Rystad Energy has identified three key drivers for the expected production growth: production itself, breakeven prices for new projects and total spending.

Production evolution

The production in the North Sea is originating mainly from Norway and the UK and only minor production comes from Denmark and the Netherlands. Production has declined from 5.5 million boe/d in 2010 to 4.3 million boe/d in 2014 due to natural decline of mature fields. After a period of growth in 2015-2017, the decline was resumed, with this year’s supply expected to fall to around 4.4 million boe/d.

Renewed production growth is driven by Johan Sverdrup. The first phase of the Johan Sverdrup project is expected to start producing by the end of 2019, and the second phase in 2022.

Non-producing fields

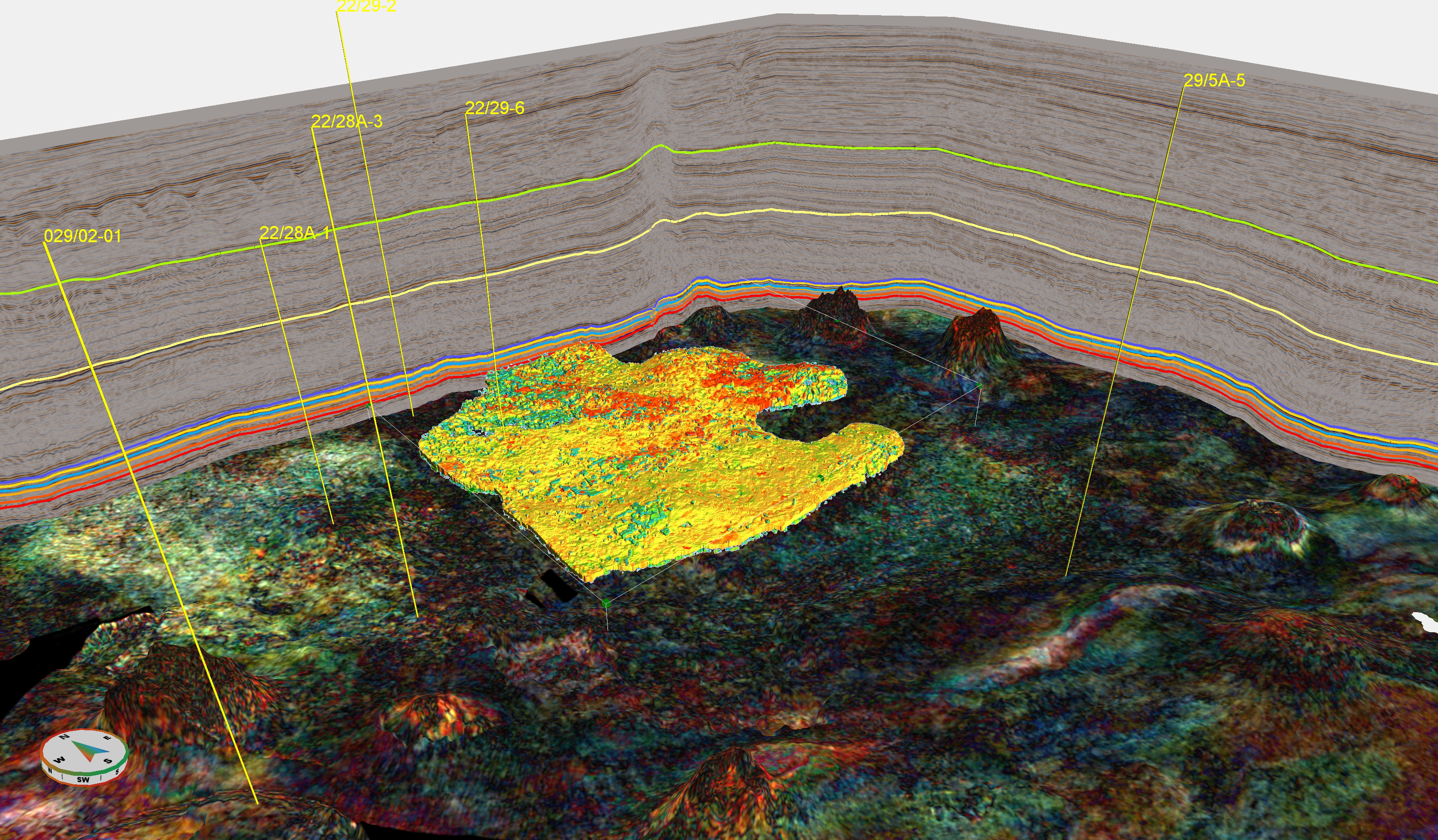

If we look at the top 10 non-producing fields in the North Sea, Johan Sverdrup is the evident leader. The field holds resources of 2,200 million. The first phase of the field has an estimated breakeven oil price of just around $21 per bbl. The unsanctioned phase 2 has an estimated breakeven oil price of $32 per bbl. This means development is economically profitable even with the current low oil price.

Two other fields on the NCS, the gas fields Troll West and Martin Linge, are being developed and will most likely start producing in 2020-2021. In the United Kingdom, two large sanctioned fields are expected to come online this year: the Mariner oil field with 300 million boe of resources and the Culzean gas field with 250 million boe of estimated resources.

Investments

Investments (capex and exploration capex) reached peak levels in 2013-2014 and have declined since then to a low in 2017. Rystad Energy states that the increase in spending before 2014 was mainly from mature fields in the Norwegian North Sea but investments after 2017 are from the development of discovered resources (Johan Sverdrup and Culzean). After 2020, discoveries in the Oseberg and Ekofisk areas, the Grosbeak discovery as well as the redevelopment of the Hejre field in the Danish North Sea are expected to see increasing investments, according to Rystad Energy.

To summarize, there are many resources still to be developed in the North Sea, which can be profitable even with a low oil price. The long-term production in the North Sea is dependent on the development of these discoveries.

Read the full article from Rystad Energy here.