![]()

Upstream projects for the global transition

Whether the world likes it or not, hydrocarbons will still be needed even envisaging the most optimistic energy transition. At the time of writing, with COP26 under way, the world’s leaders are still trying to agree what measures they should be targeting by 2050 (or in China’s case 2060), in order to limit the rise in global temperatures. Limited progress seems to have been made in agreeing exactly how they intend to achieve this, other than a phasing out of coal over the coming decades.

Future demand for E&P projects

The transition will need to include hydrocarbons, and in particular gas, to bridge the gap until alternatives which are both achievable and affordable, are developed to replace them in the next 30 or so years. Gas is clearly significantly less emissive than coal which still powers some of the largest economies and by switching one for the other would come very close to reducing the emissions by the 30% climate change experts consider is necessary to keep global temperature rises below 1.5°C by 2050.

The lack of funding following the commodity price crash in 2014, increasing environmental, social and governance (ESG) influence on investors and the last two years of the Covid-19 pandemic has significantly dented the global upstream sector’s traditional exploration capability. The key question is whether the remaining capability can meet the future demand and unlock the new oil, and increasingly gas resources, that will be needed for the transition. As commodity prices inevitably increase with tightening supply and new upstream investment returns with improved profitability, it is expected that market money will again become available to fund the search for the hydrocarbons needed to achieve the energy transition.

![]()

Lower risk, near-term cash-flow projects (albeit ESG compliant) will almost certainly be the first investments to attract funding, and there are many projects available now that would already have secured funding in a more buoyant market. Associated exploration will also return in time, assuming prices stay high, as investors seek the financial ‘blue-sky’ rewards that exploration and production (E&P) can generate. This is likely to include a contribution from E&P companies as their cash flow and profits increase and can again be risked to replace and grow resources.

The Asian opportunity

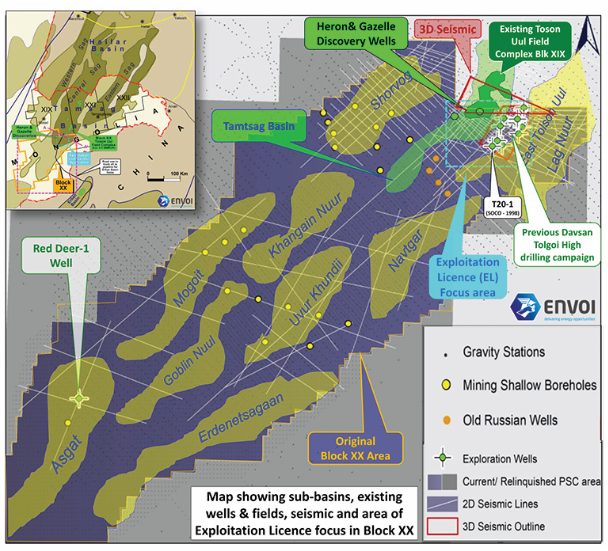

In some of the world’s fastest growing economies with the highest energy demand growth (currently reliant on the most emissive fossil fuels including coal), Envoi has already seen evidence of renewed interest in E&P projects and recognition that now is an excellent time to participate before a potential new exploration cycle gathers pace. In this regard, Envoi’s client, Petro Matad, has recently been awarded an Exploitation Licence for their Block XX in Mongolia which allows them to focus on development of their Heron and Gazelle discoveries with existing nearby infrastructure. These assets will benefit from immediate access to the strong, local, Chinese market just across the border. Surely this would be better for the environment than using coal upon which much of the region currently relies.

NE Mongolia (Tamtsag Basin) Block XX Exploitation Licence: Key Information for Investors

- Development of 3D defined 2019 Heron-1 discovery (flowed 821 bopd on test) at the southern end of the Tamtsag Basin.

- Established export route from existing fields ensures early revenue potential (2022) from CPR defined 19 MMbo contingent resource potential in Heron-1 discovery well.

- Combined 32 MMbo (P50) contingent and prospective (with 200+ MMbo upside) resource in Heron and Gazelle discoveries, and large additional upside in several undrilled lead

![]()

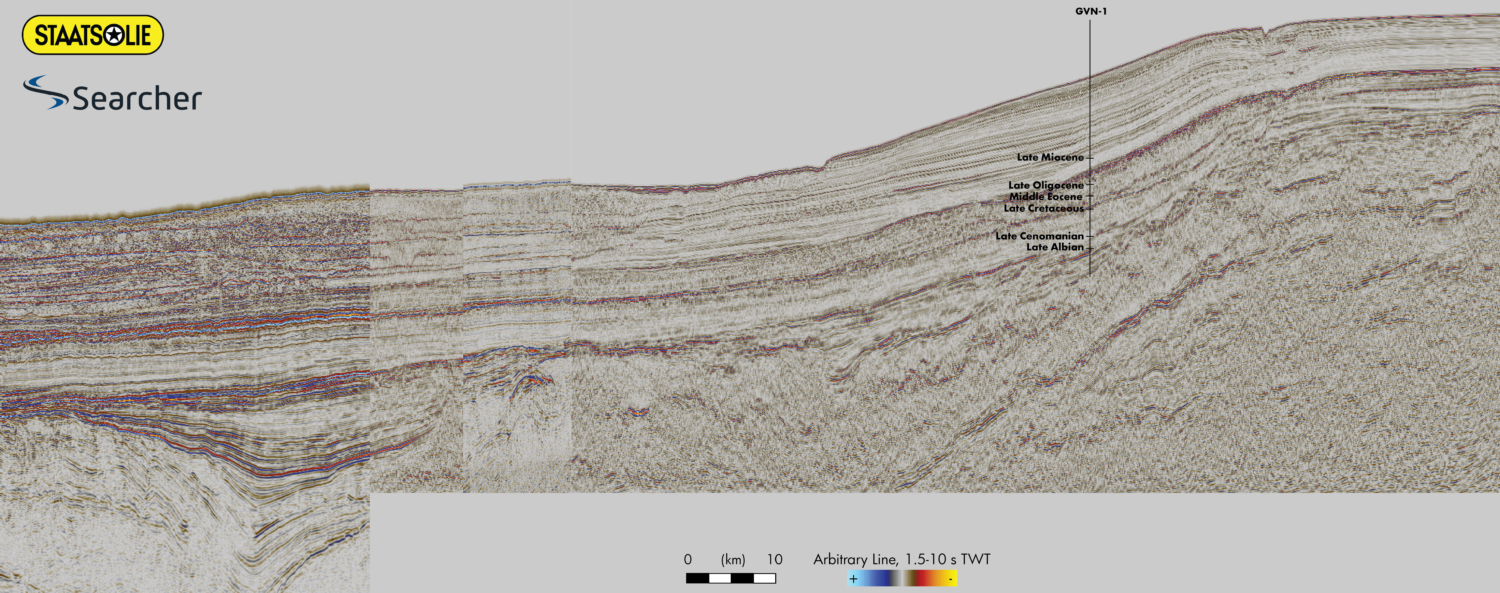

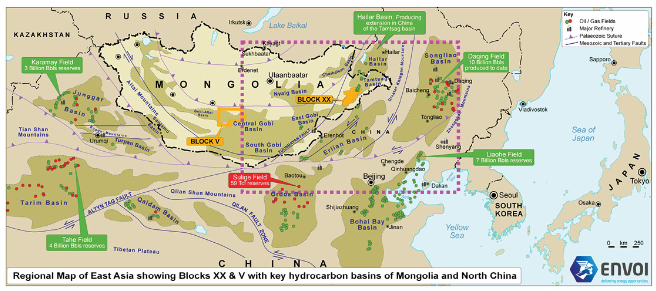

Petro Matad Ltd, the London AIMlisted company, has commissioned Envoi to identify a strategic partner to join them in the appraisal and development of two discoveries made in 2019 in the northern part of their large, 100% owned and operated, Block XX Exploration Licence. Situated in the Tamtsag Basin of NE Mongolia, which is historically the most productive part of the country, Block XX lies at the southern end of the basin where Petro Matad’s successful Heron-1 discovery in 2019 was in effect an appraisal of the existing T19-46-3 discovery made in 2009 immediately to the north in the adjacent Block XIX Licence operated by PetroChina. This was the southernmost discovery in the Toson Uul Sub-basin where the first of many discoveries were made by SOCO in the late 1990s and sold to PetroChina in 2005. They have since drilled numerous wells and defined new closures as well as fully developing the Cretaceous-aged Tsagaantsav and Zuunbayan Formation plays of the existing fields found in the Tamtsag Basin. Regionally, these are a geological extension of the proven Hailar Basin that has been producing oil across the border in China since the 1980s, following exploration dating back to

the 60s (Regional maps).