Geothermal, in the Oil Patch?

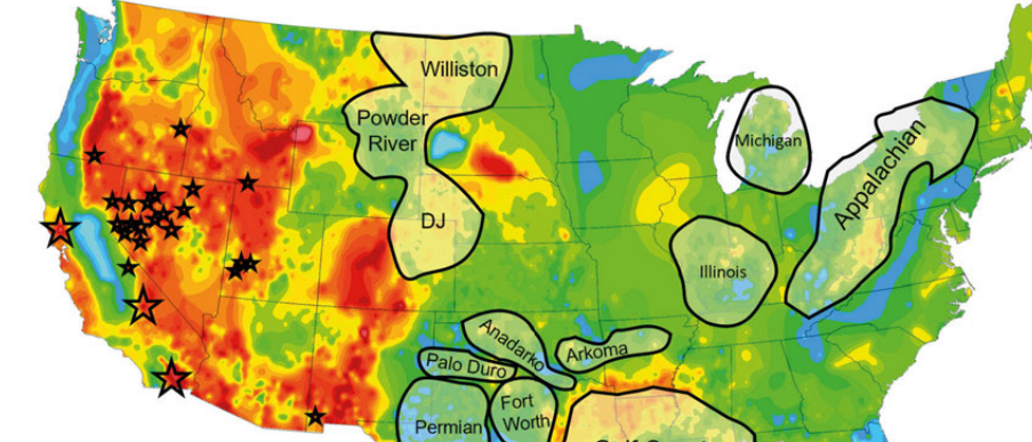

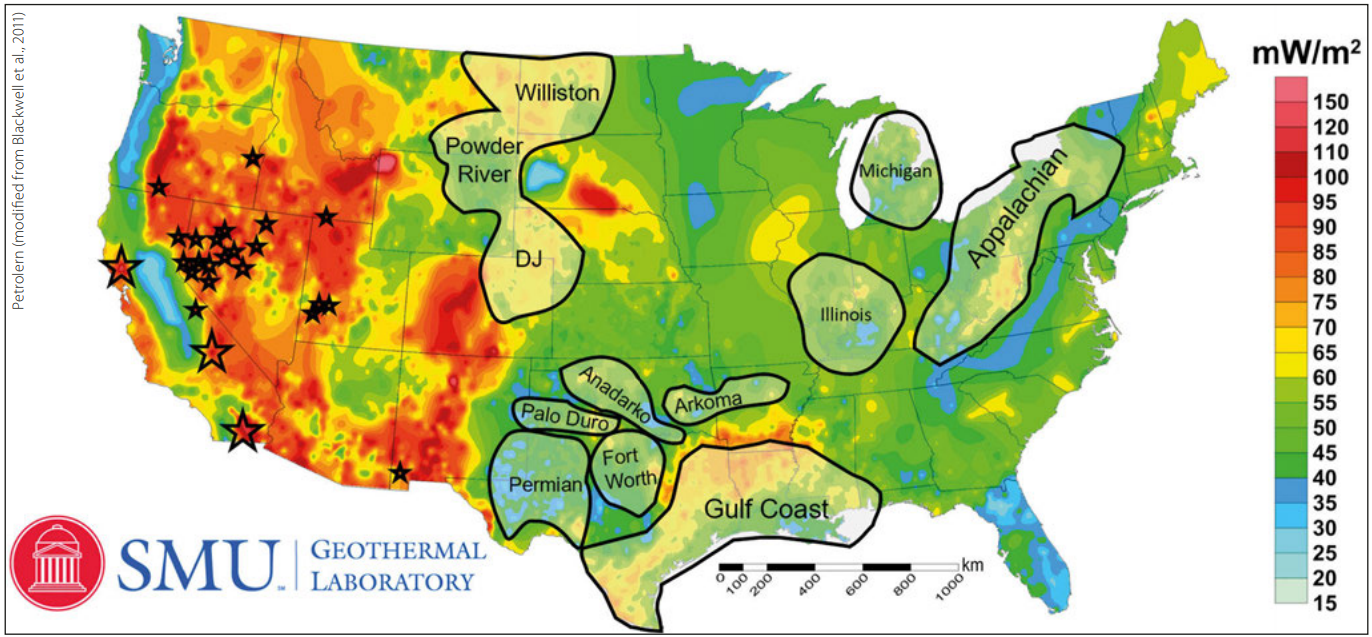

Geothermal energy is the heat within the Earth, slowly cooling like the coffee in your insulated thermos. If you ask a Geologist where you would find geothermal energy, the simple answer is volcanic settings – Iceland, Hawaii, Yellowstone. While this is true, it is not a complete answer. Geothermal energy is everywhere, and we can produce geothermal electricity anywhere with sufficient heat and sufficient fluid to move that heat. The real question is where can we produce geothermal electricity at competitive prices? For the United States, this is currently limited to the western half of the country, in the Basin and Range tectonic province and volcanic centers along the North American – Pacific Plate boundary (Figure 1); however, there are similar geothermal (heat flow) signatures into the central and even eastern United States (Blackwell et al., 2011b; Roberts, 2014; EIA, 2016).

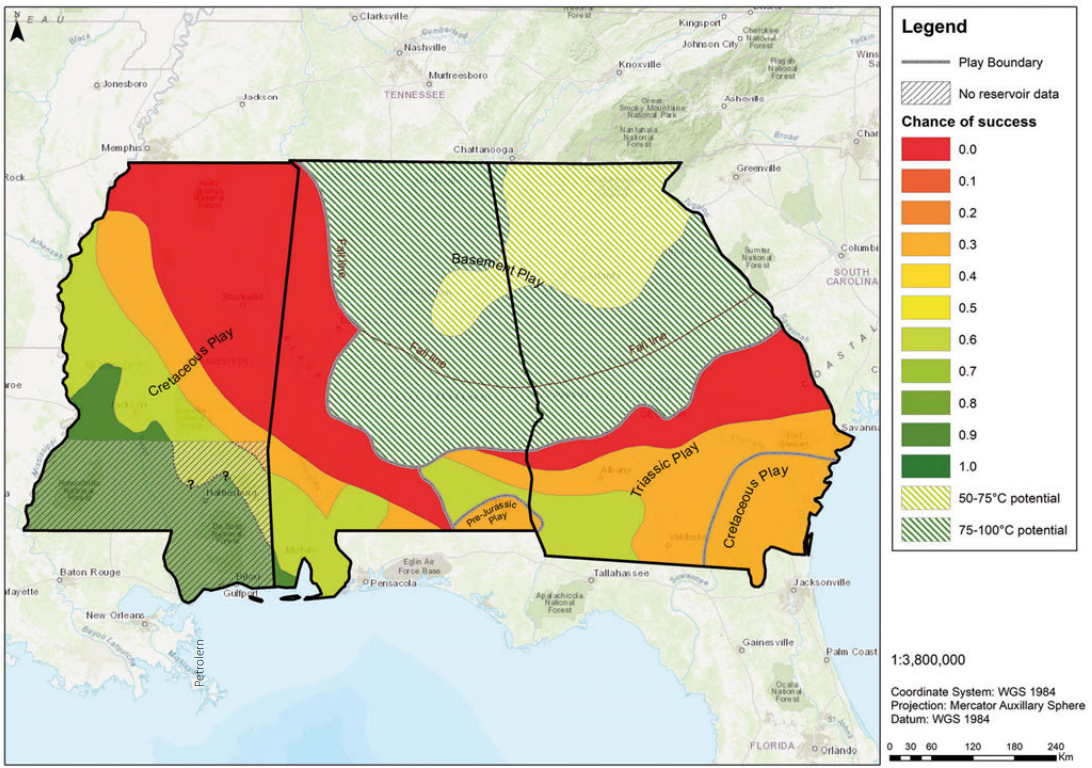

Through recent play fairway analyses, we have found promising geothermal targets within the Gulf Coast Basin with co-located high thermal potential and high porosity, high permeability lithologic sections (Figure 2); still, there is no present-day geothermal electricity production from a sedimentary basin within North America (Petrolern, 2020).

Sedimentary basin hosted geothermal systems have been actively studied for decades; yet, to our knowledge, there are no existing power plants in sedimentary basins in North America. Recent projects can be split into two categories: repurposing hydrocarbon wells for energy co-production or drilling new geothermal focused wells.

Existing Well Co-production

Co-production is production of hydrocarbons while simultaneously extracting heat from the produced water for utilization. An early project demonstrating the technical feasibility of co-production was the Rocky Mountain Oilfield Testing Center (RMOTC) demonstration project that ran intermittently from September 2008 through November 2010. RMOTC produced an average net 170 to 185 kW and showed a technically possible estimated levelized cost of electricity (LCOE) of $0.06/kWh (Williams et al., 2012). More recently a co-production demonstration was performed in the Williston Basin as a partnership between University of North Dakota, Continental Resources, and others. This project proved technical viability of net 124 kW electricity production. The demonstration had engineering issues and did not perform an extended operation phase. Still, LCOE was estimated at $0.0725/kWh based on the limited production data (Gosnold et al., 2017). Both demonstrations presented technical feasibility and competitive electricity cost estimates based on respective location. New technology developments could further optimize power production and further decrease LCOE. Both projects were discontinued because of unforeseen circumstances, which is realistically a risk in any commercial project.

New Drilling

Another opportunity to produce geothermal energy from sedimentary basins is through drilling geothermal wells utilizing new technology. Deep Earth Energy Production (DEEP) successfully drilled and tested a geothermal well in the Williston Basin (DEEP, 2021a) in Canada. DEEP reported that the well was the first horizontally drilled and stimulated geothermal well in the world, as well as the deepest horizontal well in Saskatchewan. The temperature of the production test fluids was ~125°C. In addition to the DEEP project in Saskatchewan, Terrapin has a new drill prospect, the Alberta No. 1, which logged 118°C at 4 km depth in an adjacent well (Terrapin, 2021). No new drilling prospects have published LCOE estimates at this time, but we can estimate based on installed capacity costs.

Investment Size Comparison

There is a significant difference in total capital investment for the different sedimentary basin geothermal energy projects, which requires different investor strategies and different economic metrics. There are two projects in the Williston Basin, one co-production and one a new drilling project. The University of North Dakota-Continental Resources (UNDCLR) co-production system had a net production cost of ~$900,000 for an installed 250 kW (Gosnold et al., 2017), or approximately $3,600/kW. Comparatively, DEEP announced their first power plant will be 32 MW installed capacity and cost approximately Can$8 million (~$5.4 million US$) (DEEP, 2021b) per MW, or approximately $5,400/kW. If we use a direct correlation between installed cost to LCOE, the first DEEP power plant would have an approximate LCOE of $0.105/kWh, or 1.5 times the price of the UND-CLR system. DEEP expects this cost to drop as additional experience produces more efficiency. The difference in installed cost and total investment is ultimately drilling and completion cost.

For both projects, there are additional economic considerations including tax credits, additional hydrocarbon production, carbon emissions reduction, and stakeholder considerations that are not fully incorporated here.

US Gulf Coast Case Study

We recently scoped a geothermal electricity co-production project for an onshore US Gulf Coast petroleum producer. The proposed well had a flow rate of about 7,500 barrels of water per day (BWPD) and wellhead temperature of ~270°F. For this well, a 100 kW net modular power system was selected with an estimated cost of $3,000–3,500/kW. Initial estimates of power production cost including CAPEX and O&M were $0.033/kWh. Comparatively, the client estimated their current electric utility rate to be around $0.09/kWh. We estimated an unofficial internal rate of return range using simple average taxes and straight-line depreciation. If electricity was sold to a third party, internal rate of return (IRR) is approximately 7% for a 20-year system or 10% for a 30-year lifetime. The cost savings to the oil company relative to their current utility charges, and the profit from the hydrocarbon co-production, were not included; but, when accounted for, the overall IRRs would be significantly above the values listed here. While this is only one, more recent example, previous studies examined the Gulf Coast Basin for geothermal energy potential (Figure 3) and found prospective regions all along the Texas and Louisiana Gulf Coast, in addition to the recent geothermal potential zones found in Mississippi (John et al., 1998; Petrolern, 2020). It is clear that co-production and conversion projects are available in multiple areas throughout the world, but petroleum producers are unaware of the geothermal energy they are actively producing and how to utilize it in a profitable and effective way.

What are the Challenges?

With the multiple previous projects and high geothermal potential, why is there not a commercial geothermal power plant in a sedimentary basin? Our experience suggests oil and gas companies do not have or want to allocate the personnel to produce a geothermal resource evaluation, design and optimize a geothermal power plant, and then evaluate electricity markets to determine the most profitable use of the produced electricity. These required skill sets are almost exclusively found in the largest, vertically integrated oil and gas companies, yet they are the minority in the US oil and gas industry. IHS Global Insight (2011) reported that smaller, independent operators accounted for oil and natural gas production of 45 and 65%, respectively, which was trending upward based on 2011 and prior data. The Independent Petroleum Association of America (IPAA) states that current oil and natural gas production by independent operators is 83 and 90%, respectively (IPAA, 2021). Based on these production shares, most oil and gas operators will not have the expertise to fully evaluate a geothermal resource co-located with their existing oil and gas operations.

In addition to the lack of expertise, the ideal well for geothermal energy production would be one with high water production. High water production is often a trait of lower hydrocarbon production, indicative of an end-of-life, marginally economic well. These end-of-life wells become an economic liability, where any additional capital investment is at risk of generating a net loss. With the end-of-life wells, geothermal energy production is a possible additional revenue stream that could extend the producing lifetime of the well; yet, even examining a well for geothermal energy is an additional expense that companies may not want to invest in an already marginally economic well. It is important to highlight, oil companies ultimately must plug and abandon end-of-life wells and might consider a solution that defers such costs and liabilities – i.e., geothermal conversion – if they realized that option was available.

Geothermal Growth Through Screening

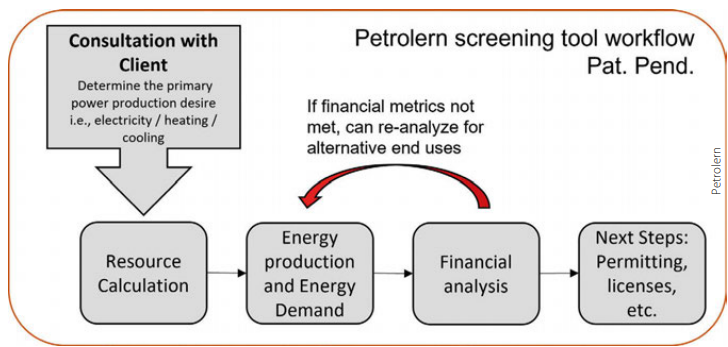

Existing oil and gas wells provide an important, profitable opportunity for geothermal energy expansion, as shown by the examples above, because of the reduced drilling costs; however, wells are often not examined due to the high perceived risk in geothermal energy production from the petroleum industry. Similarly, hiring geothermal experts for evaluation or well workover costs for recompletion is an additional expense that may result in a net loss and is often not approved. A streamlined well screening should be performed in a step-by-step process (Figure 4) as part of the end-of-life assessment to find ideal well conversion opportunities. A streamlined process eliminates low potential wells early, thereby saving time and expenses for detailed evaluation of the most prospective wells, which may prove profitable to a company’s bottom line. The Boak et al. (2021) CSEG Recorder article describes in more detail the benefits of proper screening following the flow outlined in Figure 4.

Screening should follow a similar workflow that provides assessments oriented to the stakeholders’ project objectives, while also providing thermal results if the end user wants to consider additional use options. This means sites are quickly disqualified where wells fail to meet the desired geothermal resource output, or where there is insufficient data to make a direct assessment. If more hydrocarbon wells are screened prior to final abandonment, we expect significant growth in geothermal energy production associated with hydrocarbon-to-geothermal well conversion projects.

Teaching an Old Well New Tricks

There are significant geothermal resources within sedimentary basins, collocated with active oil and gas production, but not all basins will have economic geothermal resources. Some geothermal resources are already being produced by oil and gas operators, yet the geothermal water is discarded. This article focuses on the United States, but end-of-life hydrocarbon wells occur elsewhere in the world and offer an opportunity for geothermal energy production (Boak et al., 2021). Our projections, using real-world water production data and a conceptual conversion, indicate repurposing some oil and gas wells to geothermal heat and power production is profitable with IRRs of 7 to 27%. Sample costs of produced electricity are US$0.03–0.05/kWh. These potential values warrant evaluation of all wells prior to permanent plugging and abandonment. The primary issues hindering geothermal energy production in sedimentary basin settings seem to be the perceived high risk and high cost of geothermal projects and the necessary expertise to perform a full valuation of existing resources in a cost and time effective manner. A screening tool streamlines well evaluation for the oil and gas industry, to facilitate hydrocarbon-to-geothermal conversion. By providing cost effective and efficient evaluation of existing oil and gas wells, we expect more hydrocarbon-to-geothermal conversion and co-production projects within existing oil and gas producing basins, thereby growing the geothermal industry globally and lowering emissions within the oil patch. Conversion of end-of-life wells to geothermal utilization provides additional monetary value while also providing a pathway to decarbonize existing operations.