UAE – Looking Outward

A cautious road to international participation in upstream exploration in the UAE, with hydrogen in hot pursuit.

The Middle East is not a region associated with open international participation, since the nationalisation of resources in the 1970s, but strong trends are emerging to counter this isolationist policy. Since 2018, Sharjah, Ras Al Khaimah and Abu Dhabi have welcomed international bids on competitive licensing rounds, albeit in a selective manner designed to attract strategic partners and reward existing investors.

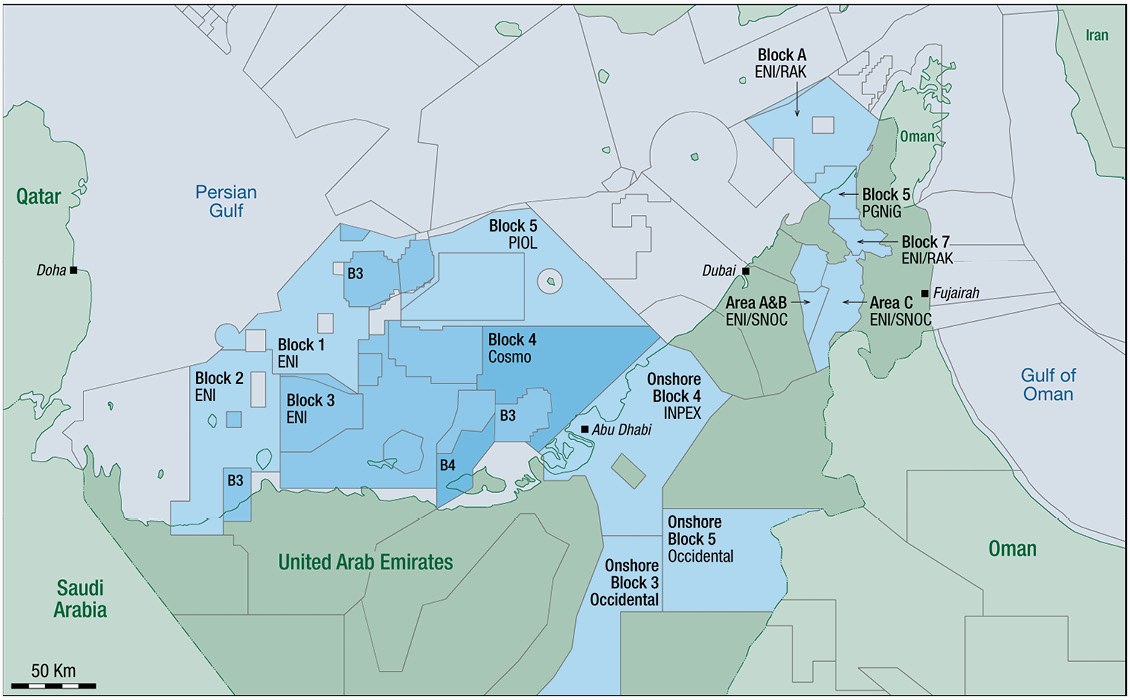

Eni in particular has played a dominant role across the Emirates, taking three blocks in Abu Dhabi, two in Sharjah and two in Ras Al Khaimah in the last two years, with companies from Japan and most recently Pakistan, participating. Meanwhile hydrogen and ammonia, its energy transport medium, is beginning to grab the limelight, as Abu Dhabi in particular builds major infrastructure for blue ammonia, with cargoes being sold to Japan in August 2021.

Abu Dhabi announced its very first Bid Round in 2018, with blocks outside the main producing areas. In support of this and further licensing in 2019, the state national oil company ADNOC, kicked off the world’s largest contiguous 2D and 3D seismic survey to cover all underexplored areas. In January 2019 Eni and partner PTTEP were awarded Blocks 1 and 2 offshore, while INPEX took Block 4 straddling the coast. Occidental acquired onshore Block 3.

In opening investment to competitive bidding, ADNOC called for major E&P investment, a nine-year term for exploration, with a further 35 years for production, and an optional back-in for ADNOC of up to 60% on all production leases granted as a result. Eni committed US$230 million for the two offshore blocks and INPEX bid US$176 million. An Indian consortium took Block 1 onshore (Indian Oil Ltd and BPRL).

Before this first open Bid Round, ADNOC had sold small stakes in the main producing assets of the Lower Zakum and Umm Shaif projects to the likes of Eni, INPEX and CNOOC.

ADNOC announced a second Bid Round in May 2019. Whilst international interest was high, the award process was clearly based on firm criteria including strategic economic considerations (such as long-term offtake contracts with Japan and Asia) and long-term investment in existing projects in the Emirate. Terms remained similar with nine years for exploration, 35 years for exploitation and a possible 60% state back-in, along with signature bonuses and work programme commitments.

Occidental returned to win Block 5 onshore, adjacent to their existing block (bidding US$140 million). Cosmo, a Japanese consortium, already actively investing in the Mubarraz field offshore (as ADOC), were awarded offshore Block 4. US$145 million was bid, including signature bonus.

Block 3 offshore was awarded to the Eni / PTTEP consortium, adjacent to their First Round Blocks 1 and 2. Most recently in August 2021, a Pakistan consortium made up of OGDCL, Mari Petroleum, GHPL and PPL (25% each) were awarded the large offshore Block 5 concession. Block 5, with a US$305 million price tag, will be operated by Pakistan International Oil Limited (PIOL).

Interestingly ADNOC state they will not continue to offer Block 2 Onshore as part of the second round. The state firm announced a huge unconventional ‘find’ there in 2020, with volumes of 22 Bbo and 160 Tcf quoted at the time. ADNOC refer to the potential for licensing this to unconventional resource companies (Total was awarded 40% in a similar unconventional block, Ruwais Diyab, in 2018).

As a fascinating parallel to this surge in activity and investment in conventional and unconventional oil, Abu Dhabi is focusing heavily on hydrogen, ammonia, carbon capture utilisation and storge (CCUS) and renewables. Eni again is heavily involved, signing a memorandum of understanding (MoU) in September 2021 with Mubadala for hydrogen and ammonia joint ventures in the Emirate; the Italian firm already holds 20% in ADNOC Refining.

In 2021 alone, ADNOC has completed several agreements with international firms to push hydrogen and ammonia to the front of the energy agenda. In January, Japan and Abu Dhabi agreed headline terms to jointly develop ammonia and CCUS technology. In March, the Korean firm GS Energy invested in ammonia projects, whilst Petronas signed a broad MoU on upstream, downstream and ammonia investments. In April, the government of India signed a similar MoU for hydrogen and ammonia, whilst in May, ADNOC itself announced major plans for the production of Blue Ammonia (using blue hydrogen produced with CCUS) at its Fertil plant in the Ruwais Industrial Complex.

In June, Fertiglobe announced it will join ADNOC and ADQ as a partner in a new, large-scale, 1 million tonnes per annum, blue ammonia project at TA’ZIZ industrial services zone in Ruwais. In July, companies from Japan (INPEX, JERA and JOGMEC) all agreed investments in hydrogen and renewables. Most recently ADNOC have announced first cargoes of blue hydrogen to Itochu, Idemitsu and INPEX.

Whilst oil and gas will continue to provide wealth and growth opportunities for the Emirates, for exports (and foreign currency reserves), domestic use and petrochemicals, there is a new kid on the block, with demand for hydrogen and ammonia already generating long-term revenues from major infrastructure projects. This is the reality of the energy transition in practice; the progress of hydrogen and ammonia will create conditions for low and net zero carbon energy, whilst oil, gas and petrochem will dominate global economic and industrial productivity for years to come.

This exploration Hot Spot is brought to you in association with NVentures Ltd.

This exploration Hot Spot is brought to you in association with NVentures Ltd.