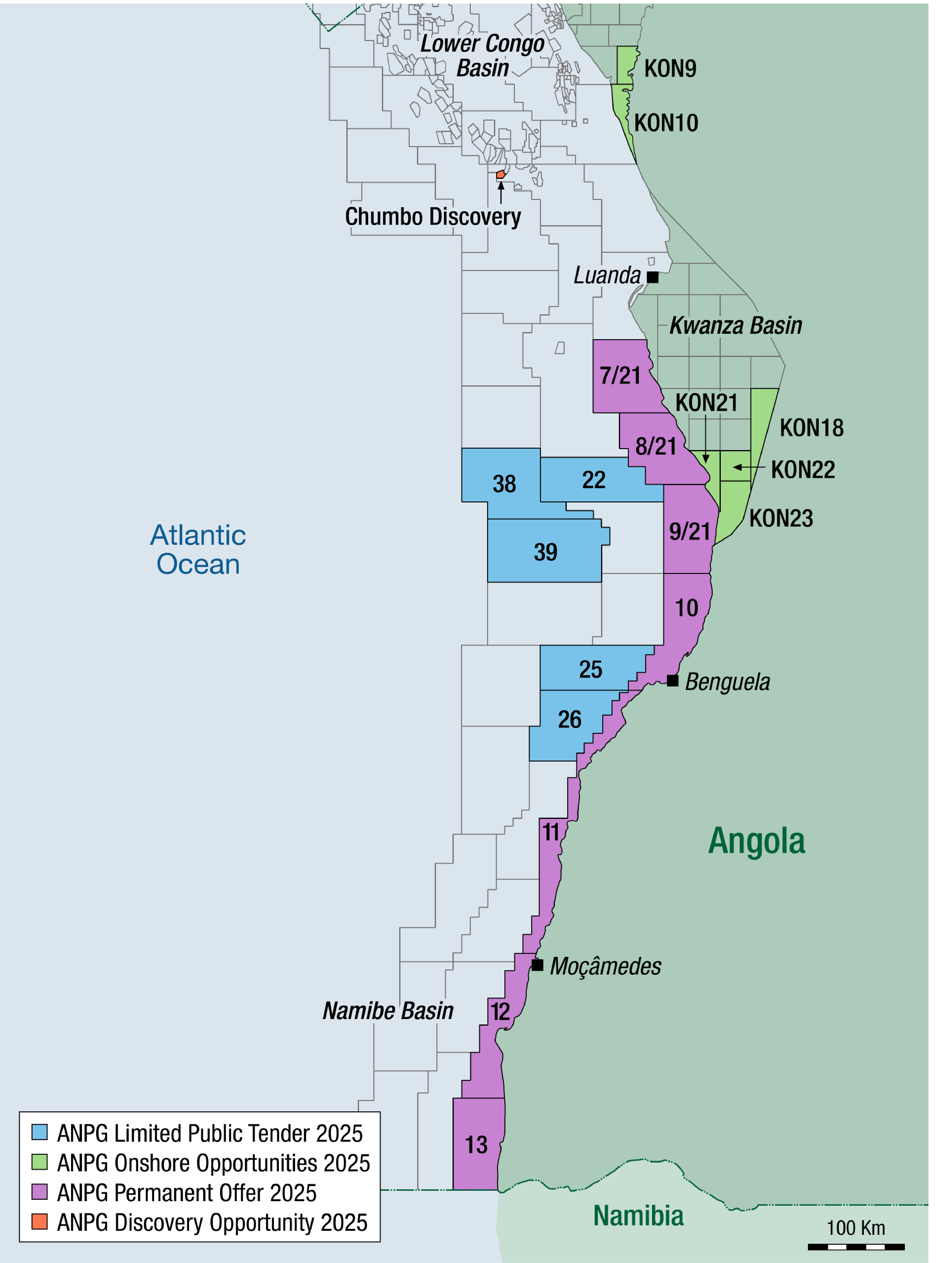

Figure 1: Key exploration deals and block awards in Angola. Source: NVentures.

It’s all in the planning

The stage is being set for a major E&P drive in Angola

Angola is host to a number of recent exploration highlights, driven by a well-organised and energetic energy regulator, ANPG and a strong appetite for low-risk growth in the upstream sector. Wildcat drilling activity remains low for now, but major reforms to licensing strategy are set to ramp up the number of awards, well commitments and seismic surveys. ANPG recently announced 23 licensing opportunities on- and offshore, in four distinct offerings (Figure 2), whilst announcing their ambition to assign 50 new blocks in the coming years.

Three hotspots

Angola recorded its peak production of 1.9 mmbopd in 2008, from the traditional heartlands of the offshore Lower Congo Basin post-salt bonanza of the 1990s. Future production highs can be expected from three further areas of sustained activity: The rush to mature near-field exploration in the Oligo-Miocene deepwater play as the supermajors consider A&D options; the latent potential of the pre-salt mega-play in the Kwanza and Lower Congo basins; and the re-emergence of the exciting pre- and post-salt potential onshore the Lower Congo and Kwanza basins.

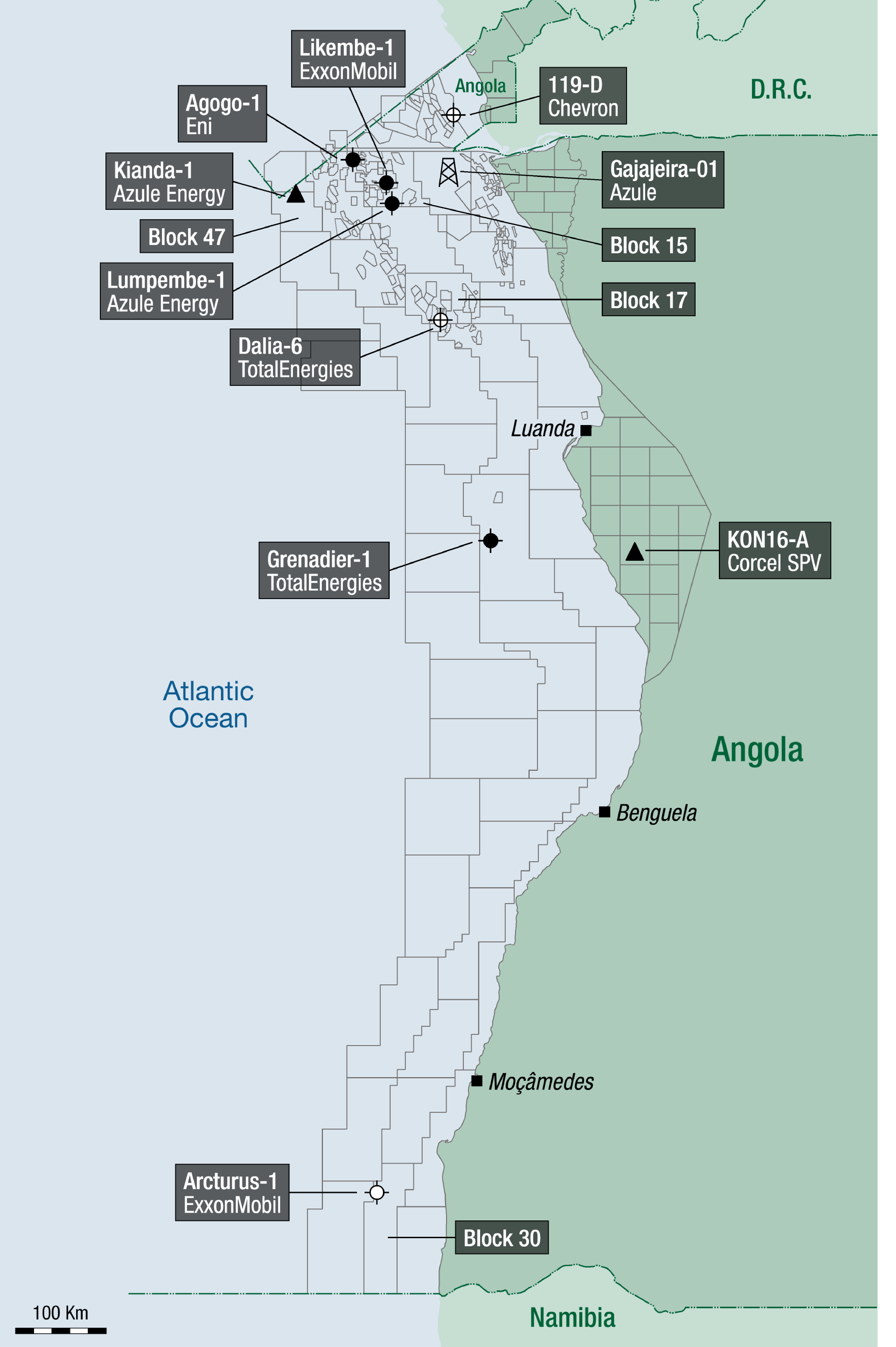

Exploration drilling activity has been reasonably subdued, although often successful in the mature offshore basins (Figure 3). Following on from the major success at Agogo by Eni and partners in Block 15 in 2021 – the discovery is now on production – ExxonMobil and partners have tested the Likembe prospect in Block 15, and Azule drilled Lumpembe in Block 15/06. TotalEnergies re-entered the Block 20 Kwanza play with Grenadier 1 in 2023 (with Petronas), then returned to the hugely successful Dalia play in 2024 with a deep Dalia target (Dalia 6). Further infrastructure-led exploration has paid dividends for Azule in Block 1/14 (with 1 TCF at the Gajajeira 1 discovery) and Chevron in Block 0 (Well 119-D). ExxonMobil carried out a wildcat campaign in the Namibe Basin in the south of the country in Block 30, but to no avail. Independent AIM-listed Corcel attempted a field rejuvenation project at Tobias 13 in 2023, onshore Block Kon 11, and while that was not hugely successful, it does begin the story of what is likely to become a major series of exploration drilling campaigns onshore Angola in the next few years.

Lots of activity

ANPG held a bid round for a number of blocks in 2023, including the onshore. Early results suggested a successful round, and some of those awards still stand. Afentra took Blocks Kon 15 (with Acrep ) and Kon 19 (Sonangol), while Etu Energias (previously Somoil) were awarded Con 2 and 8 in the onshore Lower Congo Basin, usually partnered with Effimax and Simples Oil, although the firm now appears to have interests only in Con 1 and Con 6. Likewise, early awards of Kon 13 (Serinus) and Con 7 ( Enagol) appear to have fallen away, and Canadian junior MTI Energy no longer appear to be active, having taken interests in four onshore blocks in 2021.

More recent activity onshore has proven more permanent (Figure 1), with Corcel strengthening its position in the Kwanza Basin, and the likes of Afentra, Walcot and Oando taking major onshore positions. Corcel now hold interests in Kon 11, 12 and 16, with a major new exploration well planned for Kon 16 in the coming months. Sintana have taken a stake in that campaign, extending its impressive exploration reach in southwest Africa to new, exciting plays. Early 2025 saw Oando (the major Nigerian independent) take a stake in Kon 13, to be joined there by Walcot. Walcot themselves are investing in blocks Con 3 and 7. Afentra will add to its onshore portfolio with an RSC for block Kon 4. Negotiations for these latter awards (Figure 1) are still underway (July 2025). In the far south of the country, two large reconnaissance licences have been award in the Etosha – Okavango districts, to ReconAfrica and to Xuan Thien Group.

Offshore, a number of awards have been completed, including Blocks 49 and 50 for Chevron. Azule plan a major ultra-deepwater wildcat at Kianda 1 in Block 47 in the near future, with Equinor and Sonangol. Block 6/24 was awarded to Sonangol EP and the Australian RedSky Energy (35 %) and Acrep (15 %) in 2024. Afentra, meanwhile, has been busy strengthening its equity position in Blocks 3/05 and 3/05A, a major production hub for them, buying Etu Energies’ piece in 2025.

Ahead of the curve

Angola is ahead of the curve when it comes to attracting fresh upstream investment in new and existing basins, coinciding with what looks like a nascent hydrocarbon renaissance globally. ANPG are working on various strategies to expedite these goals, with greater transparency and access in what was seen as a “supermajor’s playground”, world-class data management and promotion, and strong communications for planned acreage offerings. Whilst the main fiscal regime mechanisms remain the same, based on Production Sharing Contracts, fiscal incentives have been provided to firms extending production in well-established Lower Congo Basin core hubs. For example, TotalEnergies and partners have won an extension and improved terms on Block 17, the prolific Girasol/Dalia hub, with the licence now up for renewal in 2045. TotalEnergies expects to recover an extra 300 mmboe from the new deal. Likewise, Block 15 has been extended out to 2037 for the ExxonMobil operating group, again with fiscal incentives to extend production and encourage ILX. Block 15 is home to 4 active FPSOs, including the Kizomba hub.

New acreage opportunities are now defined by ANPG in their current promotional campaign (Figure 1). The regulator is offering 23 blocks as follows; 7 shallow to deepwater blocks in the Kwanza (7/21, 8/21 and 9/21) and Benguela (10, 11 and 12) and Namibe (Blok 13) basins under a Permanent Offer regime; five deepwater offshore exploration blocks in the Kwanza (22, 38 and 29) and Benguela (25 and 26) Basins are offered under the 2025 Limited Public Tender scheme; 10 onshore Blocks are being promoted, six open (Con 9 and 10 and Kon 18, 21, 22 and 23) and 4 as part of what appears to be a farm-out process (Con 5 and Kon 5, 17 and 20). Finally, the Chumbo field offshore is available as an “Opportunity with Discovery” asset divestment in the Block 18 area (32.5 mmbo contingent resources).

Angola continues to be a powerhouse of production and exploration in West Africa, and clearly intends to remain competitive in the global E&P race for new barrels. The country benefits from a strong industry regulator, decades of production experience, and great geology. The prolific Lower Congo Basin continues to deliver, and there is great potential in the revitalised onshore salt basins, while further upside is yet to be revealed in the deepwater pre-salt. The Namibe Basin is yet to show its hand, with only two wells to date, either side of the border.