Markets are fickle and the market for E&P equities is no exception. Investors tend to like smaller oil companies when oil prices are rising but abandon them for the safe haven of dividend-paying supermajors when oil prices fall. Linking the short-term oil price to the longer-term value of subsurface assets is not logical and this pattern of investor behavior can result in the mis-pricing of assets and share price volatility.

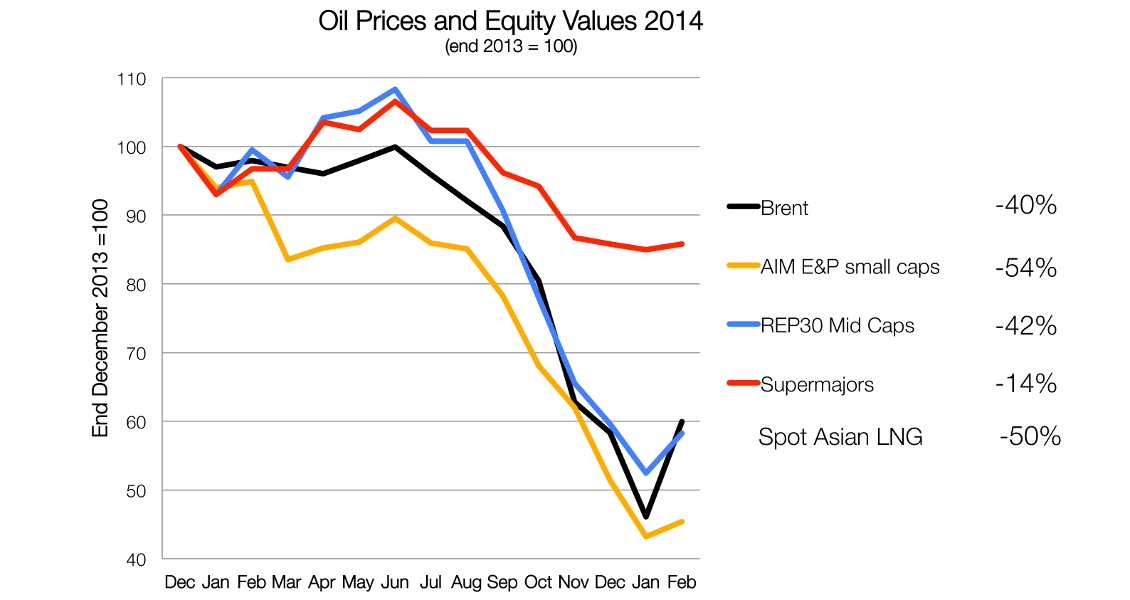

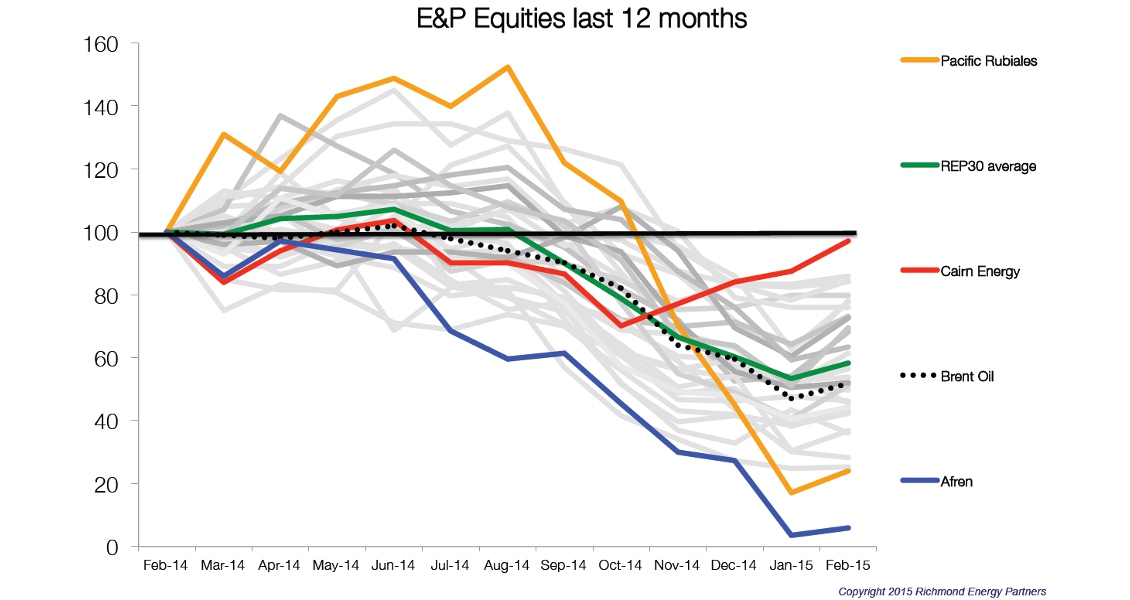

The value of small E&P companies on the London AIM Stock Exchange has dropped 54% in the past year – more than the drop in the oil price over the same period. Meanwhile, shares in the supermajors have proved more resilient, losing a mere 14% of their value in 2014, and have outperformed smaller oil companies over the last seven years due to their ability to pay dividends. The small and mid cap E&P sectors on average have delivered positive returns only in years when the oil price increased and investors had an appetite for risk. The unpredictability of individual stock performance makes effective stock picking very difficult, with a number of companies losing as much as 95% of their value in the past year while a few, like Cairn Energy who made a significant discovery, were able to maintain their February 2014 value (at least until they were hit by a hefty Indian tax demand).

‘Oil price fall triggers re-rating of E&P stocks.’ Is the correlation justified? (Copyright: Richmond Energy Partners).

‘Oil prices and E&P Equities’. In last 7 years smaller cap E&P sector on average delivered positive returns only in years when oil price increased. (Copyright: Richmond Energy Partners)

E&P Equities performance over the last 12 months. The spread is enormous making stock picking extremely difficult.

The truth is that exploration is not completely out of favor with investors, but it has not been delivering sufficient high impact discoveries to make it a good investment. It could be said that investors sowed the seeds of capital destruction by encouraging too much exploration and the creation of too many start-up oil companies during the last oil price ‘up’ cycle. This has added to competition and the consequent cost inflation. It is now difficult for the smaller companies to access equity capital when oil prices are flat or falling.

Those Elusive New Plays

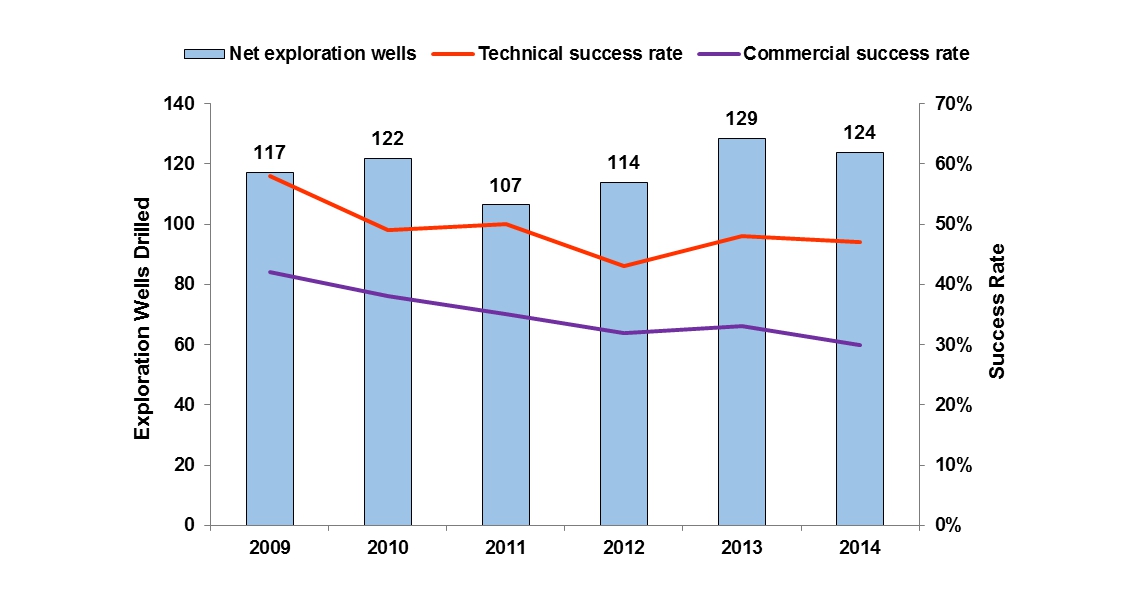

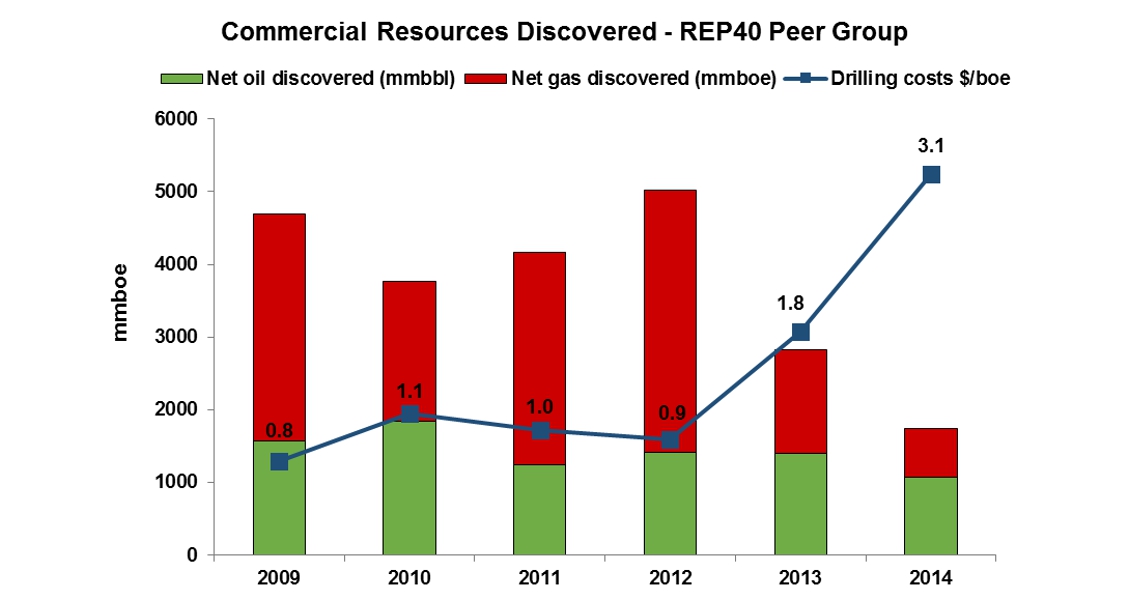

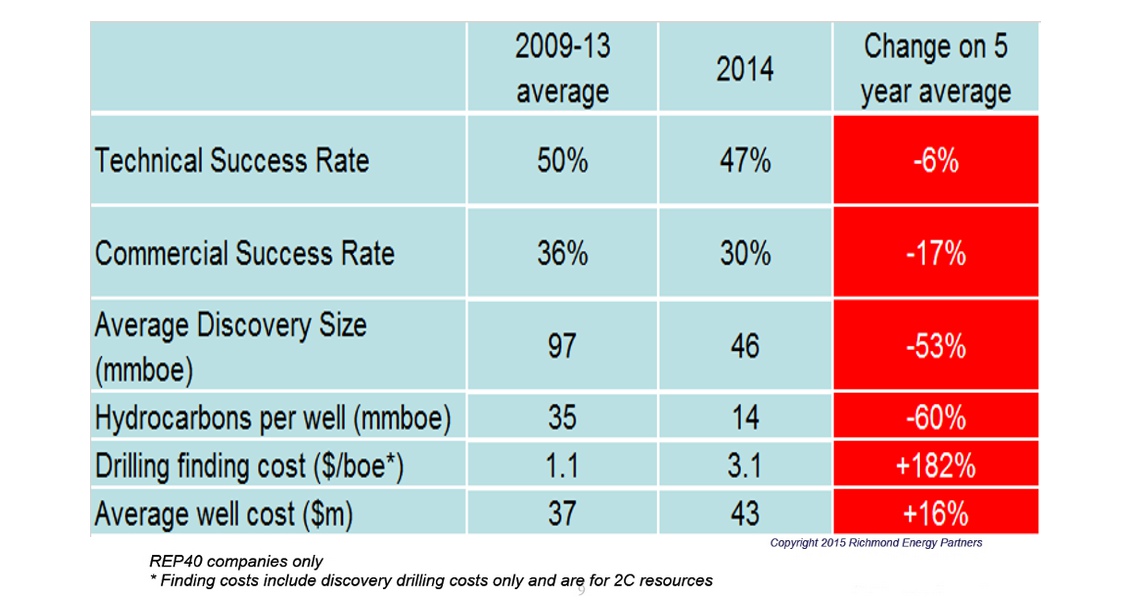

The commercial success rate of exploration wells dropped from 40% in 2009 to only 30% in 2014 with discovered volumes at a 7-year low. Using REP40, the Richmond Energy Partners peer group of 40 mid-cap and large cap companies, chosen to test the pulse of global exploration, average drilling finding costs have shot up, from an average $1.0/boe between 2009 and 2012 to $1.8/boe in 2013 and $3.1/boe in 2014 – an increase of 210%, and not creating value at current oil prices. Performance in the 2009 to 2012 period was flattered by large gas discoveries in East Africa and the Eastern Mediterranean. Since then declining average discovery sizes and increasing numbers of very high-risk, high cost deep-water frontier wells have weighed on success rates and finding costs.

Net Exploration Wells and Success Rates – REP40. (Copyright: Richmond Energy Partners)

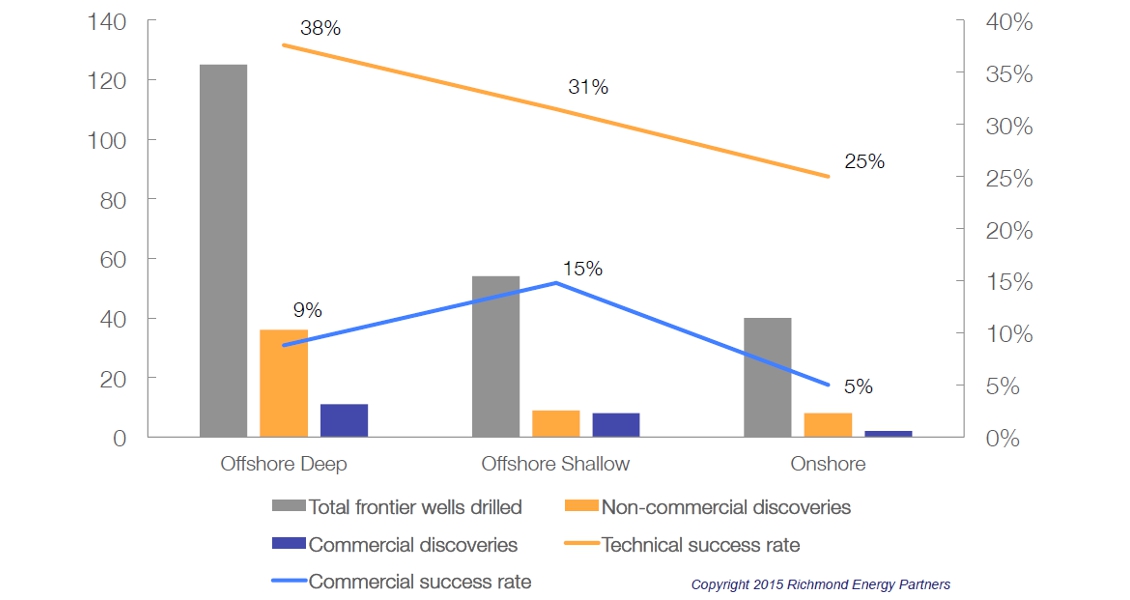

2009-2014 frontier drilling success rates by water depth. (Source: Wildcat database end February, 2015)

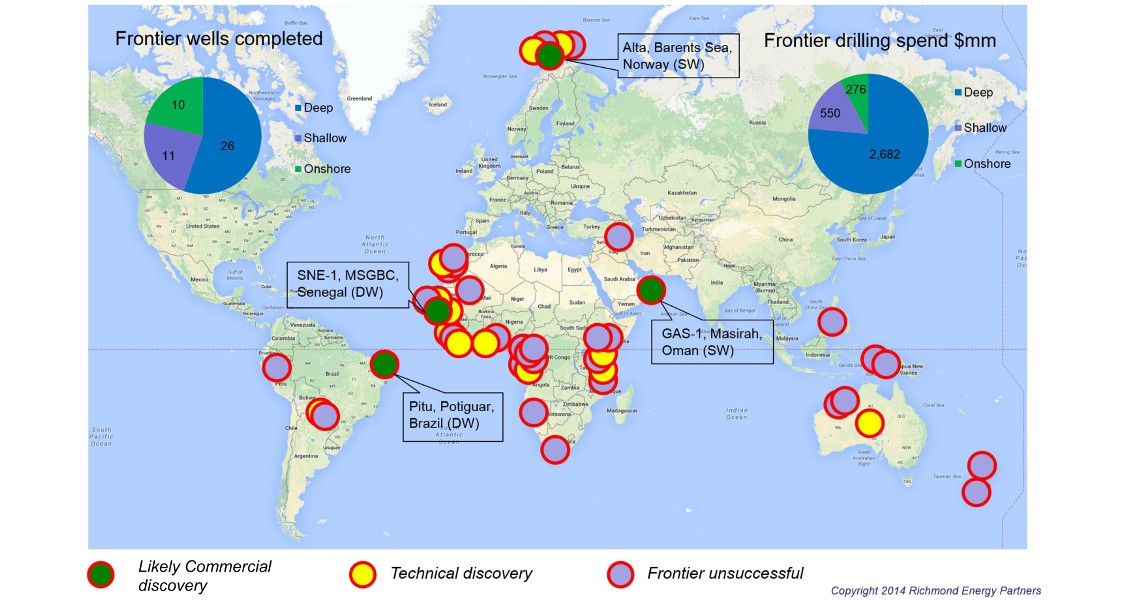

The industry has been drilling record numbers of wells in frontier basins and plays, particularly in deep water, seeking elusive new oil plays. The 47 frontier wells in 2014 delivered only four new potential commercial plays (in Norway’s Barents Sea, the Potiguar Basin off Brazil, offshore Senegal and possibly Oman). Richmond Energy has analyzed $17 billion of drilling spend on frontier wells since 2008 and found that the frontier program delivered a creditable technical success rate of 33% – but a commercial success rate of only 10%.

Frontier wells in 2014 – only four were potential commercial discoveries. (Source: Wildcat database end February, 2015)

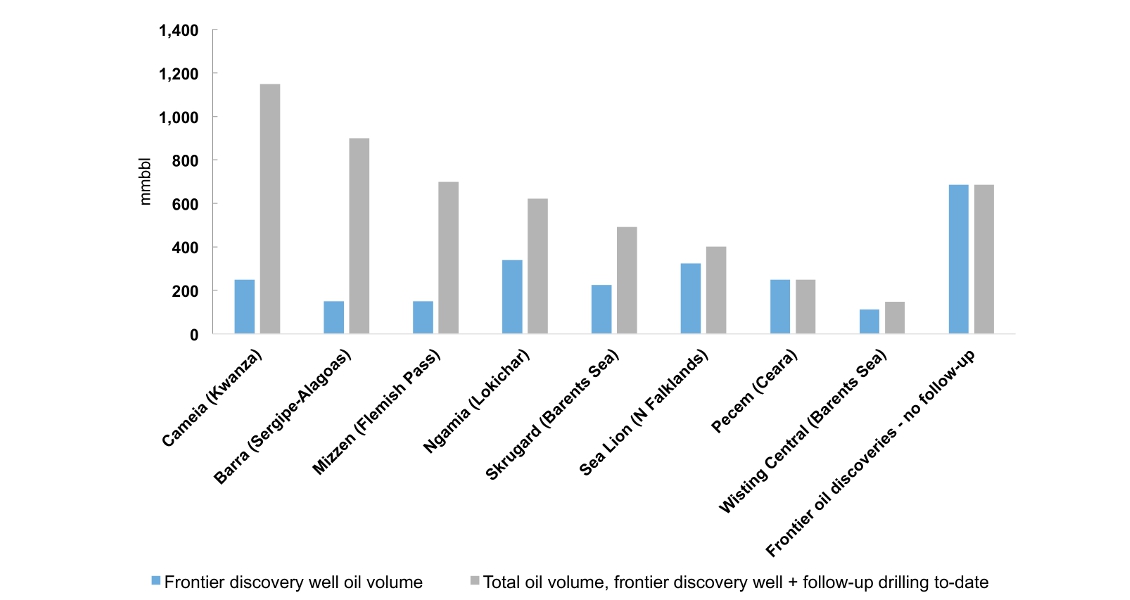

Frontier oil discoveries by basin 2009-2014 and follow-up drilling: discoveries in the new emerging provinces have been relatively modest. (Copyright: Richmond Energy Partners)

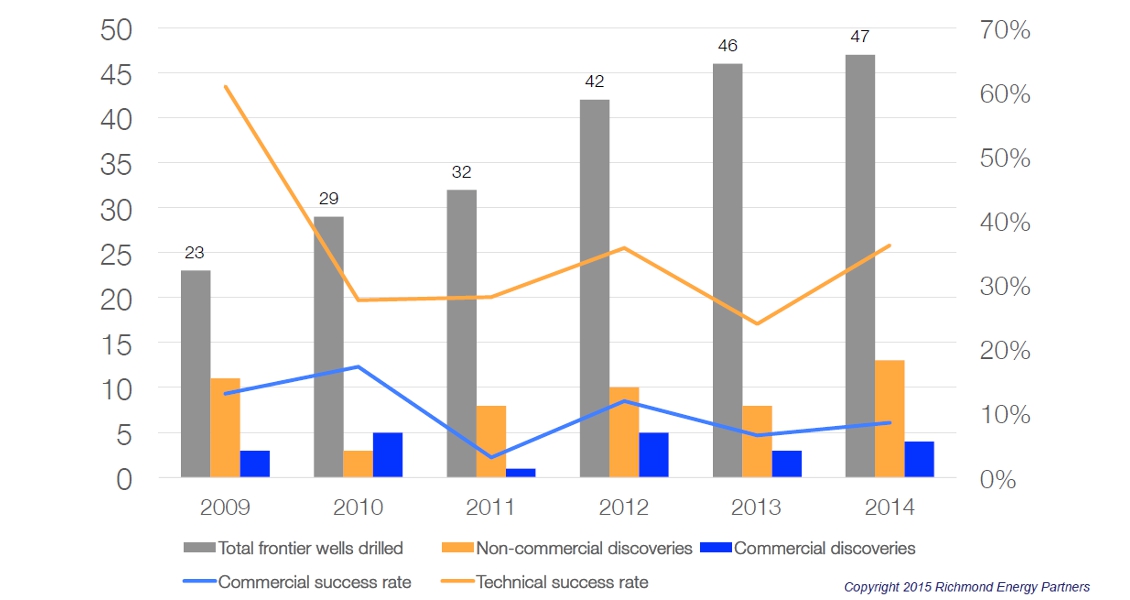

Frontier wells drilled 2009-2014. ‘The industry is trying ever harder at frontier exploration.’ (Source: Wildcat database end February, 2015)

Whilst the frontier gas discoveries have led to 170 Tcf of follow-on discoveries in East Africa and the Eastern Mediterranean, the frontier oil provinces discovered have been modest in size. Only the pre-salt of the Kwanza Basin has so far opened an oil province bigger than a billion barrels, but even here recent dry holes have limited the scale of the province. The total oil volumes discovered in these new provinces found so far is only equal to 80 days of current world oil production. Disappointingly, few of these emerging provinces have built on their early promise through subsequent drilling.

Commercial discovered resources have plummeted since 2009, while finding costs (in $/boe) have risen dramatically (source: Wildcat database end February, 2015).

Richmond Energy Partners expects exploration drilling to be down about 40% overall in 2015 and so 2014 should prove to be the high water mark for frontier drilling. Nonetheless, over 30 frontier wells are still expected to complete in 2015.

Blip – or the Future?

So is it time to invest – or to panic? Well, that depends on your perspective. Exploration certainly needs to deliver higher returns to restore investor confidence.

If you are convinced that oil prices will recover and that 2014 is only a blip in the exploration cycle, meaning that investor risk appetite and interest in the sector will rapidly return, then this is a good time to invest. You would be able to take advantage of lower competition and costs. Of course, it is definitely time to invest if you happen to know where the next big play is going to emerge.

However, high debt business models combined with high cost assets (both operating costs for mature assets and capital costs for assets currently under development, sanctioned in the previous high oil price era) leaves little for equity investors to get excited about. Companies holding high-risk acreage with big work commitments without the necessary funds available are also in a vulnerable position.

And feel free to panic if you think that 2014 may not be a blip in performance but is, in fact, the future.

Exploration performance for the REP 40 companies – 2014 was not a good year. (Source: Wildcat database end February, 2015)