In recent years there has been a very low uptake by IOCs for opportunities offered in countries such as India, Pakistan, Bangladesh and Oman, while in Iraq, foreign entries via the licensing round process have been dominated by Chinese companies such as Geo-Jade and Sinopec. While there are undoubtedly valid reasons for the low interest, including above-ground considerations and often sub-industry benchmark commercial terms, it is difficult not to feel that these countries are possibly superficially overlooked by investors in search of more familiar options closer to home. This has historically led to firms underestimating the long-term merits of a new country entry and missing out on well-established oil and gas reserves and mature geological plays.

Opportunities in Indian and Bangladeshi exploration markets

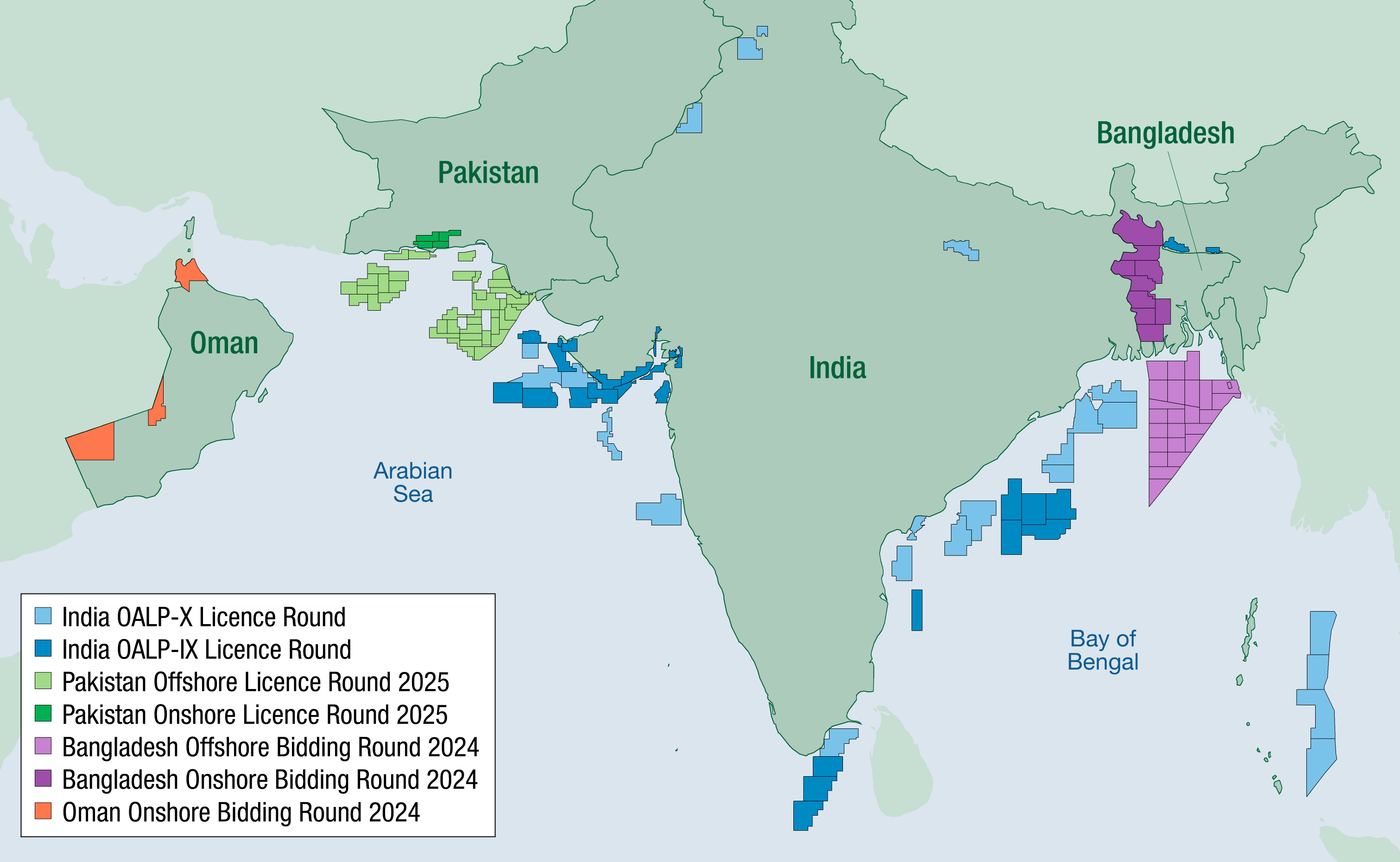

India opened OALP-X, its largest-ever exploration acreage offering, comprising 25 blocks covering a total of 191,986 km2 in 13 basins, in February 2025. The round is open until the end of July. While all blocks offered in the previous OALP-IX round in 2024 received competing bids, no awards have been formalised, and it would presumably inspire investor confidence if the results of the prior round were determined before progressing too far with the current one. Meanwhile, bp, having generated significant publicity in February 2025 by back-tracking on its previously stated renewable energy targets, is courting India through signing a comprehensive MoU for exploration with state entity ONGC, a regular winning bidder in the OALP rounds.

Acreage on offer in OALP-X includes four deepwater blocks to the east of the offshore Andaman Islands, in the backarc basin setting where there have been exploration successes in recent years to the south, in Myanmar and Indonesian waters. While state-backed company OIL’s first well in a current campaign is to the west of the Andaman Island chain, in the forearc basin which has seen limited success to date, ONGC in March spudded an ultra-deepwater well, ANE-E, in the backarc basin to the east. If successful, this will be a play opener and highlight the attractiveness of the blocks on offer. Both OIL and ONGC have further drilling planned for the Andaman region. Bangladesh offered a comprehensive offering of offshore acreage in 2024, but despite numerous international companies subscribing to the seismic data package acquired by TGS specially for the round, there were no bids. Petrobangla is expected to re-launch the round in April 2025. TGS has indicated that the lack of bidding interest was due to above ground issues rather than the geology. While Bangladesh has in the past suffered due to perceived unfavourable commercial terms, the model PSC had been updated for the round, and it is possible that the political unrest of mid-2024 deterred bidders. Onshore blocks are also on offer, and Chevron is reported to have bid for an unspecified onshore block, possibly adjacent to its producing Surma Basin gas fields.

Pakistan and Oman: A shift in focus for regional exploration

Pakistan has an offshore bid round currently active, offering significant tracts of the Indus Delta as well as the frontier offshore Makran area. The deadline for the round was recently extended from mid-March to end June 2025. Pakistan’s previous round saw bids by the state-run and domestic entities and the Chinese-led UEP.

Across the Arabian Sea, Oman had been expected to offer offshore Block 18 which would offer geological contiguity with Pakistan’s Makran coast. However, the blocks announced in early February 2025 as available in Oman are three onshore blocks (Blocks 36, 43A and 66) including recently relinquished acreage.

Delays and variations to expectations (in blocks, fiscal terms and timing) such as these may deter company confidence in the licensing round approach to gaining acreage in the region. However, the award of Block 54 (Karawan), ensuing from Oman’s 2023 onshore bid round to new entrant Genel Energy, partnering with state-backed OQ as an operator, announced in March 2025, is encouraging from the bid round outcome perspective.

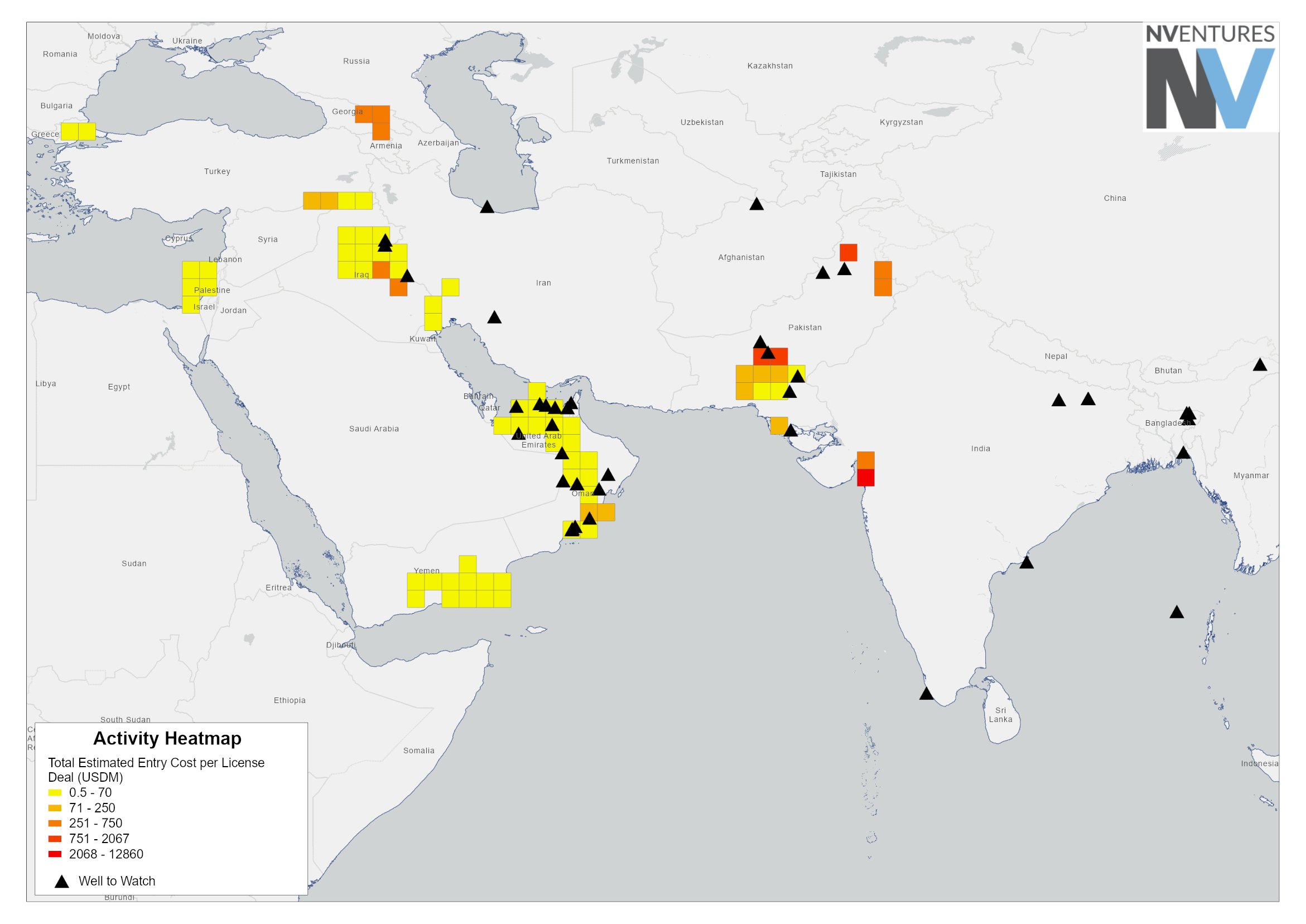

Considerable levels of current and forthcoming exploration activity in the region, highlighted by the NVentures Wells to Watch map, mean the significance of high-impact exploration successes, such as ONGC’s play-opening Chola-1 in the deepwater Cauvery Basin, and Mari Energies’ Spinwam-1 in the Bannu Basin onshore Pakistan, could be overlooked in the international E&P space. However, with the countries under discussion continuing to make significant strides ahead in the New Energy sector, in which Solar, Hydrogen, Wind and CCS projects are all gaining traction, seeking an exploration entry into one of the MESA countries by way of a bid round could be seen as a good way to ally with energy transition projects and thus enhance green credentials and deliverables.