The 1959 giant Groningen gas discovery made by NAM, the joint venture between Shell and ExxonMobil, transformed the energy landscape of Western Europe. It also formed the starting shot of a highly successful exploration bonanza across the North Sea that led to huge Rotliegend gas discoveries, especially in UK waters.

The 1959 giant Groningen gas discovery made by NAM, the joint venture between Shell and ExxonMobil, transformed the energy landscape of Western Europe. It also formed the starting shot of a highly successful exploration bonanza across the North Sea that led to huge Rotliegend gas discoveries, especially in UK waters.

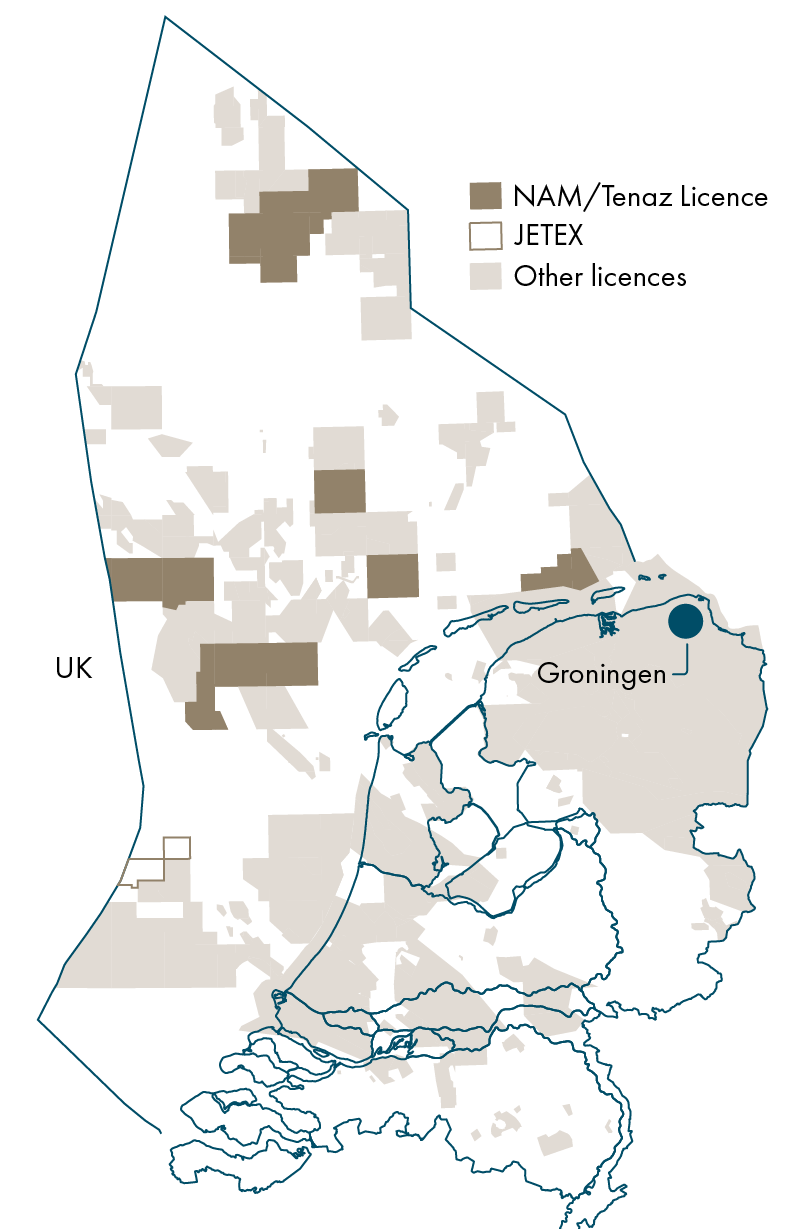

Groningen production started in 1963, but following reports of small earthquakes caused by pressure depletion, the Dutch Minister of Economic Affairs and Climate put the break on production in recent years, ultimately leading to full closure of the field last year. There is still gas production from nearby smaller fields to heat local homes, keep industry running, and lessen dependence on foreign gas supplies.

The rapidly falling production from these smaller fields, in addition to the early closure of the Groningen field, has now turned the Netherlands from an exporter to a net gas importer. However, the Minister of Economic Affairs and Climate still supports the exploration and development of gas from its North Sea sector, stating this is preferred over imports. There is still running room left in the county’s offshore, and with its shallow waters, infrastructure and, of course, a hungry energy market, it makes small accumulations commercial with fast returns on investment.

Opportunities

Energie Beheer Nederland B.V. (EBN), representing the government’s interests in the extraction of energy resources, has outlined in an excellent publication the concepts and scope for exploration in the mature Dutch offshore province, including several overlooked plays. One such company that is active in exploring innovative ideas is UK-registered JETEX Petroleum. Operating Blocks P8b and P10c with partner EBN, JETEX is targeting the Carboniferous Namurian sands and Dinantian carbonates near the international border with the UK within the prolific Southern Gas Basin. Several seismic amplitude-supported prospects have been mapped.

Deals to be done

On the deal side, the industry is still very much alive in the Netherlands. None more so than the announcement in July 2024 that Tenaz Energy from Canada had entered into an agreement with NAM to purchase its offshore exploration and production businesses, associated pipeline infrastructure, and onshore processing facilities, excluding assets in the Ameland area. The US$180 million deal is expected to close by mid-2025. The deal will make Tenaz the second-largest operator in the Dutch North Sea. Tenaz is familiar with the Netherlands already, holding both upstream and midstream assets. Tenaz entered the country through its purchase of a private company in 2022 and XTO Netherlands in 2023.

With the sorrowful winddown of the UK oil and gas industry, luckily, sense still prevails in the Netherlands, and the offshore represents an attractive option for disillusioned companies on the other side of the median line.