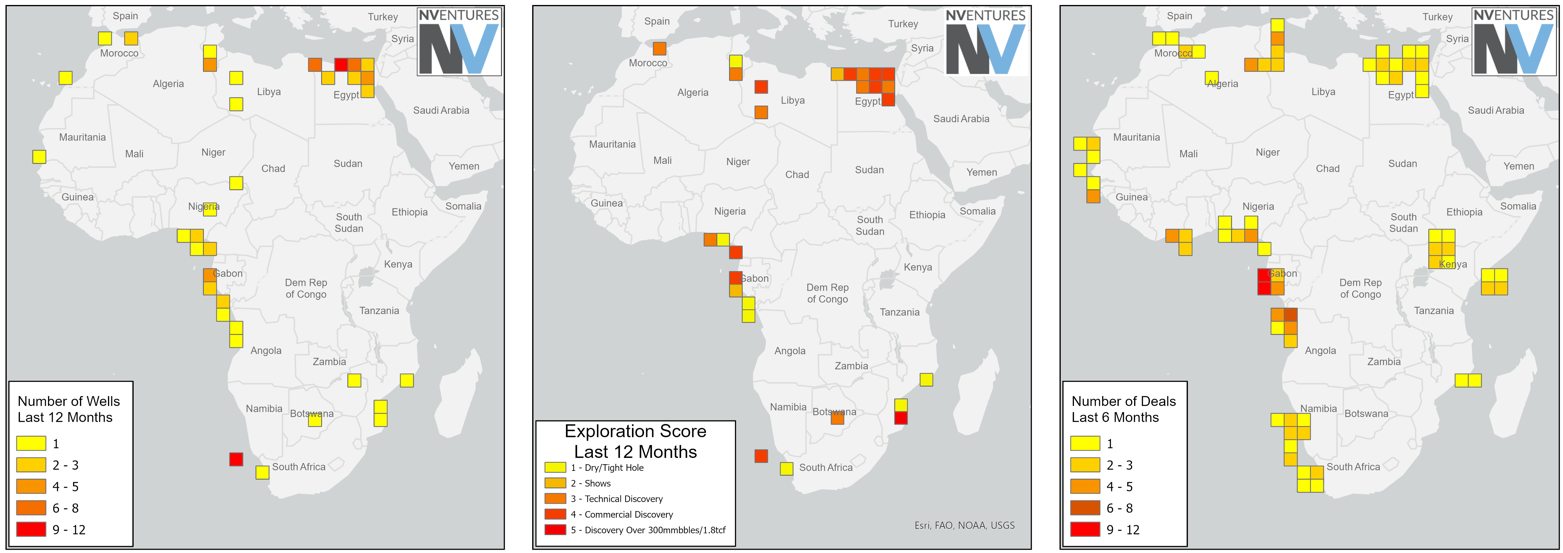

E&P across Africa in 2024 is off to a busy start, with clear signs the exploration industry is recovering from half a decade of under-investment. Exploration activity is still focused offshore and predominantly in deepwater, whilst appraisal and development remains focused in mature basins in shallow water and onshore. Onshore exploration remains woefully overlooked, although it’s good to see new drilling and licence awards onshore in the Kwanza Basin in Angola.

Established basins take the limelight

In terms of deal flow, established basins in Angola, Congo, Nigeria and Egypt take the limelight. The Orange Basin remains a focus for equity transactions, while large gaps remain in the West Africa Transform Margin and East Africa. Major deals of interest include the Renaissance JV (ND Western, Aradel, First E&P, Waltersmith and Petrolin) in Nigeria buying Shell’s shallow and onshore portfolio, Perenco taking ENI’s mature assets offshore Congo and TotalEnergies increasing its dominant position across the Orange Basin with deals on the Venus Block and also 3B/4B in RSA. Vaalco swooped on the Svenska stake in Baobab in CDI, which may in turn trigger more deals in this area.

Drilling activity over the last few months exhibits a similar trend, with a gradual upturn in activity, exploration in deepwater, and appraisal and development concentrated in shallow water and onshore. Whilst fast-paced exploitation companies like Panoro, Perenco and AOC take advantage of late-life field development, supermajors are left to push the envelope on deepwater frontier drilling. Of note are the new deepwater discoveries in Namibia at Mopane (Galp) and Mangetti (TotalEnergies), and in Cote D’Ivoire where Eni extends its run of success with another giant discovery at Calao with the Murene 1X well. Sasol continue to drill up gas in the PT area, and Invictus report promising results at Mukuyu 1 in Zimbabwe. However, there are no wildcat successes to report from offshore East Africa.

New developments

New oil and gas developments are coming on stream this year in Senegal (Sangomar) and Mauritania (GTA LNG project), while Eni are gearing up to produce 3 mmtpa LNG from the new Congo FLNG projects. Jubilee Southeast has proven successful for the Tullow Group in Ghana, although TEN is failing to deliver, and Egina West is up and running for TotalEnergies and partners in Nigeria. In mature basins firms such as Assala in Gabon and Perenco in Cameroon, Congo and Gabon continue to extract maximum value from late-life assets previously held by the super-majors.

A buyer’s market for exploration

Looking ahead, there are a good number of opportunities to continue the growth in E&P investment on the continent. A large number of active data rooms are seeking the attention of international new ventures teams. Many firms are seeking partners to fund new 3D, especially in promising areas like the Walvis Basin (Namibia) and the southern MSGBC. In general, it remains a buyer’s market for exploration, with not many farm-in deals achieving more than ground floor terms, and a seller’s market for appraisal and production, with many firms lining up to pick at the remains of mature producing fields and basins.

Activities to keep an eye on

Major opportunities for drilling exist across the continent, with firms seeking partners or investment in high-impact drilling campaigns. In Ghana, Heritage and other firms have low-risk drilling opportunities in the Tano Basin in and around Jubilee. The MSGBC hosts a number of exciting opportunities to drill multi-billion barrel prospects, including Supernova in Guinea Bissau and Petronor in Gambia.

Several significant campaigns stand out, such as the planned wells in the Herodotus Basin offshore Egypt where ExxonMobil and Chevron separately have wells planned. In South Africa, TotalEnergies are reported to have up to 5 wells planned to test the central and southern Orange Basin, and the government in South Africa is quickly putting into place new institutions and regulations to encourage future development of resources.

ExxonMobil is set to drill the Namibe Basin offshore southern Angola; a successful campaign here could open another oil and gas front in neighbouring Namibia. Junior explorers are picking up momentum as well; Petrodel and Octant plan to drill large targets in the Pemba coast in Tanzania, Conjugate Energy are planning two wildcats in southern Uganda, and all eyes are on Guinea Bissau as Apus gear up to drill the long-awaited Atum well.

So, it is fair to say that after having weathered the perfect storm of low oil prices, investor boycotts and global lockdowns over the last few years, high-impact exploration in Africa is back on the map.