Markets Behaving Differently

The Middle East – one of the most stable E&P markets

The Middle East is the largest producing area within the E&P industry, with a total production of around 41 MMboepd in 2015, while Western Europe is the largest offshore market in terms of spending. These markets are expected to behave differently during the current downwards cycle. The Middle East is the largest producing region in terms of liquids and the third largest in terms of gas, where current production is 28.6 MMbpd and 55 Bcfpd, respectively. Liquid production is expected to grow by 0.8 MMbopd in 2015. This production growth is mainly derived from the redevelopment of old fields in Iraq and the growth of mature fields in Saudi Arabia.

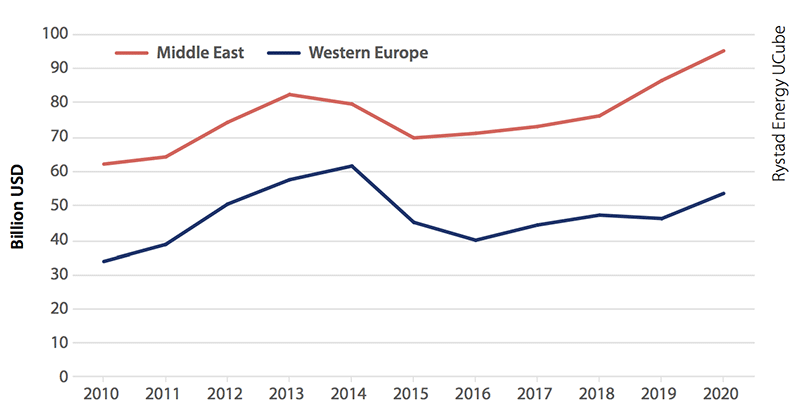

Upstream investments (excluding exploration) for Middle East and Western Europe.Until 2020 the Middle East is expected to continue to grow at an average pace of around 0.5 MMbopd per year, with Iran as another key driver. The lifting of sanctions against Iran will probably result in the return of international oil companies, where the focus will be on redeveloping mature, oil-producing fields. In terms of investments, the Middle East has been relatively resistant to lower oil prices. Total investments in 2015 are expected to be down by 13% compared to 2014, compared to a global average of 23%. One interesting observation is that despite the drop in oil prices Saudi Arabia’s rig count is up 25% in 2015 when compared to 2014.

Upstream investments (excluding exploration) for Middle East and Western Europe.Until 2020 the Middle East is expected to continue to grow at an average pace of around 0.5 MMbopd per year, with Iran as another key driver. The lifting of sanctions against Iran will probably result in the return of international oil companies, where the focus will be on redeveloping mature, oil-producing fields. In terms of investments, the Middle East has been relatively resistant to lower oil prices. Total investments in 2015 are expected to be down by 13% compared to 2014, compared to a global average of 23%. One interesting observation is that despite the drop in oil prices Saudi Arabia’s rig count is up 25% in 2015 when compared to 2014.

Different Reactions

Western Europe cannot compete with the Middle East when it comes to production. The region is expected to produce 3.6 MMbpd of liquids and 23 Bcfpd of gas in 2015. For 2015, the liquid production is estimated to increase by 150 Mbpd, but for the rest of the decade it is believed that production will be flat. On the activity side, total investments will fall by around 30%. There are several reasons for this decline, but some key explanations include completion of development projects, lower unit prices and fewer maintenance investments.

The development and reaction of the Middle East and Western Europe to low prices are quite different. Middle Eastern activity levels have been robust and production is projected to increase, whilst in Western European production is expected to remain flat going forward. One of the key reasons for the resilience of the Middle East, even in a low oil price environment, is the number of large mature fields with high potential at a relatively low cost.