Photo: Tomislav Zivkovic/Dreamstime.com.

How much oil in the Middle East?

“No such galaxy of fields of the first magnitude over such a wide area has been developed in the history of the oil industry.” - Everette Lee DeGolyer, Oil in the Near East, 10 May 1940, Texas

Part Two of a two-part series by author Rasoul Sorkhabi, focusing on oil and gas in the Middle East. Part One – Why So Oil in the Middle East?

Current estimates place the Middle East’s conventional oil at about 800 Bbo, or nearly half of the world’s proven recoverable crude. What makes the Middle East so unique is the concentration of numerous giant fields in the region. With only 2% of the world’s producing wells, the Middle East’s output is over 30% of the world’s crude, highlighting its prolific fields. In addition, the Middle East holds 40% of the world’s conventional gas reserves. Despite our best estimates, it is not exactly known how much oil and gas exist in the Middle East and how much of it can be recovered in the future, but there is probably more to Middle East petroleum than what we currently know.

Where is the Middle East?

‘Middle East’ and ‘oil’ are images easily connected in the public mind. It is also commonly agreed that Middle East oil reserves and production have huge relevance for the global economy. Estimation of oil and gas reserves is usually a task threaded with many uncertainties. In the case of the Middle East, the problem is even more severe, not only because petroleum data are treated with secrecy by the Middle Eastern governments but also because it is not easy to define the Middle East. In a 2012 book Is There a Middle East?, a group of historians and geographers have argued that the term Middle East is simply a 20th-century geopolitical concept born out of British imperial geopolitics and that it has no reasonable geographic basis, partly because the boundaries of the so-called Middle East, unlike the terms Asia or Africa, cannot be well defined, and the ‘Middle East’ depicted variably on world maps by various authors is not really the middle of the East (whatever ‘East’ means).

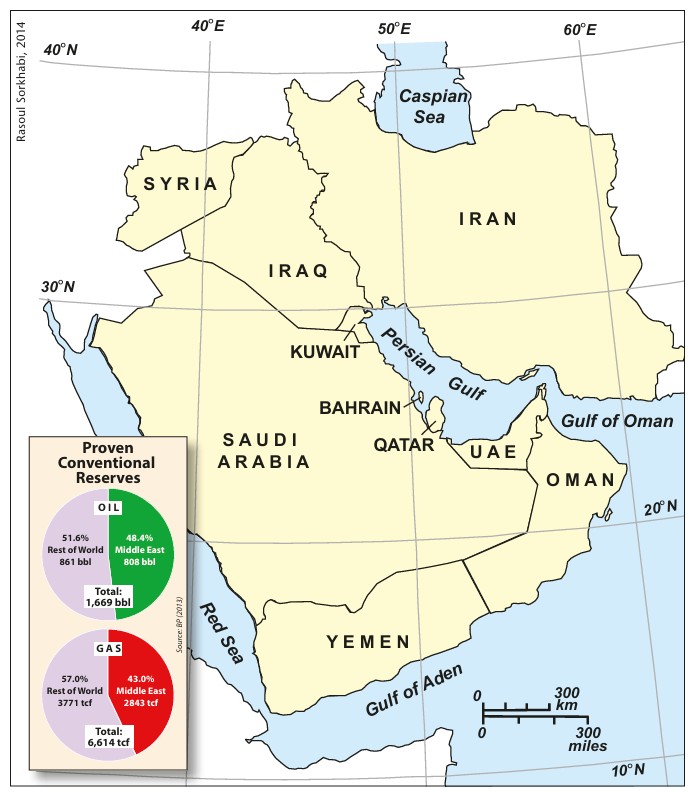

With this qualifying statement, for the purpose of this article, we define the Middle East as consisting of ten oil-producing countries in what is geographically South West Asia: Iran, Iraq, Syria, Kuwait, Saudi Arabia, Bahrain, Qatar, United Arab Emirates (UAE), Oman, and Yemen. These countries together cover an area of 5.4 million square kilometres (or about 3.6% of the Earth’s land surface) but their significance for the world’s oil economy is second to none. Of these countries, Iran, Iraq, Kuwait, Qatar, Saudi Arabia and UAE are also members of OPEC.

‘The Centre of Gravity’

The renowned American geologist Everette Lee DeGolyer (1886–1956) was one of the earliest oilmen to recognise the unique abundance of oil resources in the Middle East. In 1943, he visited Saudi Arabia on a special mission to collect data for an assessment of Middle Eastern oil. In his report (published in AAPG Bulletin, July 1944), DeGolyer estimated the oil reserves of Iran, Iraq, Kuwait, Saudi Arabia, Bahrain and Qatar to be about 27 Bbo but also suspected that ‘reserves of great magnitude remain to be discovered.’ He concluded: ‘The centre of gravity of world oil production is shifting from the Gulf-Caribbean areas to the Persian Gulf area.’ This, indeed, has been a reality for the past six decades. Geological reasons for the abundance of oil in the Middle East have been discussed in a previous article, ‘Why so much oil in the Middle East?’ Here we look at the patterns of petroleum reserves in the region.

Each year, several organisations such as British Petroleum (BP), Oil & Gas Journal (OGJ), OPEC, and US Energy Information Administration (EIA) publish estimates of oil and gas reserves for various countries. According to their latest reports, the Middle East as a whole contains 808 Bbo (BP, 2013), 802 Bbo (EIA, 2013), 799 Bbo (OPEC, 2013) or 797 Bbo (Oil & Gas Journal, 2013). This accounts for nearly one-half of the world’s total reserves of about 1.5 to 1.7 Tbo. Note that these data are given for geo-statistically ‘proven’, recoverable (with current technology and economy), and conventional oil reserves.

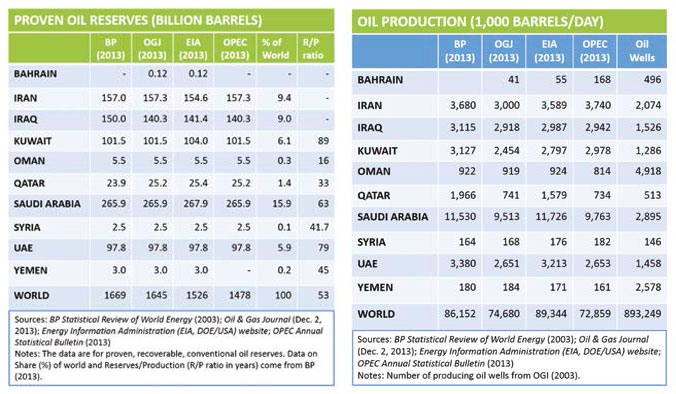

A very interesting fact emerges when we consider oil production and the number of producing wells globally and in the Middle East. In 2012, there were 893,249 producing wells around the world and their total output was 74.680 MMbpd; that averages 30,515 barrels per well in a year. In the Middle East, only 18,659 wells produced 23.130 MMbopd, which translates to oil production of 452,459 barrels per well per year (or 15 times the global average).

The Middle East is also home to abundant natural gas resources. Conventional gas reserves of the region are currently estimated to be 2062.5 Tcf (43% of the world’s total) (BP, 2013), 2822.7 Tcf (41%) (OGJ, 2013), 2880.3 Tcf (41%) (OPEC, 2013) or 2823.3 Tcf (41%) (EIA, 2013).

Patterns of Reserves Distribution

The distribution of oil fields and reserves is not uniform throughout the Middle East for a variety of reasons, partly because of the size of each country. For instance, Saudi Arabia, with an area of 2.1 million km2 or almost five times the size of Iraq (400,000 km2), is home to oil reserves of 265 Bb or nearly twice the volume of Iraq’s oil reserves (140 Bb).

A more important factor is the location of each country with respect to the optimal petroleum geology of sedimentary basins. For instance, although Kuwait has an area of only 18,000 km2, less than one-tenth the size of Syria (187,000 km2), its oil reserves of 101.5 Bb far exceed Syria’s reserves of merely 2.5 Bb. Finally, we should also consider the non-uniform nature of oil exploration activities in various parts of the Middle East or across the spectrum of stratigraphic levels from shallower to deeper rocks.

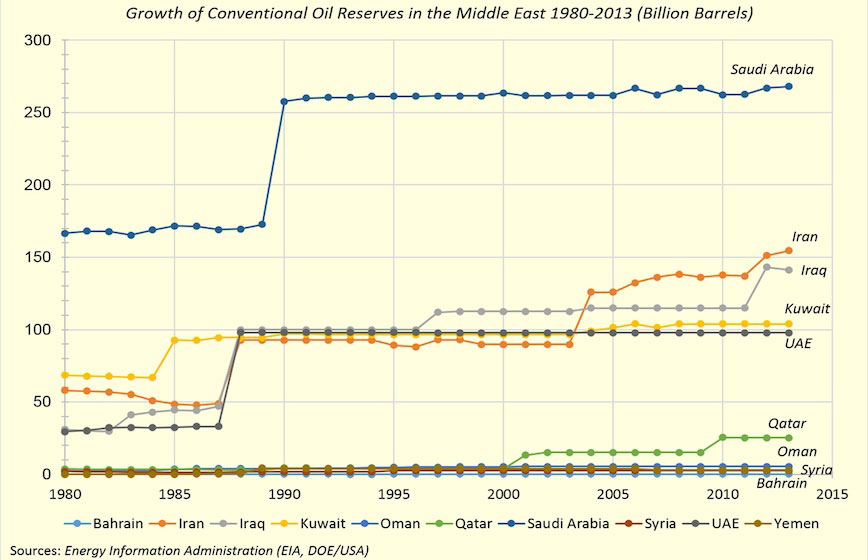

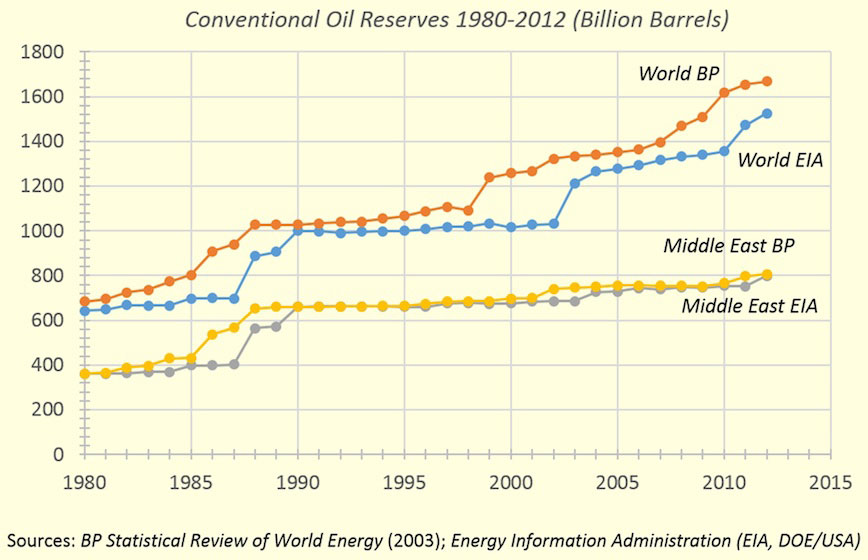

In terms of geology, there is a finite volume of petroleum in a given reservoir and basin. However, ‘reserve’ estimates are always in a state of flux because of changes in our knowledge of basin geology, exploration activities, drilling and recovery technology, and assessment methodology. Utilising these factors thus leads to ‘reserves growth’ through time. For instance, in 1960 (when OPEC was formed), the Middle East oil reserves were estimated to be 183 Bb (or 60% of the world’s total) which increased to 343 Bb in 1970 (55%), 362 Bb in 1980 (53%), 661 Bb in 1990 (53%), 697 Bb in 2000 (55%), and 766 Bb in 2010 (47%). These data (from BP sources) indicate that Middle Eastern oil reserves have accounted for about one-half of the world’s proven oil in the past six decades.

Future Plays: Frontiers and Unconventionals

Early oil discoveries in the Middle East were made in Jurassic, Cretaceous and Oligocene limestone reservoirs. Indeed, these reservoirs are still the major plays in the Middle Eastern basins. Given its decades of prolific production, the Middle East is often thought of as a ‘mature’ petroleum province. However, promising oil and gas prospects do exist in the region.

Future plays that would drastically increase the Middle East’s oil reserves and production can be categorised into the following:

- Frontier Areas: Some parts of the Middle East remain poorly explored. One notable example is Iran, where oil production has traditionally come from the Zagros Basin in southwest Iran, while the central and northern parts of the country remain virtually untouched.

- Deep Plays: Although Permian and Silurian rocks have been drilled in some parts of the Middle East, the Palaeozoic section in deeper parts of the basins has not been explored thoroughly.

- Unconventional Resources: With such abundant conventional reserves, it is probably less attractive economically for Middle Eastern countries to tap into unconventional resource plays such as shale gas, oil shale, tight sandstone and coal-bed methane. Nevertheless, these resources exist in the region although comprehensive studies and exploration have not been made. For example, Jordan (not included in this article for its insignificant conventional oil and gas) sits on one of the world’s largest oil shale (immature kerogen) plays. Indeed, the Middle East stratigraphy contains several major regional shale plays, both in the Palaeozoic and the Mesozoic sections, which are excellent candidates as self-sourced shale reservoirs.

In 2012, the United States Geological Survey released its ‘Assessment of Undiscovered Conventional Oil and Gas Resources of the Arabian Peninsula and Zagros Fold Belt,’ in which it estimates 86 Bb for yet-to-discover conventional oil and 336 Tcf for yet-to-discover conventional natural gas. The report recognised several petroleum systems in the Middle East with the following source rocks: Huqf (Precambrian-Cambrian); Silurian-Ordovician; Palaeozoic-Triassic in Euphrates Graben of Syria; syn-rift Triassic-Jurassic sediments in the Palmyra and Sinjar areas; Madbi-Amran-Qishn system (Upper Jurassic) in Yemen; Middle Cretaceous Natih Formation in Oman; and Jurassic-Cenozoic systems distributed in much of the Arabian platform and Zagros Basin, accounting for 92% of the estimated yet-to-discover oil reserves in the region.

Finally, improvements in recovery technology can also boost the Middle East’s reserves and production. Assuming a recovery efficiency of 50%, almost one-half of oil-in-place still remains underground in conventional reservoirs.