Apart from Norway, the UK Continental Shelf saw the highest number of seismic surveys acquired when looking at a global overview over the past ten years. Is that something to cherish as a UK exploration community and use as proof that there is actually a lot going on?

Maybe not so much, when listening to Graeme Bagley’s presentation at the Seismic Conference in Aberdeen. “Most of these surveys were postage stamps,” he said when I spoke to him afterwards.

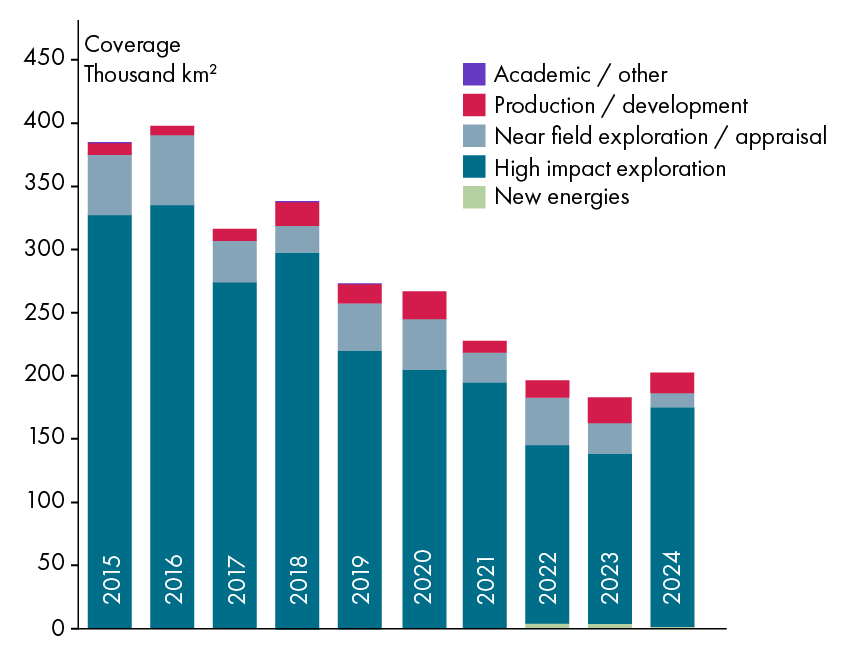

This observation seems to correspond with a global trend when looking at overall seismic acquisition activity over the past ten years, as Graeme illustrated in several ways through the work performed by his colleagues from Westwood Global Energy Group and Seisintel.

In 2015, about 400,000 km2 was surveyed; in 2024, it stood at slightly north of 200,000 km2.

“It is a tough game the industry is in,” said Graeme at the start, “and these numbers are probably the reason why the business is tough.”

Then the question can be asked, are we now at a turning point towards an increase in surveying activity in the years to come, or is it a matter of continued decline?

When looking at high-impact exploration drilling activity over the same period, it is very hard to see a trend. Where trends in oil price and the number of exploration wells drilled was nicely coupled, despite there being a small time-lag, that relationship broke down around 2020. Oil prices rose again after the Covid slump, but the number of wells drilled has not and stabilised at most. “Capital discipline at times of enhanced volatility” is how Graeme called it.

So, I guess it will be difficult to predict the future, but what is more certain is that the global prospect portfolio is drying up this way. In support of that, Graeme showed that from the moment a survey is acquired, the success rate of wells drilled on that survey drops off after five years. This probably relates to the observation that a good prospect will stand out on a new acquisition, forming an immediate momentum to drill and not wait. If there is no obvious candidate, there is more of a chance for the data to be “forgotten” for a little while.

It will be really interesting to see how the industry is developing over the next few years, but if there is a trend that provides ammunition to those wanting to see the end of high-impact exploration, at least by the IOC’s, it is the graph shown here.