The metals Company’s (TMC) August release marks a milestone in its history, as well as for the global marine minerals industry. The technical summary of the pre-feasibility study (PFS) for its NORI-D nodule project includes the declaration of mineral reserves, which is a first in the deep marine realm.

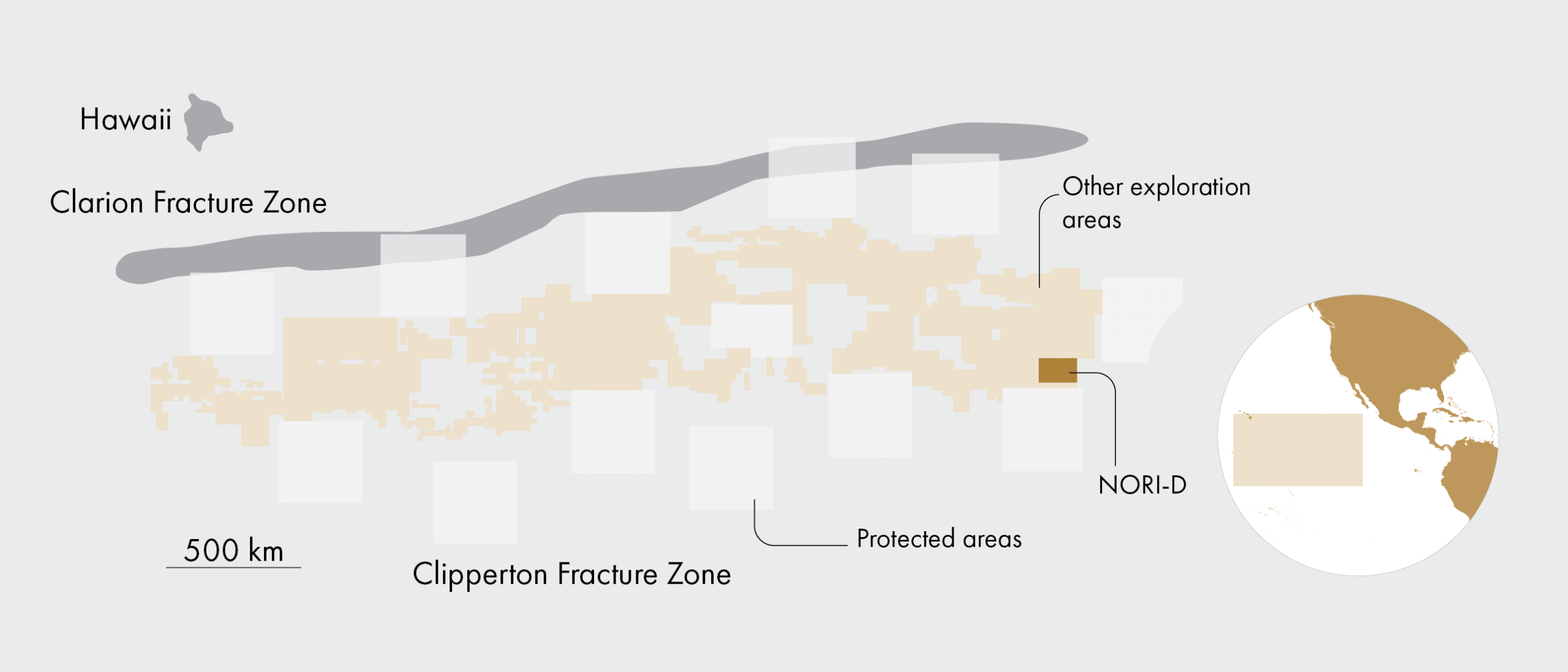

Located in the Clarion-Clipperton Zone (CCZ), the world’s largest known nodule field in the Pacific Ocean, NORI-D is a cornerstone of TMC’s ambitions. The company is targeting commercial production by late 2027, reaching 10.8 of wet nodules annually by 2031. The expected production timespan is 18 years.

The technical report declares 51 Mt of probable reserves. Additionally, 274 Mt are pegged in the “measured, indicated and inferred” mineral resource categories, with 113 Mt potentially recoverable beyond this. Annually, NORI-D is expected to produce approximately 97 kt of nickel, 2.4 Mt of manganese, 70 kt of copper, and 7.4 kt of cobalt, comparable to a medium-to-large land-based mine.

TMC’s lean, capital-light strategy with initial capital outlays of less than $550 M, should appeal to investors. The PFS outlines a phased approach, leveraging vessels and offshore operations by partner Allseas and initial onshore processing by Pacific Metals Company (PAMCO). The PFS projects an after-tax net present value (NPV, estimated future cash flow value today) of $5.5 B for NORI-D, with a 27 % internal rate of return.

Rosy price assumptions

However, the metal price estimates stand out as rather optimistic, with cobalt prices well above current levels. While TMC states that the price assumptions are provided by third parties, mining companies typically use more conservative commodity price assumptions in technical reports.

In TMC’s defence, a price sensitivity analysis shows NORI-D retains a solid NPV of around $4.9 B, even with a 20 % decline in the price of either nickel sulphate and manganese, the two most sensitive metals in the NPV analysis. Still, a corporate practice of using buoyant prices may leave some investors to question whether other aspects of the PFS are overly optimistic.

Icebergs ahead

Critics share these concerns. Iceberg Research, known for its activist approach and short-selling reports, sharply criticizes the PFS’s validity in its latest report. The research firm highlights a 152 % surge in offshore costs and a 35 % cut in nodule production due to complex seabed terrain. Iceberg also criticises TMC’s above-market metal price assumptions, noting that its manganese output (13 % of global supply) could flood the market and depress prices. Iceberg’s recalculated NPV, with conservative assumptions, yields a negative $1.5 B, concluding: “The economics simply do not work”.

However, despite widespread scepticism over TMC’s daring sidestep of the ISA, a recent $85 M strategic investment from metals refiner Korea Zinc signals a vote of confidence. Furthermore, TMC’s stock price has soared in 2025, suggesting market belief in the company’s future.