The global energy landscape is undergoing profound transformation, shaped by shifting market dynamics, technological advancements, and the accelerating need for sustainable energy solutions. Photography: Getty Images.

The E&P industry of the future

The global energy landscape is undergoing profound transformation, shaped by shifting market dynamics, technological advancements, and the accelerating need for sustainable energy solutions. The Exploration & Production (E&P) sector stands at the forefront of this evolution, navigating the complex interplay between operational efficiency, resource optimization, and the broader energy transition. This brief, produced by S&P Global Commodity Insights in collaboration with the European Association of Geoscientists and Engineers (EAGE), explores the immediate opportunities in 2025 and the long-term transformations that will define the industry over the next five to ten years.

An industry in transition or transformation?

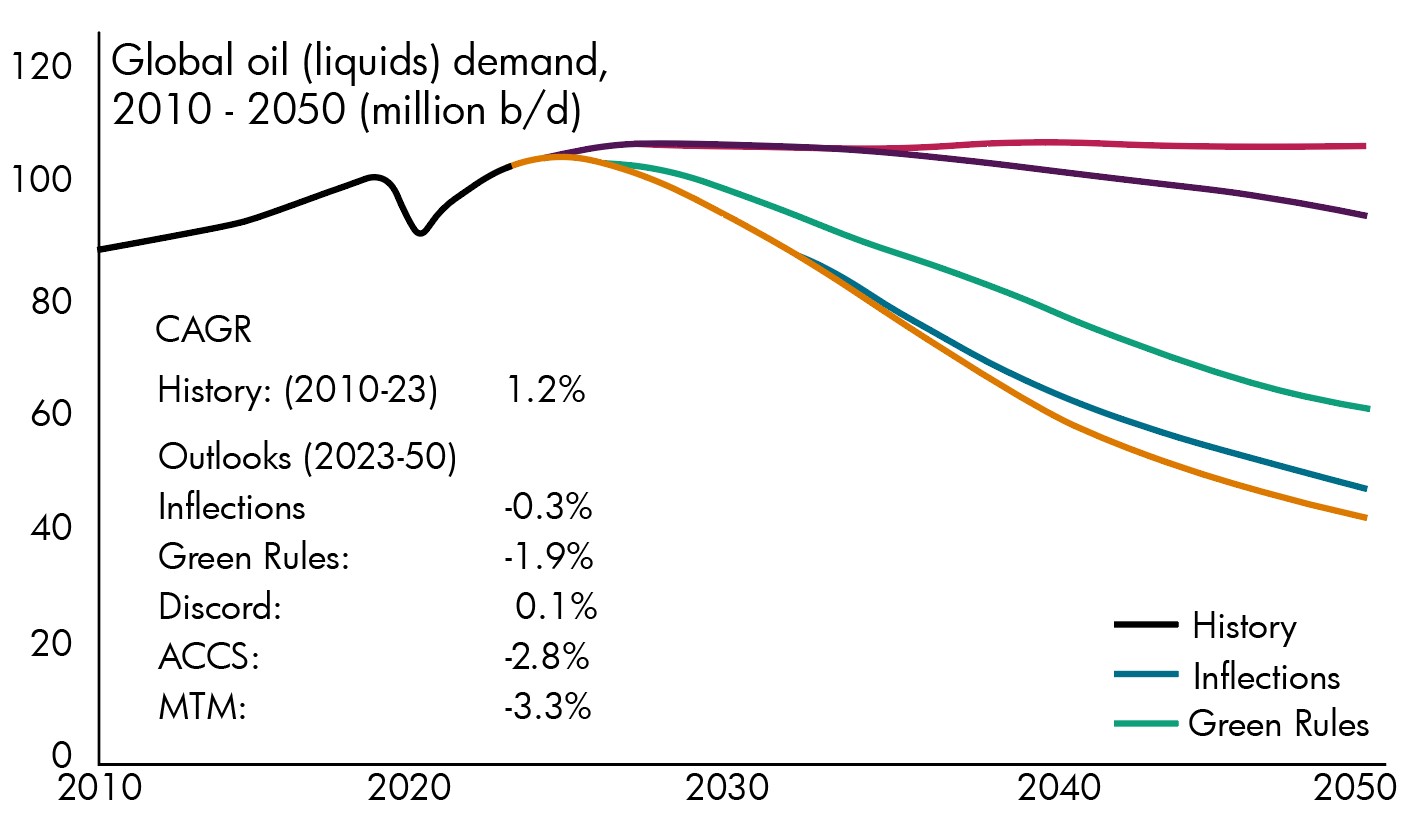

The upstream E&P sector has faced challenges over the last decade, including a downturn, the energy transition, and COVID-19. The industry is resilient but must address questions about its future shape and size as it considers factors such as expected continued demand beyond 2050, workforce demographics and capabilities by 2035, and the role of technology in achieving returns on investments. Figure 1 shows the S&P Global Energy Scenarios liquids demand up to 2050, highlighting the “Inflections” scenario with peak demand around 2029 followed by a gentle decline.

Global geoscience outlook for 2025: Setting the stage for years to come

The energy industry is shifting in how it works, manages data, and makes operational decisions. Key themes for 2025 include emerging technologies, sustainability, decarbonization, evolving workforce skillsets, and global challenges in the geopolitical landscape. Opportunities will center around new job roles in Carbon Capture and Storage (CCS), Geothermal, and Digital Transformation within the E&P sector. Several factors will influence how this landscape evolves in 2025:

- The continued drive to harness the potential of data-driven decision-making, including the testing and scaling of autonomous systems already in development

- Evolution of the geoscience workforce as the sector adapts to career development and skills evolution in order to create business advantage through technologies such as AI

- Maximizing recovery through relentless focus on excellence in reservoir optimisation

- Continued innovation in subsurface data (e.g. seismic) and technologies

AI, automation, and digitalization are transforming the E&P industry. It is being tested and applied in many workflows, from strategic settings such as portfolio management through to technical applications such as predictive analytics, seismic interpretation, reservoir modelling, and production optimization. Over the next five years, AI-driven geoscience models will improve subsurface imaging, reduce exploration risks, and enhance resource identification. AI-powered automation will optimize drilling parameters, and AI will play a crucial role in emissions monitoring and carbon capture initiatives.

Exploration drilling and resource discovery potentially hit record lows in 2024, and whilst an uptick is possible in 2025, there is a real risk that secure, diverse production at the required levels might be difficult by the late 2030s. This is a combination of stranded resources (transition regulation, cost, GHG intensity) and low discovery rates allied with reducing returns from established technical reserves replacement approaches such as enhanced oil recovery or infrastructure-led exploration. If the industry accepts that exploration is needed to add material reserves back into market, then it might struggle to do so through highly mature basins, meaning that risks associated with finding new reserves increase. The jury is still out on the return of exploration, but it is becoming increasingly apparent that new strategies and approaches are needed.

This is a sector and workforce that continues to innovate and evolve commercially and technically against a backdrop of reduced budgets for exploration, increased regulation, a push to shorten times (e.g. the typical 8-10 years of an offshore cycle from licensing to production) against an uncertain monetization pathway and continued M&A activity. It’s fine to ask or encourage geoscience to evolve faster but good leadership is needed to really enable this.

Explore Expert Resources on Today’s Most Pressing E&P Topics

E&P workforce of the future: The dilemma

The demand for hydrocarbons will continue, requiring skilled professionals to find and produce resources. The industry faces challenges in attracting new talent due to declining enrolments in petroleum engineering programs and societal pressure against working in the industry. Retaining existing staff, ensuring they are up to speed with new technology, and attracting bright new staff with new skills and capabilities are essential steps. Where will these staff come from? There seems to be convergence in key areas:

- Providing routes into industry without pure geoscience degrees

- Recruiting from regions that have increased their geoscience academic offerings and working with those institutions to help them deliver the best courses possible

- Building bigger teams local to resources where education can be supported and there are additional benefits such as meeting local content requirements

- Understanding the demographics of teams a decade from now and maximising knowledge retention in E&P organisations through both technology and people before the opportunity is lost

E&P technology innovation

Technological innovations have significantly impacted the E&P industry, focusing on enhancing efficiency and developing new capabilities. Recent improvements include seismic acquisition, wellbore, and reservoir technologies. Digital transformation has also led to advancements in exploration and production workflows, data retrieval and processing, and increased innovation cycles.

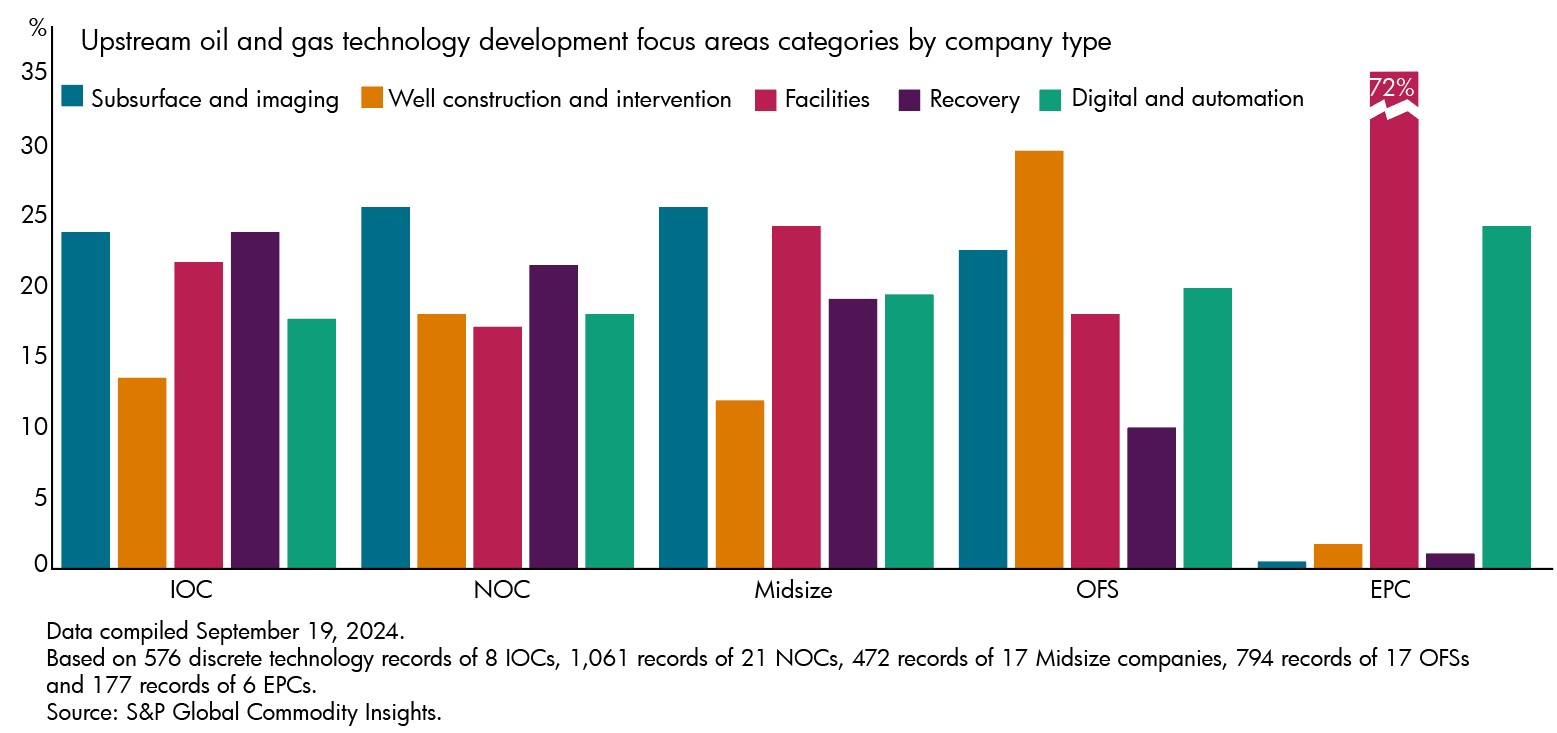

Different types of companies across the Upstream space vary on their technology development strategies. Figure 2 shows OFS companies have shifted focus to wells and subsurface, while IOC operators align strategy with development, and NOCs emphasize subsurface and enhanced recovery. Digitalization and automation remain consistent priorities across the industry.

The exploration and production (E&P) industry is undergoing a profound transformation, driven by advancements in artificial intelligence (AI), automation, and digitalization. Technology innovation and areas of investment will rapidly change with the next few years being pivotal in defining areas of rapid AI development and adoption. As operators and service companies strive to enhance efficiency, optimize reservoir management, and reduce operational costs, AI is increasingly becoming a core enabler of technological evolution in this space.

Energy diversification for a profitable energy transition

Energy companies are diversifying their portfolios beyond traditional oil and gas as part of broader energy transition strategies. This includes investments in CCS technology, renewable energy, and green hydrogen. The outlook for carbon sequestration projects is optimistic, with significant growth expected in regional hubs like the Gulf Coast, Permian Basin, and Midwest. These hubs are being scrutinized to see if they really work and can be replicated elsewhere in the world. Renewable energy investments are also robust, with North America, Europe, and Asia-Pacific leading the transition to a low-carbon energy system.

Summary

The E&P industry is at a pivotal moment, navigating the complexities of the energy transition while striving for operational efficiency and sustainability. This brief highlights the key trends, challenges, and strategic imperatives that will shape the future of energy. As we look ahead to 2025 and beyond, it is crucial for industry professionals to embrace innovation, digitalization, and collaboration to drive the evolution of E&P in a changing world.

Copyright © 2025 S&P Global Commodity Insights. All rights reserved.

S&P Global, the S&P Global logo, S&P Global Commodity Insights, and Platts are trademarks of S&P Global Inc. Permission for any commercial use of these trademarks must be obtained in writing from S&P Global Inc. You may view or otherwise use the information, prices, indices, assessments and other related information, graphs, tables and images (“Data”) in this publication only for your personal use or, if you or your company has a license for the Data from S&P Global Commodity Insights and you are an authorized user, for your company’s internal business use only. You may not publish, reproduce, extract, distribute, retransmit, resell, create any derivative work from and/or otherwise provide access to the Data or any portion thereof to any person (either within or outside your company, including as part of or via any internal electronic system or intranet), firm or entity, including any subsidiary, parent, or other entity that is affiliated with your company, without S&P Global Commodity Insights’ prior written consent or as otherwise authorized under license from S&P Global Commodity Insights. Any use or distribution of the Data beyond the express uses authorized in this paragraph above is subject to the payment of additional fees to S&P Global Commodity Insights. S&P Global Commodity Insights, its affiliates and all of their third-party licensors disclaim any and all warranties, express or implied, including, but not limited to, any warranties of merchantability or fitness for a particular purpose or use as to the Data, or the results obtained by its use or as to the performance thereof. Data in this publication includes independent and verifiable data collected from actual market participants. Any user of the Data should not rely on any information and/or assessment contained therein in making any investment, trading, risk management or other decision. S&P Global Commodity Insights, its affiliates and their third-party licensors do not guarantee the adequacy, accuracy, timeliness and/or completeness of the Data or any component thereof or any communications (whether written, oral, electronic or in other format), and shall not be subject to any damages or liability, including but not limited to any indirect, special, incidental, punitive or consequential damages (including but not limited to, loss of profits, trading losses and loss of goodwill). ICE index data and NYMEX futures data used herein are provided under S&P Global Commodity Insights’ commercial licensing agreements with ICE and with NYMEX. You acknowledge that the ICE index data and NYMEX futures data herein are confidential and are proprietary trade secrets and data of ICE and NYMEX or its licensors/suppliers, and you shall use best efforts to prevent the unauthorized publication, disclosure or copying of the ICE index data and/or NYMEX futures data. Permission is granted for those registered with the Copyright Clearance Center (CCC) to copy material herein for internal reference or personal use only, provided that appropriate payment is made to the CCC, 222 Rosewood Drive, Danvers, MA 01923, phone +1-978-750-8400. Reproduction in any other form, or for any other purpose, is forbidden without the express prior permission of S&P Global Inc. For article reprints, contact: The YGS Group, phone +1-717-505-9701 x105 (800-501-9571 from the U.S.). For all other queries or requests pursuant to this notice, please contact S&P Global Inc. via email at ci.support@spglobal.com.