The level of carbon dioxide in the atmosphere last year surged at its fastest rate in 30 years according to the UN Meteorological Organisation, possibly indicating that the world’s oceans and forests are no longer able to store the gas as they have done in the past. Although the world is aiming at emission levels of 1 to 1.5 tons per head per year, we are currently close to 40bn tons annually across the globe and on track for a four degree warming by the end of the century, a temperature that will change both the human and physical geography of the planet.

Governments’ options are varied but unpleasant – stopping deforestation, discouraging livestock farming (to curb methane production), reducing international travel and trade, cutting consumption generally. Faced with such unpopular choices governments are looking for substitutes to the fossil fuels that are the source of 87% of global human carbon dioxide emissions. Power production is the primary focus given the global move towards the electrification of heat and transport.

Coal-fired power generation is seen as the primary culprit as, at the power plant, it produces roughly twice the emissions of gas – as well as health damaging, smog-creating pollution. The low efficiency of most coal-fired plants – a global average of 33% – has helped focus the attention of governments.

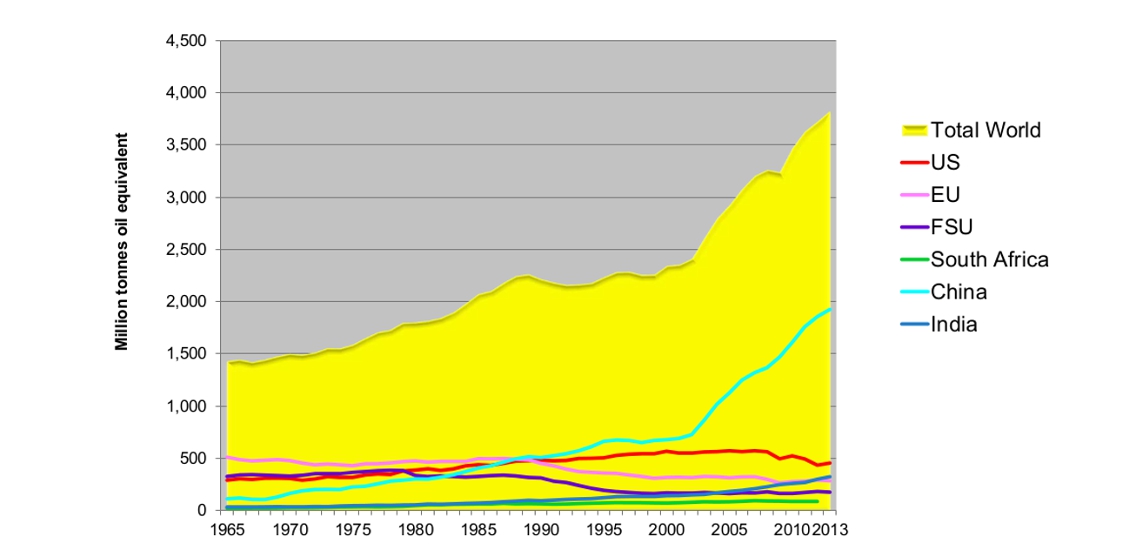

Coal consumption in selected countries since 1965. (Source: BP statistical Review of World Energy 2014)

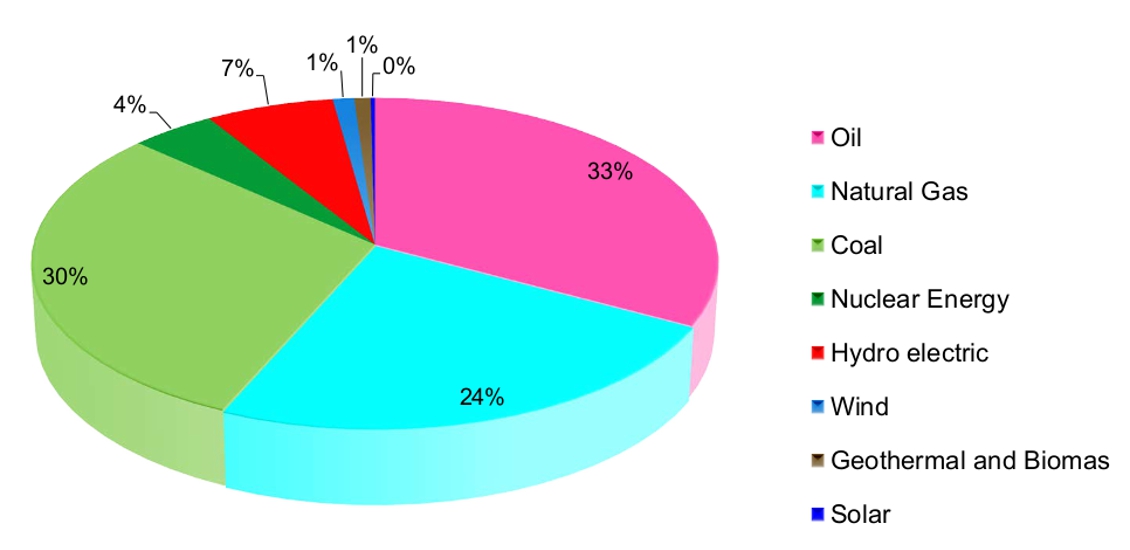

Global energy consumption 2013. (Source: BP statistical Review of World Energy 2014)

However, according to the IEA, in 2014 coal was still the world’s principal fuel for the generation of electrical power, a total of 1,700 gigawatts, 41% of global consumption. This has been fuelled by low prices as exports from the US have surged, following the shale boom, and there has been increased production from Australia, Indonesia, Colombia and South Africa. China’s growth has fuelled this ramping up: the country now accounts for almost half of global coal consumption, a marked increase on its 25% share two decades ago.

There has been a fair amount of finger-pointing at China but, in fact, neither the US nor Europe have managed to wean themselves off coal. In Europe coal consumption began rising again in 2009, fuelled by the failure of the carbon pricing mechanism, as well as Germany’s closure of nuclear plants. US consumption has been declining, but the Environment Protection Agency still anticipates coal will produce 30% of America’s power in 2030. Creeping up on the inside, India accounted for 21% of global growth in 2013 and is set to overtake China as the world’s biggest coal importer.

Tiananmen Square enveloped by heavy fog and haze in January 2013. Many of China’s cities face serious air pollution and poor air quality. (Source: axz65/123RF.com)

Gas as a Substitute

The industry is pushing gas as a substitute, claiming that it is far cleaner than coal and can have the added advantage of relatively speedy reaction to fluctuations in grid demand. Instability in grids has been heightened by the switch towards intermittent renewables, now generating 22% of the world’s electricity. In recent months Japan has announced that it is closing its grid to large-scale renewable generation because of this problem.

Backing up the argument for gas, manufacturers are now show-casing larger and more efficient turbines, capable of ramping up to full power within 30 minutes and with relatively low turn-down levels (40%).

However, both the industry and governments are asking searching questions, not only about the economics of a shift to gas but also security of supply and the actual claims of comparative cleanliness.

The argument for gas lies in the fact that it is twice as clean as coal at the power plant. However, there is real difficulty in comparing the two fuels when the whole production-fuel cycle is factored in, since each coal and gas field has its own production methods, processing requirements and different distances from markets. Emission levels will depend greatly on the CO2 concentration in the raw gas, which can be as high as 14% mol, and processing and transport add substantially to the equation. LNG requires the super-cooling of gas to -162°C, ocean shipping in cryogenic sea vessels, regasification and pipeline distribution. There are wide variations in thermal efficiencies at liquefication and regasification stages dependent on the type of gas turbine used and the choice of process when reheating, and 85% of current carriers are fuelled by low efficiency (approximately 27%) heavy fuel il and boil-off gas. One estimate is that LNG, usually transported over distances of 3,000 km or more, consumes, on average, 25% of the energy transported.

Gas pipeline transmission has, to an extent, been below the radar, but a recent European Commission study found that over long distances (~7,500 km) pipeline greenhouse gas emissions are equal to those from LNG transport. These emissions are associated with the energy required to overcome frictional losses and also to maintain the pressure in the line.

Local leakages in distribution networks – almost 100% methane – are also a significant factor. In July this year the EPA reported that fugitive emissions from distribution pipelines in 2012 accounted for more than 13 million metric tons of carbon dioxide equivalent emissions, 10% of the total coming from the US natural gas industry.

Emissions in Gas Production

Emissions associated with conventional production (still the major source of gas) have also not been factored in to the ‘cleanliness’ argument. They depend on the energy used in dehydrating the gas, sending it to a treatment plant, guaranteeing the energy supply to the facilities and enhancing production with water injection, plus the characteristics of the gas produced. Analysts Altran Italia calculate that greenhouse gas emissions at this stage are typically between 0.95 and 1.5 kg/m mBtu, 15% of which are fugitive emissions and 5% flaring.

Emissions for shale gas, tight gas and coalbed methane are far higher than conventional gas sources. According to the IEA, this is partly because of the need for more wells and more hydraulic fracturing in order to maintain output – usually powered by diesel motors – and partly because of more flaring and venting during well completion. During the early flow-back period, when there is more fracking fluid than hydrocarbons, companies do not always separate and process the gas: at this stage it is mostly methane with a small fraction of volatile organic compounds. These emission levels are compounded by fugitive emissions plus incidents of ruptured equipment. There is also a need for local transportation, and there are emissions associated with water supply and waste water management.

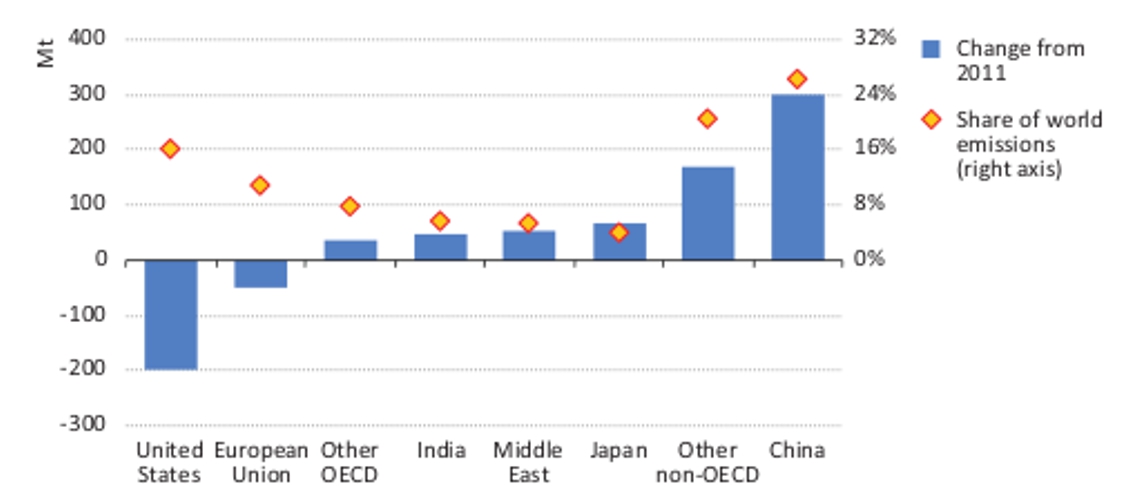

CO2 emissions trends in 2013. (Source IEA)

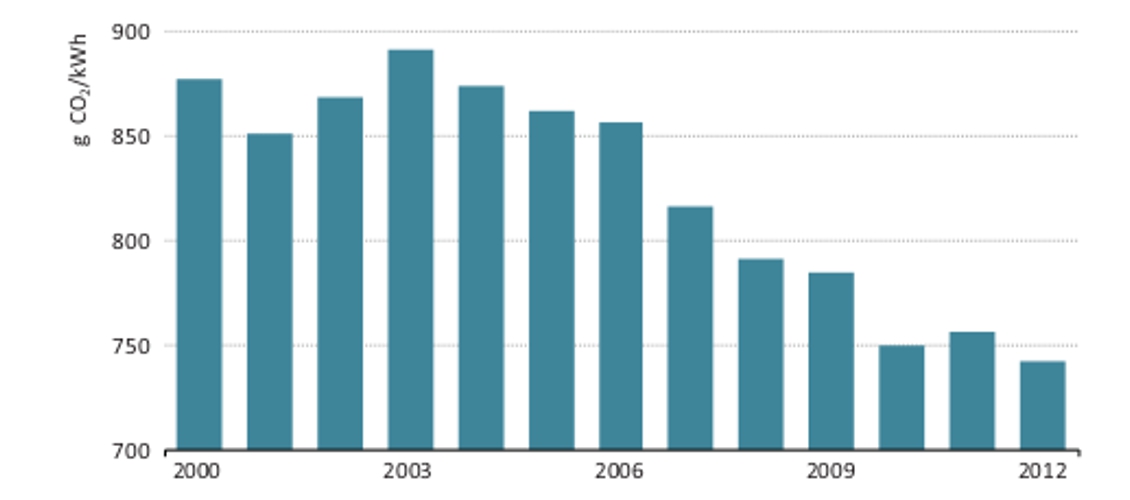

CO2 emissions per unit of electricity generation in China. While China made the largest contribution to the global increase in CO2 emissions in 2012, this level of growth is one of the smallest in the past decade, reflecting China’s efforts in installing low carbon generating capacity. (Source IEA)

Is Gas the Answer?

Despite these considerations, governments appear to have been swayed towards the environmental benefits of gas – though they are more hesitant when considering the economics and the geo-strategic risks. Energy security has risen on the political agenda: in particular, the Ukrainian crisis has focused European minds on the continent’s dependence on Russia, since approximately 30% of its gas comes from its neighbour.

If Europe is to pursue a new dash-for-gas, there are few economic, secure, politically acceptable sources of growth on offer. The most likely are Qatar, which already provides 10% of Europe’s gas, and the Southern Gas Corridor through Azerbaijan, Georgia and Turkey, which is expected to supply 20% of Europe’s needs by late 2018. Neither offer security of supply and the Caspian gas solution still requires another $28bn just to bring gas to the Georgian-Turkish border. Increased gas from Russia is unlikely given the current political climate. The South Stream pipeline, which would have brought Russian gas to Europe via Bulgaria, has been put on hold, and sanctions against Russia have effectively halted Russian shale and Arctic production.

China, like Europe, is heavily dependent on Russia, though this is less politically troublesome: approximately 40% of China’s gas comes from central Asia and this year the government finally signed a $400bn deal with Gazprom.

At first glance the US gas glut offers a solution. Producers are begging to export as production in the Marcellus basin alone is up 800% over the last five years, and in September the local spot price plunged to a seemingly unviable low of $1.5686 per mBtu. Three LNG export projects have got the go-ahead to begin construction and 13 more have filed for approval, plus there are proposals for another 13 plants on the west coast of Canada.

However, the argument of energy security from the US falters if the US gas glut is not assured for decades ahead: even before the current oil price collapse, many were arguing that simply increasing the concentration of fracking wells was unsustainable and that production would stagnate in the early 2020s. Current prices have only exacerbated those fears. Nor is US shale gas a cheap solution when investments into liquefication, transport and regasification are added to the equation. In June this year the IEA warned that the high capital costs – an expected $735bn by 2035 – are likely to constrain the LNG industry.

Is local unconventional exploration the answer? Germany has, this year, relaxed its opposition to fracking and the UK government has come off the fence and given full support to the industry. China has been issuing fracking licences for several years. But commercial viability remains unclear and given the generally higher environmental regulations and political objections in Europe, it seems unlikely that shale gas will make a serious, near-term impact on supply or price.

The Opportunity Cost

It appears that there is no clear win for gas on the three key criteria: cost, security of supply or even cleanliness. Its utility is as a back-up for the intermittency of renewables and some governments in Europe are now pursuing capacity mechanism strategies, paying producers for potential rather than actual output.

However, each dollar invested in gas locks the world further into a future of burning hydrocarbons that scientists tell us we cannot afford. Each dollar invested in gas is a dollar that isn’t invested in more and diversified renewables, or the storage and transmissions research needed to overcome the intermittency problems. It has been likened to dieting on fat-free biscuits – i.e. not addressing the fundamental problem.

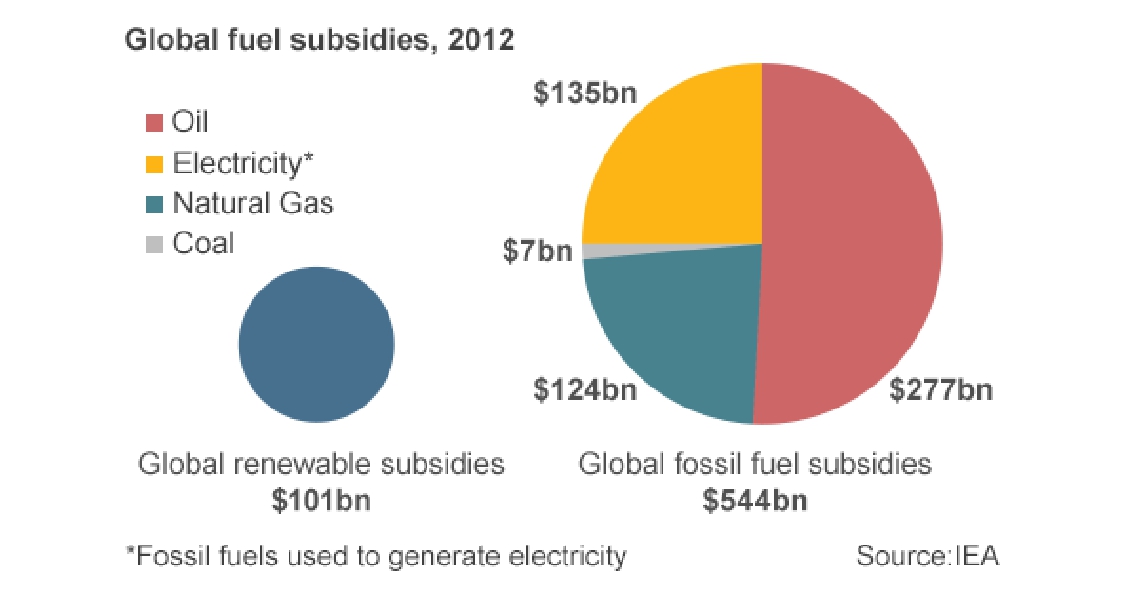

Although green investment is on the rise again after a few years of decline, mainly in China and Japan, the amounts spent – $56bn from China last year, $48bn in Europe and $36bn in the US – continue to be dwarfed by the $600bn given to the fossil fuel industry in subsidies. Now that many renewable sources appear to have achieved cost competitiveness with gas-fired power, scientists and environmentalists are arguing this investment needs to be diverted into energy conservation (which, according to the IEA, has already delivered a 5% cut in consumption across 18 OECD countries 2001–2011), interconnectors and inter-country markets. For Europe, that means geothermal from Iceland, solar from north Africa, wind from Spain; China and the US have similar opportunities with fewer political complications.

The Risks

Without really clear government direction, the risk is that coal will continue to win out on cost and security-of-supply concerns. In Europe a late October summit has delivered a target of 40% cuts to greenhouse gas emissions by 2030 (from 1990 levels) but following pressure from east European states that are heavily coal dependent, countries do not have targets for renewable generation. In the US a Clean Power Plan is targeting coal-fired power plants, but coal is still expected to supply 30% of the country’s needs in 2030. A new wave of hydroelectric stations mean that no new coal fired plants will be built in China’s industrialised east, but the country will remain heavily dependent on coal for the foreseeable future. The greatest threat to reducing coal consumption is the current glut and low price, not government decisiveness. It appears that governments are simply side-stepping the four degree problem.

A coal-fired power plant adding its emissions to the atmosphere. Unfortunately carbon capture and storage is not the hoped-for solution. This year SaskPower in Canada launched the world’s first large project but the problem of CO2 leakage has not been overcome and the technology doubles capital outlays and reduces the amount of electricity to sell. (Source: Kodym/Dreamstime.com)

A coal-fired power plant adding its emissions to the atmosphere. Unfortunately carbon capture and storage is not the hoped-for solution. This year SaskPower in Canada launched the world’s first large project but the problem of CO2 leakage has not been overcome and the technology doubles capital outlays and reduces the amount of electricity to sell. (Source: Kodym/Dreamstime.com)