When assessing opportunities for successful acquisition and divestment of upstream assets, looking into the future can perhaps be compared to driving in the fog en route to catching a ferry. The analogy is interesting as, even if one is familiar with the road, the risk of serious accident is only reduced by slowing down to a safe speed. In the end one is likely to get to the port but probably after the ferry has departed. The options include finding an alternative route where there is less likely to be fog – due to the geography and topographic conditions – even if this involves a long detour, or following the normal route and taking the next ferry – or not going at all. Whether the fog might clear in the meantime is unpredictable – like the current oil price!

In such a low or declining oil price environment, the industry generally knows where it is trying to get to but few decisions are made and new funding becomes largely unavailable, particularly whilst uncertainty continues and until there is some evidence that the bottom has been reached and some confidence returns. How long this will take in the current cycle? Predictions, range from 6 months to over three years.

The Oil Price

Although demand for oil has declined recently, global demand long term is expected to continue to increase. Population and the inevitable continued long term economic growth of China, India and Brazil suggest that demand will eventually catch up with supply. There is a huge gap in the world’s technical experience (as a result of previous downturns in the 1980s and 90s) which will start to severely hit the ability to find new resources in more subtle and complex hydrocarbon plays as the ‘easy oil’ is depleted. In the immediate term, if the price continues to crash (even if the Saudi breakeven point for some of its production is US$5/bo) the world’s largest and most influential oil producers can only sustain such a continuing price drop for a limited period before a global recession. Perhaps the latest decline, exacerbated by the prospect of Iran opening the taps and thus increasing the oversupply even more, will hurt enough of the big oil producers in next 6 to 12 months that they will agree production quotas that ensure their share of production in order to stabilise, if not rebalance, supply to meet demand, leading to a price increase. This is perhaps more of a hope than a prediction, as only time will tell who is right, but I’m not aware of any analyst who has consistently predicted the oil price although it’s likely that one will be right at some time, albeit not consistently!

Survival of the world’s upstream sector in the next few months or years, and preservation of the explorers on whom the long term success of the industry still relies, now depends on available cash flows, cost management and/or preservation of available resources, with the inevitability that a long, drawn out return to oil price stability will see more businesses struggle or even disappear. For some, this may be the first experience of a severe downturn, but I suspect that for most it’s just another one to endure and survive with cuts and downsizing, trusting that in time the price will come back up and the industry will rebalance at whatever price is sustained for confidence to return.

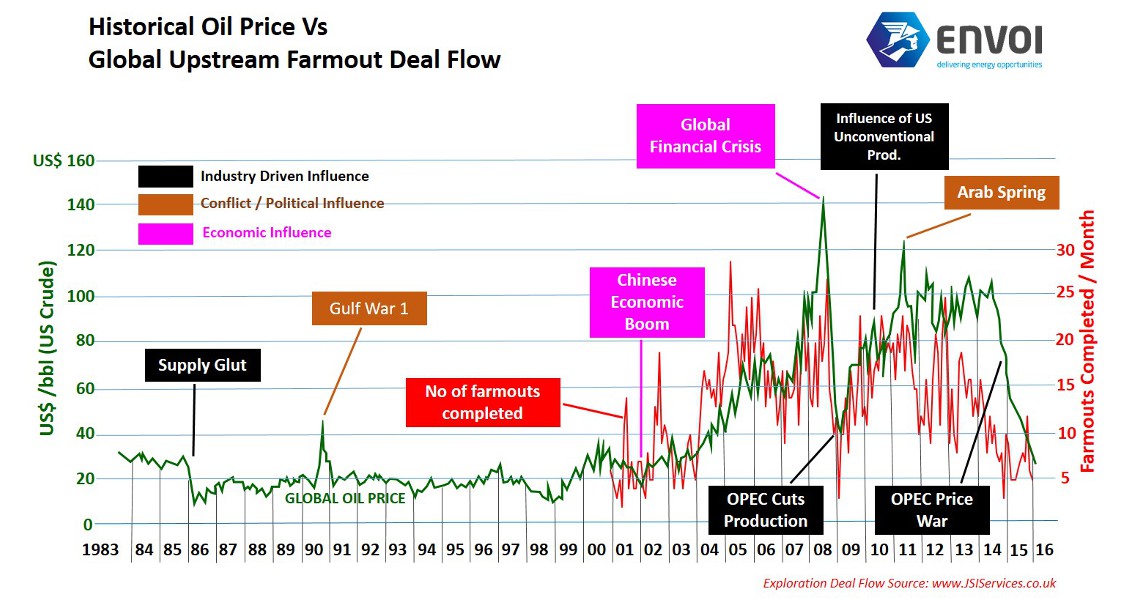

The graph below shows the oil price since the early 1980s and the various key price changes since. Although there are many other influences, these are the major ones. Interestingly, when the influences are catagorised, the historic price changes with the most damaging effect all seem to be clearly linked to industry-driven inflences – and specifically the dominant producers causing the current price war. One wonders how much of this, therefore, might be linked to the change of power in Saudi Arabia since the death of the old king in late 2014.

Oil Price V’s Deal Flow (January 2016). (Source: www.JSIServices.co.uk)

The Opportunity

Although the majority of the upstream sector suffers in such a dramatic global price decline, the old saying, ‘One man’s loss is another’s gain’, comes to mind. Arguably, those investors with resources and confidence that the price will come back up in the next 5 or so years now have a fantastic window of opportunity to invest at the lowest price point (wherever that might be), without a great deal of competition, and cherry pick the best upstream deals at the cheapest price from distressed companies trying to survive.

If one looks at the number of global upstream exploration deals (farmouts, excluding North America) that have been announced since 2000 (source JSI Services Ltd.), we see a close match of deals done per month to the oil price: they decline together. The fact that the same number of deals tends to be available, regardless of the stage we are at in the price cycle, and the fact that on average over the last 16 years the JSI Global Upstream Deals database shows an average 20% commercial success rate of farmout wells drilled globally since 2000 (when the database was started), clearly suggests that now is the right time to invest if one believes the oil price will increase within at least the next 3-5 years. Companies struggling to hold onto their longer term exploration, and even their current production, may call these opportunists ‘vultures’, but buying low and selling high is what drives most free market sectors.

The statistics also show that during dramatic oil price declines, exploration deal flows track the price, only increasing when exploration costs (particularly seismic and drilling) also go down, until the rate of decline slows and bottoms out. Much lower costs for exploration work programmes then coincide with a return of investor confidence and the ability to invest in future exploration deals on very favourable terms. This may sound obvious but many will still miss the turn.

A bit like the initial panic when trying to catch the ferry in the fog, by far the best option is to accept that the journey may take longer but that by making the right decisions and being in the right position, armed with both the facts and expertise (from those who have experienced similar conditions before), the opportunities on the way will dramatically increase the experience and ultimate value. There is funding out there, supported by recent evidence that the initiated are already in process of preparing the investment of significant resources in upstream opportunity in the down cycle with a 5+ year plan.