Bangladesh Upstream: Delayed but Not Out

Bangladesh is geologically well positioned to pursue a strategy fuelled by natural gas, but the international Covid situation is causing continued delays; namely to the 2020 licensing round. This Hot Spot is brought to you in association with NVentures.

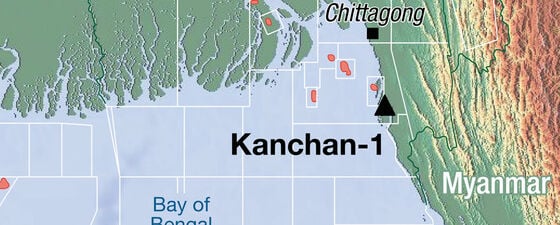

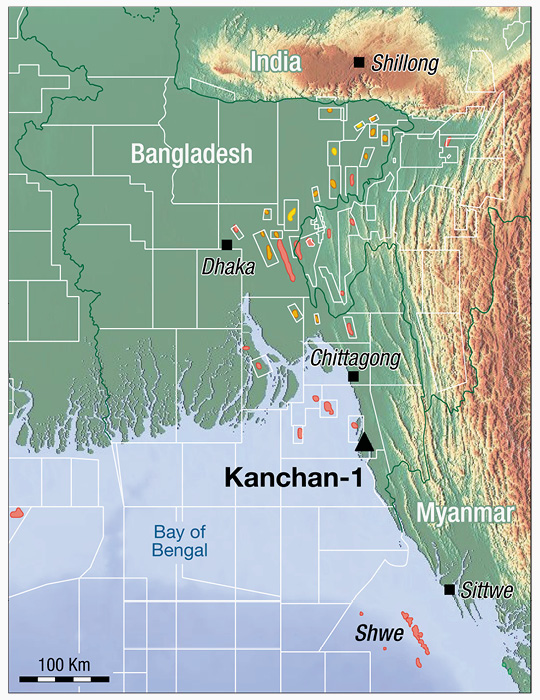

The further open-ended delay to Bangladesh’s 2020 licensing round, anticipated to have been announced in September 2020, should not come as a surprise given the international Covid situation and low oil price, though it may be a disappointment for a country whose exploration acreage map looks in need of a makeover. However, the expected end 2020 spud of an exploration well, ONGC Videsh Ltd (OVL)’s Kanchan-1 in the south-east of the country (Block SS-04, onshore), may serve as a boost to reinvigorate interest in a country in which gas demand has recently outstripped supply and which, despite some renewable initiatives such as wind, has committed itself to a medium-term energy policy dependent on natural gas.

Map showing location of the OVL’s Kanchan-1 well, onshore Bangladesh.

Well Positioned for Gas

Bangladesh is geologically well positioned to pursue a strategy fuelled by natural gas, with numerous producing gas fields onshore and, formerly, offshore, all sourced and trapped within the massive Neogene fluvio-deltaic system of the Bengal Fan, a product of, and in places a part of, the lengthy Himalayan collision. To the east of the country, fields are expressed as compressional surface anticlines in the Tripura-Cachar fold belt, a north-west to south-east trending curvilinear mountain range extending eastward into India and Myanmar. The main risks with these anticlinal structures are seal breach, and drilling challenges due to overpressure caused by the massive vertical relief on the structures, as well as risk of low saturation ‘fizz gas’, in part due to the overpressure.

Further west the structures become less pronounced and stratigraphic or combination traps are more common. These can be difficult to identify, given the excessive level of canyon cutting in the deltaic sediments. The canyons tend to be mud filled, resulting in an atypical stratigraphic play in which a muddy canyon seals a remnant sand. Seal is again high risk in this setting.

The orientation of the folds and the slightly offset orientation of the modern Ganges Brahmaputra drainage system further complicates exploration operations. The superimposition of a standard north–south aligned exploration licensing grid adds to the numerous challenges in acquiring complete high quality seismic datasets. Technical challenges such as tidal statics and feathering of streamers in the tidal channels exacerbate the problem. Seafloor acquisition and transition zone (TZ) technology is required.

Fortuitous Delay?

Perhaps due to these challenges, the IOCs active in the country in the 1990s and 2000s, including Shell, Cairn, Tullow and Santos, have all abandoned exploration, transferring operatorship of the discovered producing fields to smaller players such as KrisEnergy. While this is a reasonable field life-cycle strategy, exploration is now largely in the hands of a few regional NOCs such as Gazprom, OVL and local state-owned BAPEX, and it is important to note that the earlier international players all left before geophysical acquisition advances became practical, cost-effective, solutions. On that basis it is expected there is a lot more to find. Further along the same trend, for example, the Shwe field offshore Myanmar has numerous similarities with the Bengal Fan combination traps, and now benefits from modern 3D and AVO work (though it too was discovered on 2D data).

OVL’s onshore prospect, along trend from Cairn’s 2008 well Magnama-1 (gas shows), is reported to benefit from modern TZ data in and around the Moheshkhali (Maiskali) island and estuary. This will be critical in defining trap and enabling AVO techniques to highlight hydrocarbon responses, though gas saturation and overpressure could still be risks.

If the Bangladesh authorities review the historically low price paid for domestic gas and the restrictions on the international market, and Kanchan-1 is a discovery, the delay of the licensing round could end up to have been fortuitously timed to attract a renewed interest by international players and acquisition contractors, while avoiding direct competition in terms of timing with currently active bid rounds in neighbouring India and Pakistan.