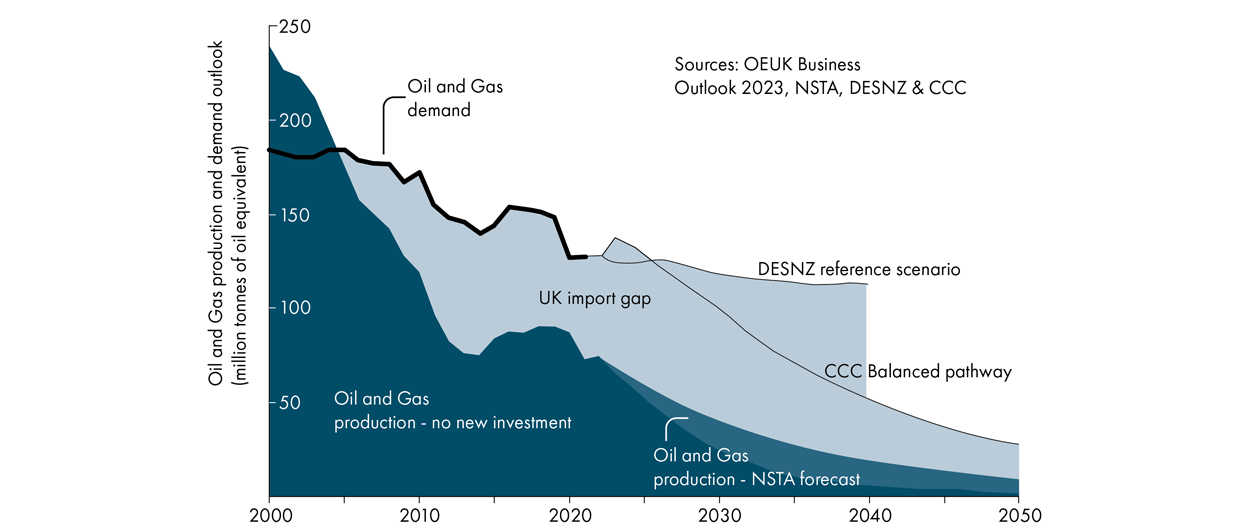

Oil and gas currently provide 76% of the total energy consumed in the UK. As the energy transition progresses, this will decline, but even in the most aggressive demand reduction scenarios, oil and gas are still estimated to provide at least 50% of all UK energy needs over the period to 2050.

Currently, domestic gas production accounts for 44% of the UK’s needs, with oil taking a share of 67%. These numbers may not look too bad, but given the maturity of most oil and gas developments across the UK Continental Shelf, the decline in domestic production will continue steadily as time progresses. That’s why without significant new investment, by 2032 over 80% of the UK’s demand for hydrocarbons is expected to be met by imports.

Resource potential

The UKCS has the resource potential to significantly reduce this import dependency, but requires the right investment climate to achieve this. The latest estimates published by the North Sea Transition Authority include 6.4 billion barrels of oil equivalent of contingent resources and 15.2 billion barrels of oil yet to find.

These numbers may look eyewatering, but if put in the context of a total volume produced from the UKCS already – 45 billion boe – the contingent resources and YTF’s should really be seen as vehicles to slow down the decline in production from existing assets rather than bucking a trend. For that reason, there is no reason to claim that continued exploration will slow down the energy transition. It will only help reduce import dependency.

Reducing emissions

In addition, UK production emissions are declining, and the industry is on track to meet its initial reduction targets enshrined in the North Sea Transition deal. Emissions intensity of UK production is lower than global averages and although some imports are currently better, new UK developments can match or improve upon these low-emission sources. This is because a new development that produces at plateau rates for a number of years will have a much lower carbon footprint than an older platform that still needs to run but with much less throughput.

On top of that, imported hydrocarbons will be primarily derived from higher emissions intensity supply, notably LNG. Replacing imported LNG (88.4 kg CO2/boe) with new domestic gas production (ca. 3 kg CO2/boe) has the potential for a material reduction in emissions, which is equivalent to removing tens of millions of internal combustion engine cars from the road.

In other words, despite the sensitivities around oil and gas exploration and production from UK waters, and the undisputed need to move to a cleaner energy system, the development of new oil and gas fields across the UKCS does not violate the spirit of the energy transition.

This article benefited from data put together by the UK Subsurface Task Force