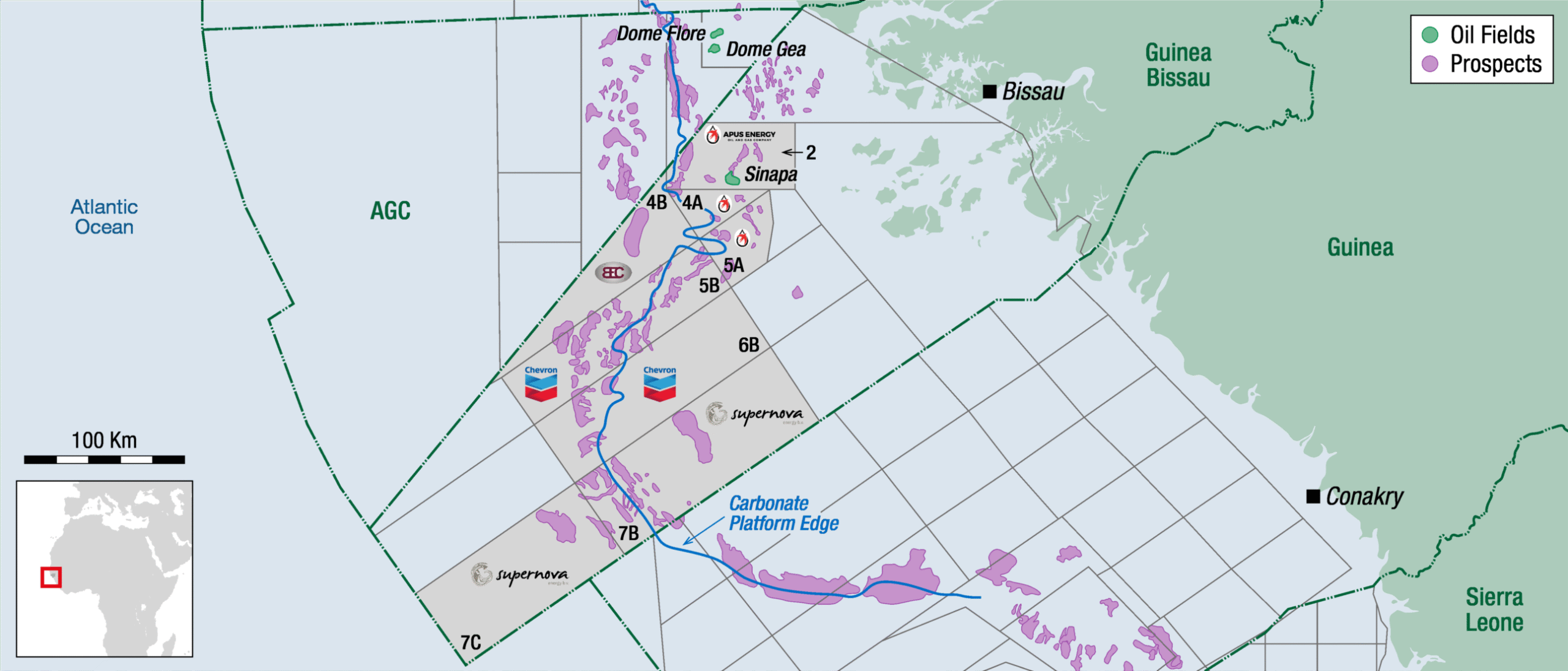

Guinea-Bissau exploration update map. Source: NVentures.

The search for barrels in Bissau – exploration renascimento in the southern MSGBC

Investor confidence is returning to the West African oil frontier as major companies pursue world-class prospects across the Guinea-Bissau deepwater basin.

Investor confidence is returning to the West Africa oil frontier, with major oil companies taking large basin-scale positions in Guinea-Bissau, Liberia and Sierra Leone. The map of West Africa offshore concessions has been a blank canvas since 2015, with the tremendous oil potential of these basins remaining dormant until now. Major drilling campaigns from Benin to Mauritania were curtailed in 2020, as the exploration industry found itself in a perfect storm of low oil prices, poor investor sentiment, toxic environmental activism and the pandemic. As shown by Chevron’s entry into Guinea-Bissau, the world is learning to celebrate oil again.

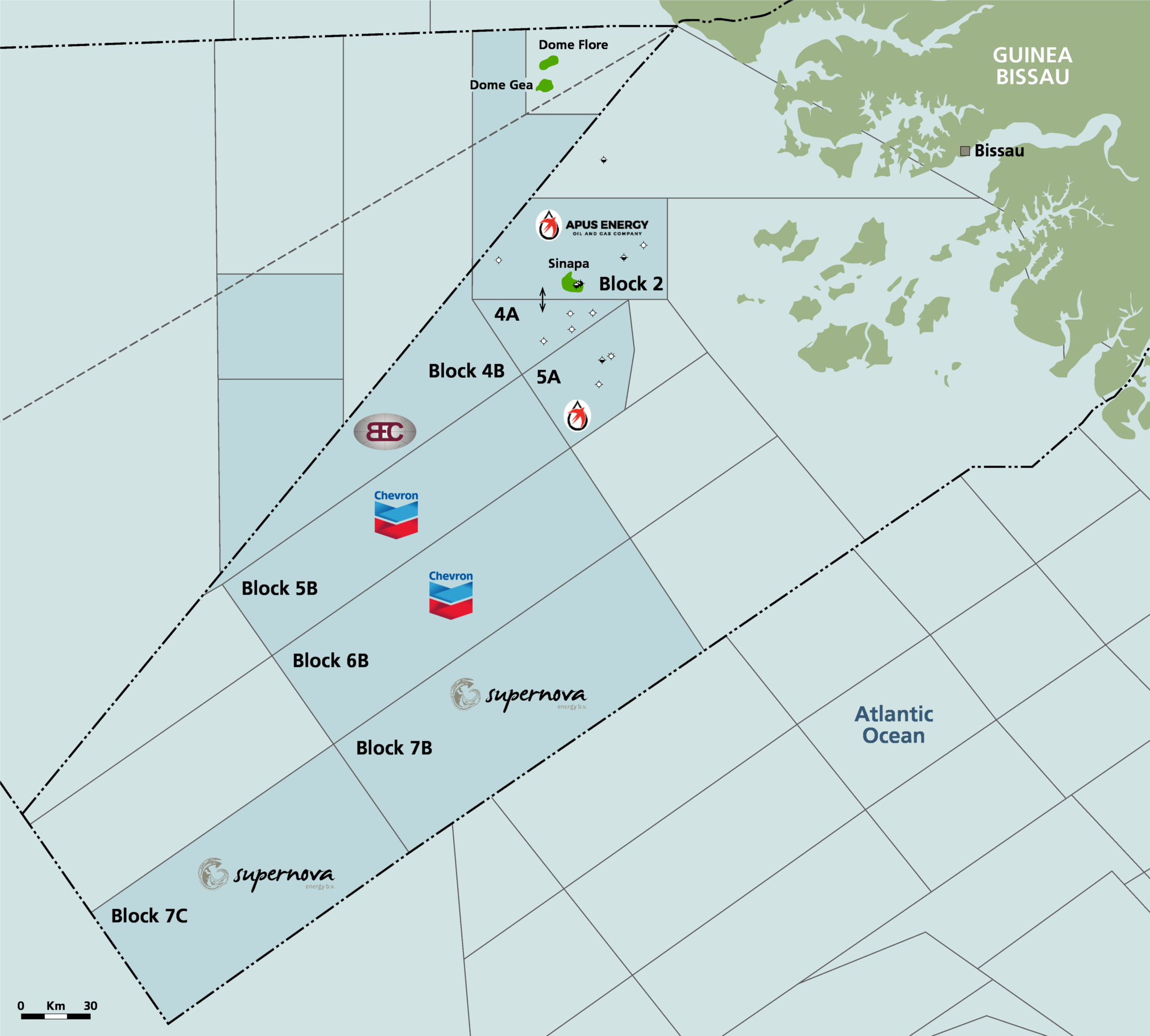

Guinea-Bissau has played host to a fluctuating oil industry over the decades, but always underpinned by strong petroleum geology, professional industry management by Petroguin, and an excellent fiscal regulatory regime. The country is set to host world-class exploration campaigns in the coming years. The Guinea plateau deepwater basin, in particular, represented by the “B” blocks on Map 1, hosts well-understood lower Cretaceous source rocks, thick Lower Cretaceous clastics and carbonates, and huge structural closures that the large oil companies cannot ignore. Oil developments in Suriname, and current drilling there on the Demerara Plateau by TotalEnergies, Shell and QE, further support the potential for high-impact exploration from what is the conjugate basin to Bissau.

A very good place to start

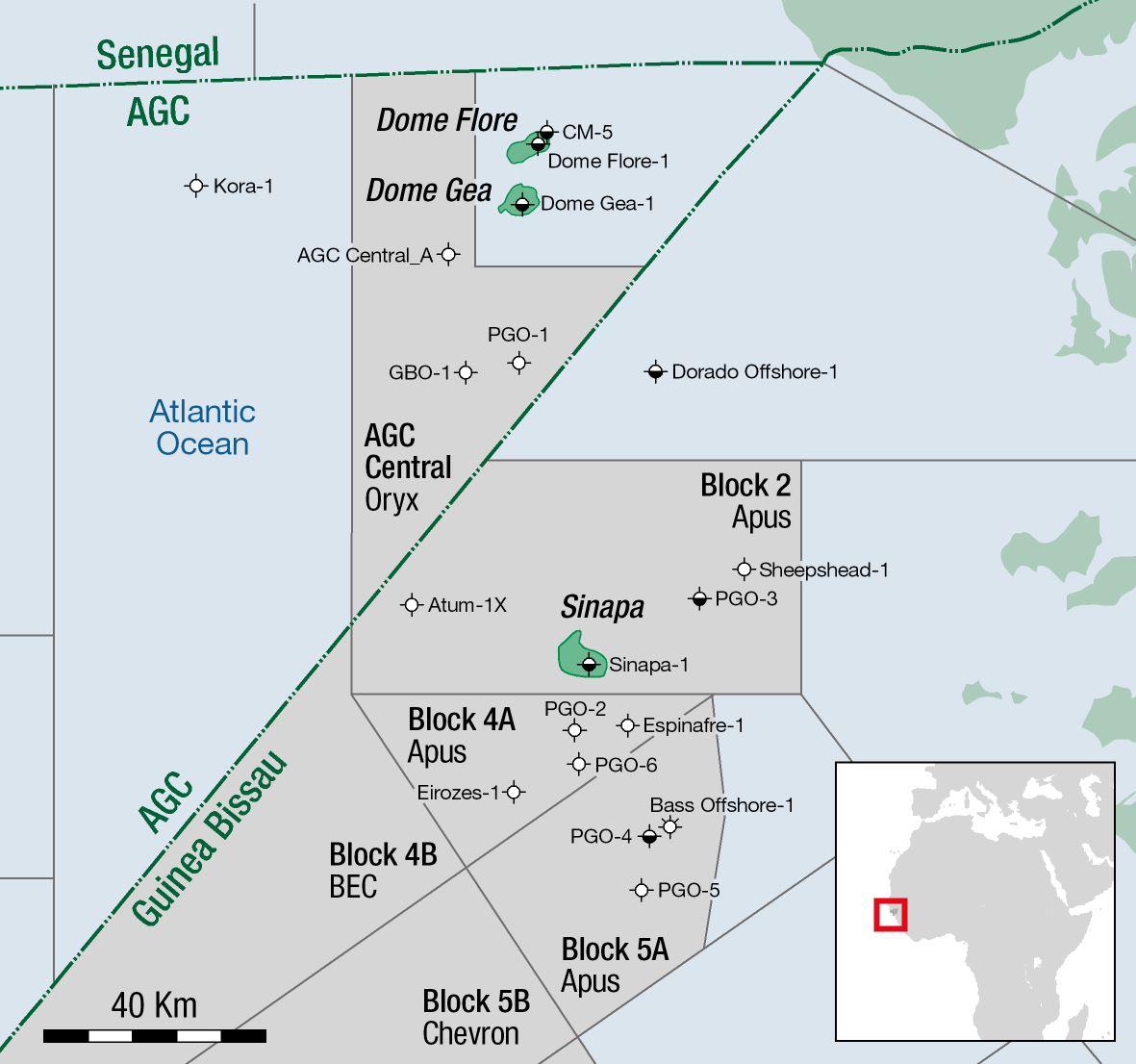

While Phillips was beginning to test the virgin North Sea frontier, and ten years after bp and Shell discovered oil on the Niger Delta, in the 1960s, Esso undertook an ambitious drilling campaign, onshore Guinea-Bissau. The firm drilled four wildcat wells in the onshore Palaeozoic basin based almost entirely on gravity and magnetic surveys and field studies. Reporting shows that in the Silurian and older Palaeozoic formations, the campaign failed to find commercial hydrocarbons. Around the same time (1967 to 71), Total and Copetea did have some success nearby in the shallow waters of what became the AGC, the shared economic zone between Bissau and Senegal. This campaign resulted in the discovery of over a billion barrels of crude at Dome Flore and Dome Gia, almost all of it heavy and bituminous oil in shallow Oligo-Miocene sands. However, one well encountered light oil in deeper Maastrichtian sands.

These early campaigns proved at least two aspects of the petroleum systems in this region: the potential for a petroliferous basin in the early Palaeozoic onshore basins (Bove) and a proven oil province offshore with Cretaceous source rocks and reservoirs. The discovery of oil from the Cenomanian / Turonian (thought to be the source for Dome Flore) is usually the catalyst for a string of prolific oil discoveries, but Guinea-Bissau has not yet cracked that play. The early campaigns were enough to point toward potential in the shallow water offshore, and Texaco subsequently drilled six wells (the PGO wells) across the Ceno-Turonian basin on the Guinea-Bissau shelf between 1968 and 1972. Whilst PGO 4 showed encouraging results for late Cretaceous oil in Albian clastic reservoirs, within a salt basin with many interesting structures, the campaign as a whole again failed to deliver the big bucks.

The formative years

Seismic surveys, drilling shows and nearby heavy oil discoveries at this stage supported a reasonable expectation of a commercial oil and gas province offshore Guinea-Bissau. The jury is still out, as will become clear. Oil sourced from the globally significant CT shales, oil trapped and reservoired in great quantities (albeit biodegraded) nearby, major trapping within a structured allochthonous salt province, and ample evidence for reservoir sands in the Maastrichtian and Albian, surely suggested a string of pearls ready to be exploited. Shell (as Pecten) threw their hat in the ring to test that theory, drilling three wildcat wells in 1990. Dorado, Bass and Sheepshead all provided the same return on investment, good shows, hydrocarbon signs flashing everywhere, but no oil to surface. If the Albian reservoir proved high quality, the charge and trapping appeared to have failed, and vice versa.

After a decade of low activity levels and regional 2D surveys, British indie Premier Oil stepped up to test the potential in this basin in 2001. Using modern 3D and new mapping, they identified a number of promising leads against salt structures (a Triassic salt basin in this region). Premier and partners such as FAR and Oxy drilled 4 prospects plus two sidetracks, at Sinapa, Erizores and Espinafre. Sinapa was the only substantial discovery, with around 13 mmbo recoverable in Albian sands against a salt diapir, but to this day the field remains undeveloped. Sinapa 2 tested the Albian and Aptian sands updip, but found a seal between the main oil charge in the Aptian and the Albian reservoir. This could pave the way for more successful exploration of the Aptian in deepwater along the Guinea Platform edge and into the distal basin centre, where good clastic and carbonate reservoir facies are expected. FAN 2 drilled to the north in Senegal proved up a thick section of Aptian with abundant source and reservoir.

Oxy proved an ambitious partner with Premier in Guinea-Bissau, and carried out a dense 2D seismic survey in deepwater over Blocks 7B and 7C, with a view to drilling a large structure on 2D. The US firm promptly exited before drilling, leaving what is one of the largest undrilled structures in West Africa (currently operated by Supernova Energy). Promising results from the Premier campaign, although sub-commercial, were enough to encourage Svenska to take over the Sinapa blocks, around 2007, which proceeded to work up the existing 3D and acquired new full tensor gravity to improve imaging around the salt. Svenska later acquired additional 3D seismic in the deeper portions of Block 2 and worked the play until around 2020 with new prospects mapped at West Sinapa, and a new play mapped at Atum and Anchova that reflected in geometry at least the platform edge play at SNE in Senegal, later to become the highly successful Sangomar oil field (Woodside Energy). Svenska searched hard for a number of potential partners to drill Atum, including CNOOC at one point, but the firm finally threw in the towel in 2020 as part of a portfolio rationalisation programme, selling their interest to the Norwegian firm Petronor. In the meantime, small independents were cutting their teeth on the deep water blocks in AGC and Bissau, chasing larger structural prospects and the Sangomar-style trend. Rocksource farmed into the deepwater AGC block (Cheval Marin) with Ophir in 2010, on the back of a CSEM survey. The CSEM results strongly supported a hydrocarbon play at Kora, a large, elongated, four-way ridge structure. With Noble Energy picking up the tab in 2011, the group drilled Kora 1, but with disappointing results. The EM anomaly appeared to be associated with carbonate lithologies at the reservoir, although the well only tested the Coniacian. Black Star Petroleum held Block 4B in 2013, as part of a small West Africa portfolio that included the original Namibia Venus Block. Impact Oil bought Black Star in its entirety, leading to a different petroleum exploration story for Impact in Namibia. Bissau Exploration Company (BEC) subsequent took Block 4B on the back of a large 3D survey there. A group of small entrepreneurial exploration companies, including Trace Atlantic and Sphere Petroleum, took acreage around 2010 at Djiffere in Senegal, and Blocks 1 and 5B in Guinea-Bissau. Trace funded a major 3D campaign on Block 5B, contiguous with the large JAAN 3D survey shot by TGS, now being worked up by Chevron. Trace failed to find industry partners to drill on these blocks, despite excellent petroleum geology indications, and exited around 2018. The Trace / Lime / Rex consortium of investors can still be found exploring W Africa in Benin, although they had more success offshore Oman. Supernova Energy, a private Dutch firm, took Block 7B in the 2007/8 licence round. Supernova took all available 2D and shot 3D to work up some major prospects in the middle Aptian, including multi-billion-barrel tilted fault block style leads. Convinced of the major potential here, Supernova went on to secure Block 7C in the extension of the Guinea Promontory.

A common theme in Guinea-Bissau, apart from strong indications of two world-class petroleum systems, is the excellent fiscal regime. The tax/royalty system in Bissau has always ranked near the top in terms of global petroleum economic systems, with high company take and rapid return on investment. A new Petroleum Code in 2014 strengthened these terms further, simplifying the economic model and improving contractor take.

Great Expectations

There is strong support for the conjugate model in the Atlantic, whereby successful petroleum provinces are mirrored on both sides of what was the same basin, pre-rifting. The qualifier is that “conjugate” does not automatically imply “analogue”. This can be seen to be the case in the Lower Cretaceous basins of the MSGBC, compared to the mainly upper Cretaceous Canje play in Guyana. However, with the strong geological connection between the Demerara Plateau in Suriname and the Guinea Plateau in Bissau, there is strong evidence to suggest the lower Cretaceous play has every chance of success. Oil has been recorded in the Aptian sands of the Keskesi 1 well in Suriname for example, and Macaw 1 (TotalEnergies) and Araku Deep 1 (Shell) will test the flanks of the Demerara Plateau late 2025.

In 2023, after another drop in activity offshore Bissau, Apus took the reigns at the Sinapa Blocks (2, 4A and 5A) from Petronor, with a view to picking up the story at Atum and Anchova. These platform edge 3-way closures against the main fault were believed to be closely analogous to the Sangomar field in Senegal. The geometry of both plays are strikingly similar, but charge and reservoir quality appear to have failed when Atum 1 was drilled by Apus in 2024. The important difference between Atum and Sangomar is a change in depositionary fabric around the AGC area, where Sangomar benefits from thick Albian and Cenomanian reservoir sands to the north, and carbonates in the Aptian. The wells south of AGC preserve much thicker Aptian sandstone reservoirs and very little late Cretaceous. There is a strong case for an upper Jurassic carbonate play to the south as well, as the Guinea Plateau develops. Atum 1 notably did not continue to the Aptian targets, and TD’d early in mediocre Albian sands. The deepwater Guinea Plateau Basin hosts a good number of world-class structures with thick Aptian clastic series, a new play that is yet to be tested in anger, and one that US supermajor Chevron is now starting to size up. Chevron took operatorship of Blocks 5B and 6B, adjacent to Supernova in 7B, in September 2025.

Guinea Bissau will host a number of major exploration campaigns over the next few years, with Supernova, Apus, Chevron and BEC all working on modern 3D data and multiple world-class prospects across the Guinea Plateau basin. The recent country entry by Chevron is likely to prove influential in attracting further oil industry investment, and this most recent phase of exploration is set to pay great dividends.