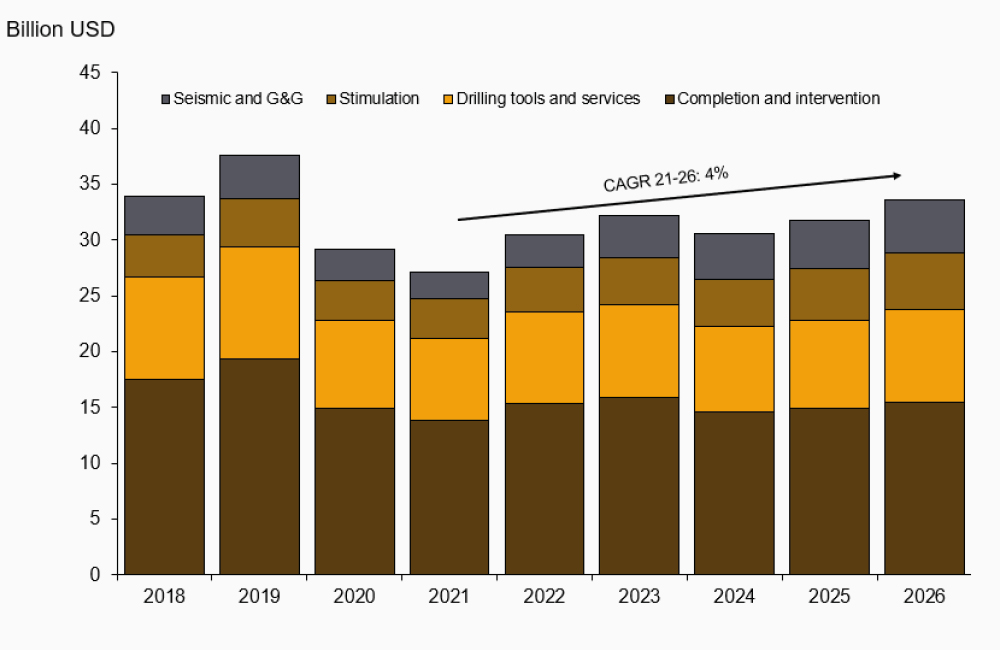

The figure below shows the expenditure for each of these segments in Asia Pacific from 2018 to 2020, with the significant impact of the pandemic evident in 2020. We can see that even though these segments were hit hard in 2020, they are expected to experience a marginal average growth of 4% each year until 2026. The drilling and completion segments account for 26% of the total cost of the well on average, providing ample incentives for service providers to develop technologies and solutions.

Growth of drilling, completion and geoscience purchases in Asia Pacific by Billion USD. Source: Rystad Energy ServiceCube.

The global pandemic has accelerated remote work, but in the context of the oilfield service industry, this presents a number of challenges. Remote working in the oilfield industry can be hindered by hardware and software resource constraints. This is amplified within reservoir engineering in particular as it requires vast computing resources to run computer intensive reservoir simulations. Some operators have sought to minimise hardware and software capex, and have rolled out Schlumberger’s DELFI (cognitive E&P environment), a high-performance cloud computing system that enables complex and different systems to talk to each other and promotes more collaboration between multiple disciplines. Woodside Australia, for example, has managed to shorten the duration of running more than a thousand simulations, which would otherwise typically take six months, to only one week using the DELFI system.