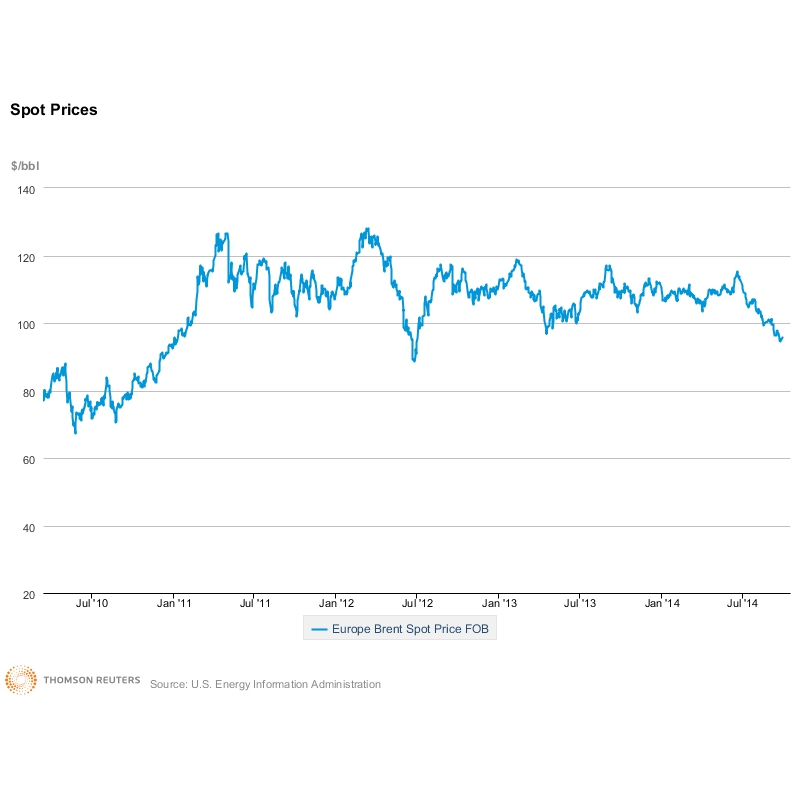

Spot prices for Brent Crude. Prices are calculated by EIA from daily data by taking an unweighted average of the daily closing spot prices for a given product over the specified time period. (Source: EIA).So, it seems the oil super-cycle is finally on its downward turn. Brent is now heading south from the all-important $100/barrel figure: WTI is close to $90. It all seems so counter-intuitive – with the oil world at war prices might have been expected to rise, but the reverse is true. What’s going on? Are predictions of Brent at $85 credible? And what are the implications for the industry?

Spot prices for Brent Crude. Prices are calculated by EIA from daily data by taking an unweighted average of the daily closing spot prices for a given product over the specified time period. (Source: EIA).So, it seems the oil super-cycle is finally on its downward turn. Brent is now heading south from the all-important $100/barrel figure: WTI is close to $90. It all seems so counter-intuitive – with the oil world at war prices might have been expected to rise, but the reverse is true. What’s going on? Are predictions of Brent at $85 credible? And what are the implications for the industry?

The truth is that war in the Middle East has not yet affected supplies. Although ‘Islamic State’ now control six of Syria’s ten oilfields, plus four in Iraqi Kurdistan, it seems that the oil smuggling network is well developed and up to 80,000 bpd is still reaching markets. A new 1 MMbpd pipeline from two southern fields in Iraq is, in fact, helping to boost supplies from the area. Similarly, Libyan output has also risen this year, although there was a significant hit mid-September. If conflict in Yemen escalates, pipelines and shipping could be affected – but at the moment they are not. A jihadi attack on a Saudi gas pipeline early September stoked fears but again, world supplies of oil have remained unaffected.

So possibly the problem is over-supply? All eyes fall immediately on North America’s shale revolution which now supplies the world’s biggest market for light sweet crude, causing a domestic glut with a knock-on effect across the whole Atlantic basin. Would a lifting of the US export ban on unrefined crude help? The ban is clearly depressing WTI but conversely, if it is relaxed the likely effect will be a further stimulation of US production which will only send world prices lower.

Economies Can’t Grow

It seems that supply is not the catalyst for change here. Analysts are waking up to the problem at the other end of the equation – structural changes in demand – and the central conundrum that economies cannot grow while oil is over $100, and that industry cannot invest at less than this price.

In early September the IEA cut its demand growth forecast, stating that the slowdown ‘is nothing short of remarkable’. Consumer behaviour is changing, efficiency measures are having an impact. A rising dollar is adding to the downturn. The question is whether lower prices will, as per the normal cycle, stimulate demand and set off the next upswing, or whether there is now a serious and credible threat to new fossil fuel production.

Those on the cheery side argue that the market will very quickly ‘kick in’. With Brent firmly in contango (ie forward prices far above spot levels) traders are looking at buying and storing, getting ready to sell off when supply disruptions do happen. World inventories are going up. Moreover, the paper traders may well be tempted back into a market that has lost much of its volatility – and therefore its allure – over the last few years. Across the board commodities are at a five year low, but an influx of herd-like speculators could help bid up the price.

Of course the usual solution to a fall in prices is that Saudi Arabia – the world’s swing producer – will cut production in order to stabilise the market. In fact the kingdom did reduce supply by 400,000 bpd in August but with no effect, and although Opec is projecting 2015 demand at 500,000 bpd less than current levels, there appears to be no clear commitment to making this happen. The world awaits the next Opec meeting in November.

What is definitely true is that cuts in capex will affect medium to longer term supplies. Some speculate that shale production in North America will be the first casualty and the speedy nature of this part of the industry may mean that the oil cycle is considerably shorter than usual. Prices could be on the rise again soon if Continental and co find they have run over a precipice.

So, opinions differ widely on where we go from here and how long prices will stay below $100. The political implications of a prolonged drop in prices are huge and scary – think Russia, Venezuela, Saudi, Nigeria… Some analysts are warning of a knock-on effect throughout the financial sector and remind us that falls in commodity markets came before equities in the 2008 crash.

Within the oil industry there will be pressure on service providers – in early August several offshore drillers suffered downgrades and clearly there will be on-going pressure on suppliers. The price drop comes at a time when oil majors were already standing accused of poor performance and those-in the-know claim that serious strategic reviews are now underway. Mergers to reduce duplication of overheads may well happen. But it seems that the nightmare scenario may have arrived: the market cannot bear the price a growing industry requires. Consumers are looking elsewhere.

Nikki Jones,

Bristol

October, 2014

To read more articles and find further analysis visit http://www.exploringoilandgas.co.uk/