Why Norway?

For more than ten years, Norway has attracted small- and intermediate-sized companies because of favourable geological and fiscal conditions. An uplift in the tax system may now reduce the majors’ interest in the Barents Sea.

“A discovery on the Norwegian continental shelf (NCS) can potentially be more valuable than in many other countries,” says Jan Norstrøm, Vice President Technology at Rystad Energy.

The reason is that, contrary to common belief, the fiscal regime is quite favourable in Norway.

Jan Norstrøm, Vice President Technology, outside Rystad Energy’s head office, which is located on Aker Brygge in the centre of Oslo. The red building in the background is the City Hall.However, a recent tax hike took the industry by surprise and will make things more difficult for the development of small and marginal fields. This is also an important reason why the NCS was placed on a watch list by the petroleum industry. In the long run, “it may be regarded as less attractive if this kind of political decision-making continues”, according to Norwegian Oil and Gas.

Jan Norstrøm, Vice President Technology, outside Rystad Energy’s head office, which is located on Aker Brygge in the centre of Oslo. The red building in the background is the City Hall.However, a recent tax hike took the industry by surprise and will make things more difficult for the development of small and marginal fields. This is also an important reason why the NCS was placed on a watch list by the petroleum industry. In the long run, “it may be regarded as less attractive if this kind of political decision-making continues”, according to Norwegian Oil and Gas.

“Nonetheless, the exploration terms remain good and coupled with frontier acreage as well as many large discoveries, quite a few oil companies still look upon Norway as a place to be. In the Barents Sea, for example, an area with only a few commercial discoveries and quite a few disappointments, more than 40 companies – Shell, BP, ConocoPhillips, Total and Eni included – are actively exploring,” says Norstrøm, inspecting one of many diagrams that he spits out of the computer. In the latest licensing round, ExxonMobil was also amongst the applicants.

Scrutinising the World

Rystad Energy is an independent consulting company offering business intelligence data to a growing number of players in the oil industry. Oil companies, service companies, investors, investment banks and governments are all returning customers. The main product is a set of global databases specifically tailored to analysing the E&P and oilfield service industry.

“The consistency of the data provided is a result of systematic research, 24 hours a day, in several time zones,” says Norstrøm.

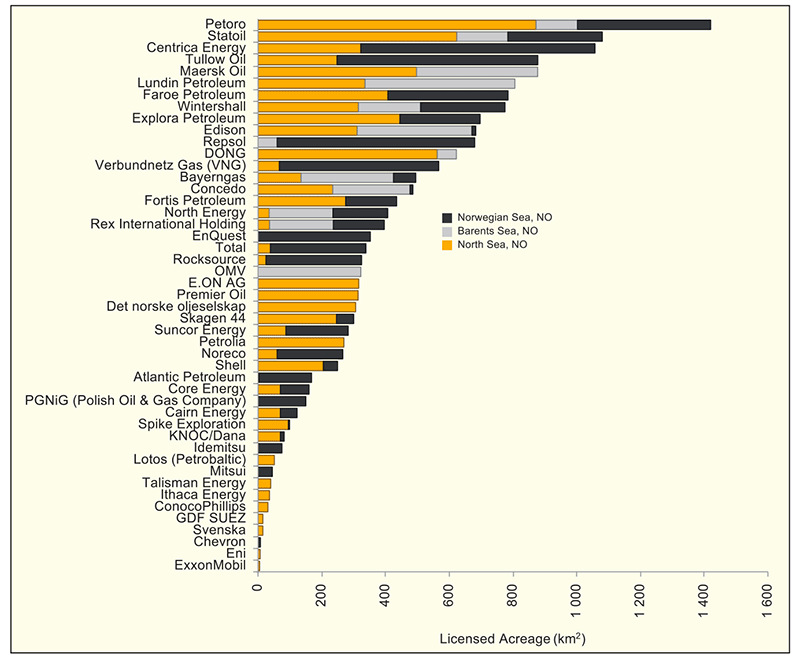

Companies with awarded acreage in predefined areas split by province.The analyses include E&P company reporting (over 1,000 companies are tracked), investor presentations, press releases, governmental sources, public institutions and academic sources including, for example, IEA, OPEC, USGS and the Norwegian Petroleum Directorate’s extensive reporting. Based on these sources Rystad Energy makes more than 1,000 data updates daily. The result is an impressive database that provides instant, colourful graphs of whatever statistics you might imagine.

Companies with awarded acreage in predefined areas split by province.The analyses include E&P company reporting (over 1,000 companies are tracked), investor presentations, press releases, governmental sources, public institutions and academic sources including, for example, IEA, OPEC, USGS and the Norwegian Petroleum Directorate’s extensive reporting. Based on these sources Rystad Energy makes more than 1,000 data updates daily. The result is an impressive database that provides instant, colourful graphs of whatever statistics you might imagine.

As a result, maths specialist Norstrøm can, in less than a second, tell you how many wells have been drilled in the Gulf of Mexico deepwater since the Deepwater Horizon explosion and blowout some four years ago (the answer is more than 350 exploration wells). In addition, he can tell you which companies have been involved, to what depth the wells have been drilled, and a lot of additional information.

Tough Comparison for the UK

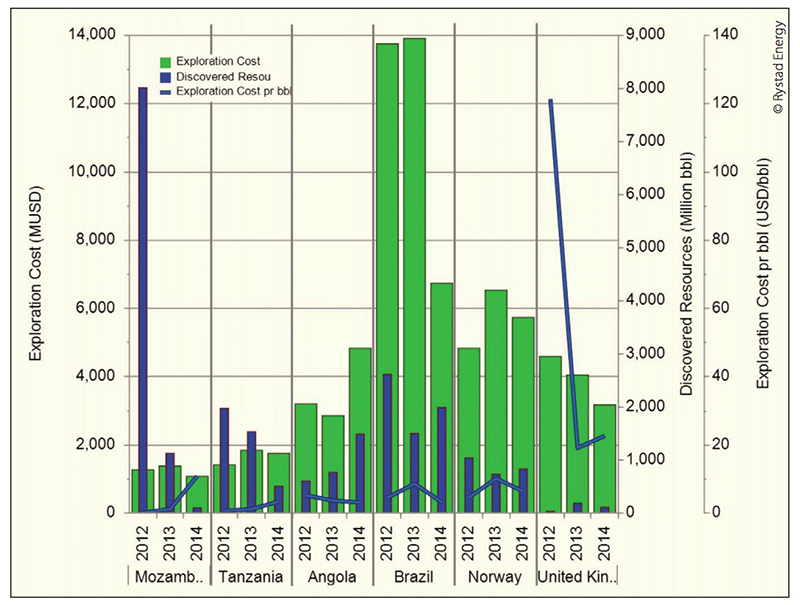

Norstrøm pulls out one graph that is of particular interest when it comes to illustrating how attractive Norway is in a worldwide setting.

The graph compares exploration costs in six countries. Thanks to several recent giant gas discoveries, average exploration costs since 2012 in East Africa – Mozambique and Tanzania in particular – are less than two dollars per barrel; for Mozambique, just 40 cents, and one dollar, 25 cents for Tanzania. Brazil used to have very good exploration costs, also less than two dollars per barrel, thanks to a number of giant oil discoveries, many in the Santos Basin. However, over the last three years the new finds have not delivered the same volumes, so costs have been averaging around $ 5/Boe since 2012. Angola comes out with a slightly better exploration cost, at around $ 3.8/Boe.

Exploration cost, discovered resources and discovery cost for six selected countries.“Norway compares favourably with these countries. Our estimate for the last three years, which includes 1.8 Bboe oil and 657 MMboe gas discoveries, totalling 2,400 MMboe of discovered resources, gives an exploration cost slightly in excess of six to seven dollars per barrel,” says Norstrøm. “Based on recent successes like the discovery of Johan Castberg, Wisting and Gohta in frontier areas, but also additions to old fields like the Gullfaks Lista formation, this may not be surprising.”

Exploration cost, discovered resources and discovery cost for six selected countries.“Norway compares favourably with these countries. Our estimate for the last three years, which includes 1.8 Bboe oil and 657 MMboe gas discoveries, totalling 2,400 MMboe of discovered resources, gives an exploration cost slightly in excess of six to seven dollars per barrel,” says Norstrøm. “Based on recent successes like the discovery of Johan Castberg, Wisting and Gohta in frontier areas, but also additions to old fields like the Gullfaks Lista formation, this may not be surprising.”

Norstrøm explains that Norway’s tax regime, with 78% cashback, is an important reason behind the low exploration cost as it encourages companies to drill more exploration wells. This, in combination with good exploration results, makes the country attractive.

“However, on the other side of the North Sea border, the perspective is quite gloomy. In the UK, discovered resources are very small, with only some 300 MMboe having been proved the last three years, resulting in an exploration cost which is sky high compared to Norway, at around 40 dollars per barrel,” Norstrøm says.

Ever Increasing Number

Based on the statistics above, it is not surprising that Norway is still attractive for explorationists.

“The primary reason is of course that there is still frontier acreage that needs many more wells, and that there are numerous prospects in the mature areas that continuously offer positive surprises. The last ones that left some geologists with eyes wide open was Pil and Bue, offshore mid-Norway, which may contain up to 175 MMboe recoverable,” says Norstrøm.

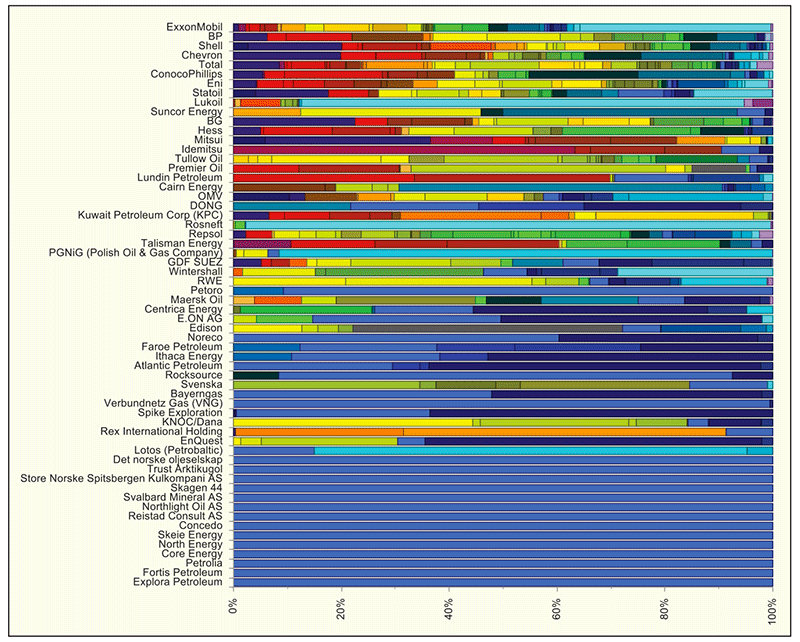

Companies active in Norway vs. other country exposure. Royal blue shows the Norwegian-only players. Other colours represent many other countries.Two other factors have been crucial in maintaining high activity on the NCS.

Companies active in Norway vs. other country exposure. Royal blue shows the Norwegian-only players. Other colours represent many other countries.Two other factors have been crucial in maintaining high activity on the NCS.

“The APA [Awards in Predefined Areas] system with acreage being offered every year within the mature areas, and the unique tax regime that allows companies to deduct exploration expenses without any producing assets, have both acted as a fly paper for smalland intermediate-sized companies, while many new companies have been established based on the revised tax system,” explains Norstrøm.

“According to our last count, 68 companies are ‘pre-qualified’ as either partners or operators, and 58 companies are currently active on the NCS, according to NPD. Out of these, 13 have offshore exploration acreage only in Norway, like Det Norske and North Energy. In addition, 20 out of the 68 companies have an offshore portfolio only consisting of Western European blocks where Norway is in focus.”

Making Things More Complicated

“Norway is a good place to be for small and intermediate-sized companies that are not dependent on making giant discoveries. For some of them, a modest discovery can easily be a company maker, as we have seen with Rocksource, a partner in both Pil and Bue.”

Acreage percentage split into regions for oil companies active in the Barents Sea. © Rystad EnergyWe can therefore expect continued interest in the mature areas. There are enough players that need to make new discoveries in order to thrive, while for some it is a question of surviving. Without a decent find, they can rapidly become cash-strapped; there are already examples of companies looking for more money to compensate for the lack of exploration success.

Acreage percentage split into regions for oil companies active in the Barents Sea. © Rystad EnergyWe can therefore expect continued interest in the mature areas. There are enough players that need to make new discoveries in order to thrive, while for some it is a question of surviving. Without a decent find, they can rapidly become cash-strapped; there are already examples of companies looking for more money to compensate for the lack of exploration success.

In the Barents Sea, the situation is different. There is still a need to attract the majors, but they are not happy about changes in the tax regime that are particularly negative for small discoveries. This is exemplified by the Johan Castberg discovery, which has been delayed by at least one year. According to Statoil, preliminary volume estimates are in the range of 400–600 MMbo but there are still uncertainties related to this as well as the investment level, so Statoil still considers the find marginal.

“The Norwegian government has recently proposed reduced uplift in the petroleum tax system, which reduces the attractiveness of future projects, particularly marginal fields and fields which require new infrastructure. This has made it necessary to review the Johan Castberg project,” says Øystein Michelsen, Statoil’s executive vice president for development and production in Norway.

“There is therefore a risk that the majors will withdraw, or put Norway on hold, as the Barents Sea is competing with acreage in other countries with potentially more attractive terms and better prospectivity,” says Norstrøm.

“Some 20 companies that are actively exploring the Barents Sea have acreage in other parts of the world. This applies not only to Shell, Total, Eni and BP, which have less than 5% of their licensed acreage in this area, but also to Statoil, which only has 20% of its exploration rights in North West Europe.

“We need to keep in mind that Norway in general and the Barents Sea in particular only represent a fraction of the acreage that the supermajors and majors control,” concludes Norstrøm.

More to Come

In APA 2014 a total of 47 companies applied fo r acreage in the mature areas. This is close to last year’s record of 50 companies, proving that both Norwegian and international companies still find Norway very attractive.

“The most important reason is, of course, that Norway still has attractive acreage. There is a strong belief amongst experienced geologists that a lot more oil and gas is to be found. According to the Norwegian Petroleum Directorate, 19 Bboe have not yet been identified,” says an optimistic Jan Norstrøm.