Iran. The Implications of Peace

An agreement on Iran’s nuclear industry should be signed by the end of June. What are the implications for the oil price, OPEC and the industry?

It seems that the UN Security Council, plus Germany, has finally come to an agreement with Iran on curbing the country’s uranium enrichment programme, and a reciprocal lifting of sanctions. The deal is expected to be fleshed out and signed by the end of June (2015), and although there is much playing to hostile audiences – Iran’s hardliners as well as Israel, Saudi Arabia and US senate Republicans – there appears to be a steely determination on both sides.

Widespread Implications

There are, inevitably, enormous implications for oil and gas prices, for OPEC and for the industry. Iran has the fourth largest oil reserves in the world and the second largest gas. Approximately 70% of the Republic’s oil is onshore and most of the remainder is in the Persian Gulf. Iran also holds largely undeveloped reserves in the Caspian. The country’s gas potential is enormous with many recent discoveries, as well as the 51 Tcfg reserve known as South Pars.

A significant increase in oil and gas supply will – bar any unforeseen supply disruptions – depress the already low world price. Iran’s oil production ran at around 4 MMbopd for much of the first decade of the millennium, but plummeted after new sanctions were imposed in 2011. The current output of liquids is 2.8 MMbopd, of which only 1.1 MMbo is exported.

Barrels of oil near Isfahan, Iran. (Source: Teimoury/Dreamstime.com)

Once compliance with international inspections is ascertained – and there are differing views on how long this will take – Iran could not only begin to increase production by a possible 500,000 barrels in six months and 700,000 within a year, but could immediately begin to release some of the 30 MMbo it is believed to have stored onshore and in tankers.

Iran’s aim is not only to achieve the pre-sanctions production level of 4 MMbopd but to reach 5.7 MMbopd by 2018, although this will take billions of dollars of investment. Some analysts estimate that $230bn is required across the energy sector.

Many western companies are poised to jump in. Shell, Repsol, Statoil and Total were all forced to pull out in 2010 but there are now reports of new contracts being drawn up, with Eni and Total believed to be among the frontrunners. Whether companies will get the production sharing agreements they want with the National Iranian Oil Company remains unclear, but at the very least they will be hoping for a flexible fee structure that will allow them to book large reserves.

Increased Supply

It seems likely, therefore, that within the lifetime of the current US shale boom significantly more oil supply will arrive on the market, depressing prices further. Some analysts are speculating that Brent could drop as low as $20/b. However, as the IEA points out, this may be partially balanced by cuts in more expensive production elsewhere.

A secondary, price-deflating effect of the agreement will be the calming of speculation over the security of the Straits of Hormuz. At its narrowest, this ‘pinch point’ is just 34 km wide, but it is the outlet for 20% of the world’s crude. Over the last few years, fears of Iranian disruption have frequently helped inflate prices.

Gas prices will also be lowered, not only because most contracts are oil-linked, but also because of greater supply. In 2012 Iran produced 5.6 Tcf, although currently only 21 Bcfgpd comes from South Pars, the enormous field that is shared with Qatar (where it is known as North Dome). It is believed to hold 40% of Iran’s reserves and it is the Republic’s stated priority for investment. Under sanctions, Iranian companies have been implementing a 24-stage development plan at South Pars but this is only half complete. In addition, there have been several new gas discoveries in recent years and these await development. Iran’s overall goal is 35.3 Bcfgpd by 2018.

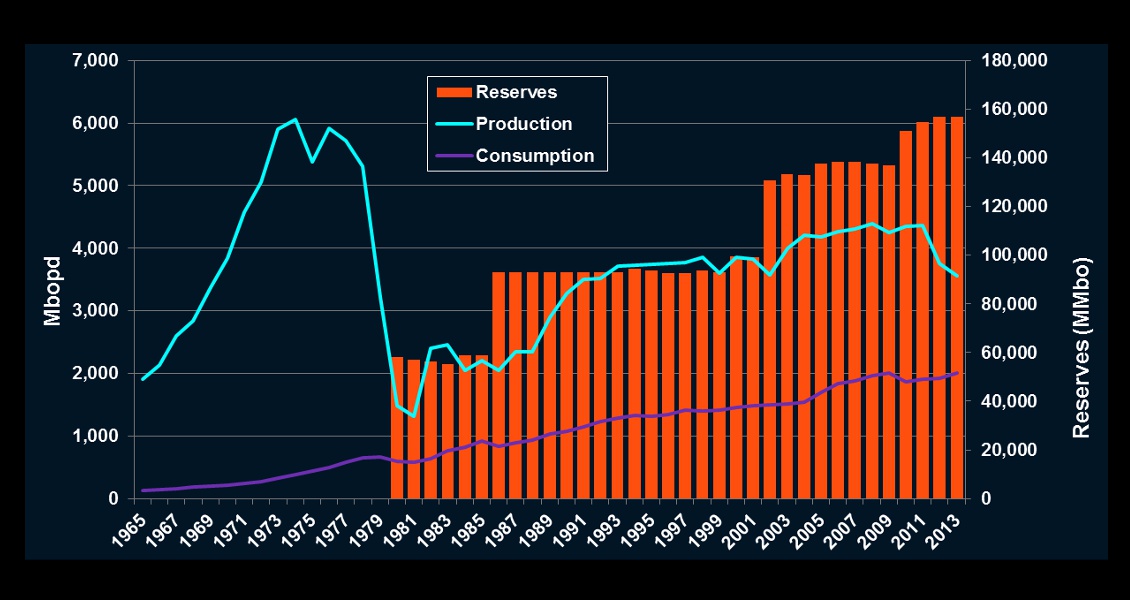

Iran’s oil reserves, production and consumption. (BP Statistical Review of World Energy 2014)

Political Commitment

President Rouhani’s commitment to reintegration with the wider world seems genuine and personal. Getting sanctions lifted was his main pledge in the 2013 election which he won with widespread, popular support. After years of corruption under President Ahmadinajad, fuelled by sanctions and attempts to circumvent them, the treasury was empty when Rouhani came to power. The country was suffering 40% inflation and almost 25% youth unemployment. In the last two years it has faced severe fuel shortages and the decimation of the agricultural sector through drought. The World Bank has estimated that a third of Iran will be empty within 20 years because of water shortages.

The Supreme Leader, Ayatollah Ali Khamenei, seems – at the moment – acquiescent towards the nuclear deal and willing to keep the Revolutionary Guards in check. The social and political context in Iran has evolved since the early 1980s, with women participating at most levels. However, the Revolutionary Guards remain vehemently ideologically opposed to the west and a political challenge for the country’s leadership. They are widely believed to have engineered Ahmadinajad’s electoral victory in 2009, and they control the Quds force which is thought to have links with Hezbollah, Syria’s Assad and possibly the Yemeni Houthis.

However, the Revolutionary Guards have also become a huge commercial entity within the country, a role which developed from their taking on infrastructure construction projects during the Iran-Iraq war. Since then, they are believed to have accumulated assets worth billions of dollars, including oil and gas, from key privatisations. Their revenue is now estimated at $100bn annually. Although they are likely to welcome foreign expertise that will boost oil and gas production, their presence in the economy and in politics will be a complicating factor for investors.

The Dove of Peace Monument in the colours of the Iranian flag stands on Imam Khomeini square in Tehran. (Source: Radiokafka/Dreamstime.com)

Challenges

Increases in oil production will inevitably bring Iran into conflict with OPEC quotas. Since last November, Saudi Arabia – the world’s ‘swing producer’ – has refused to reduce its production to help balance prices and it seems extremely unlikely that it will revise this policy in order to accommodate its much loathed Shia rival. Most members are in no financial position to cut production while the oil price – and therefore their revenues – are so low. It is hard to see how OPEC can continue as a cartel if it has lost the essential power to control production and fix prices.

President of Russia Vladimir Putin meeting with 7th President of Iran Hassan Rouhani, September 2013 (Source: Kremlin.ru)Many threats to the proposed agreement exist, but publicly Saudi Arabia’s reaction has been cautiously positive. US Secretary of State John Kerry clearly hopes that there will be a wider de-escalation of tensions in the Middle East, cooperation against ISIS and a solution to the Syrian conflict. Israel is looking increasingly isolated. Russia, which might have blocked an agreement for fear of lower oil prices, is onside and will play a key role in taking Iran’s excess uranium and processing it into fuel rods. The Chinese have offered to finance the Pakistani section of the much delayed ‘Peace Pipeline’ between Iran and Pakistan, and Tehran signed a gas supply agreement with Islamabad last December. Europe will be looking to benefit from gas supplies, via Turkey, that could lower its dependence on Russia.

President of Russia Vladimir Putin meeting with 7th President of Iran Hassan Rouhani, September 2013 (Source: Kremlin.ru)Many threats to the proposed agreement exist, but publicly Saudi Arabia’s reaction has been cautiously positive. US Secretary of State John Kerry clearly hopes that there will be a wider de-escalation of tensions in the Middle East, cooperation against ISIS and a solution to the Syrian conflict. Israel is looking increasingly isolated. Russia, which might have blocked an agreement for fear of lower oil prices, is onside and will play a key role in taking Iran’s excess uranium and processing it into fuel rods. The Chinese have offered to finance the Pakistani section of the much delayed ‘Peace Pipeline’ between Iran and Pakistan, and Tehran signed a gas supply agreement with Islamabad last December. Europe will be looking to benefit from gas supplies, via Turkey, that could lower its dependence on Russia.

Challenges remain however, in that although Rouhani appears unassailable from hardliners within Iran, this could change if he is unable to deliver economic benefits to the Iranian people. He is looking for a speedy lifting of sanctions. A more immediate threat comes from US Republicans threatening to pass legislation that will allow them to veto the deal. If the agreement holds, there will be a profound re-shaping of politics in the Middle East. The world, and particularly the oil industry, will be watching carefully.