The global energy sector from a subsurface perspective

The Karratha Gas Plant, North West Shelf Project, Western Australia. Australia is set to overtake Qatar by 2020 as the world’s largest supplier of LNG. Photo: Woodside Energy.

For an industry that is used to long-term contracts and guaranteed markets, changes in the gas market are proving unsettling. Will predictions of a future glut in liquefied natural gas prove premature?

Nikki Jones

The trade in liquefied natural gas (LNG) has risen almost without interruption for thirty years, doubling since 2000. However, 2012 saw an unexpected ‘blip’ in the upward trend and in 2013 investment in several major gas projects was delayed. The cause? The market is complex and changing, demand has become uncertain while supply is strong. The result is that analysts now appear divided on whether there will be a supply glut by the 2020s, or a supply shortage resulting from the current wait-and-see approach to long-term investment.

A Changing Market

Gas acquired a new status when the commodity super-cycle took off in the early 2000s. Companies began searching for the fuel in its own right, causing gas reserves to achieve parity with oil. Investment in infrastructure that can liquefy gas, transport it and regasify has allowed previously dis connected and remote reserves – notably in Australia, the Arctic and Africa – to be linked to markets. The high cost of such infrastructure has been justified by rising demand plus the industry convention of negotiating long-term bilateral contracts, indexed to oil, usually with at least 60% of production sold in advance.

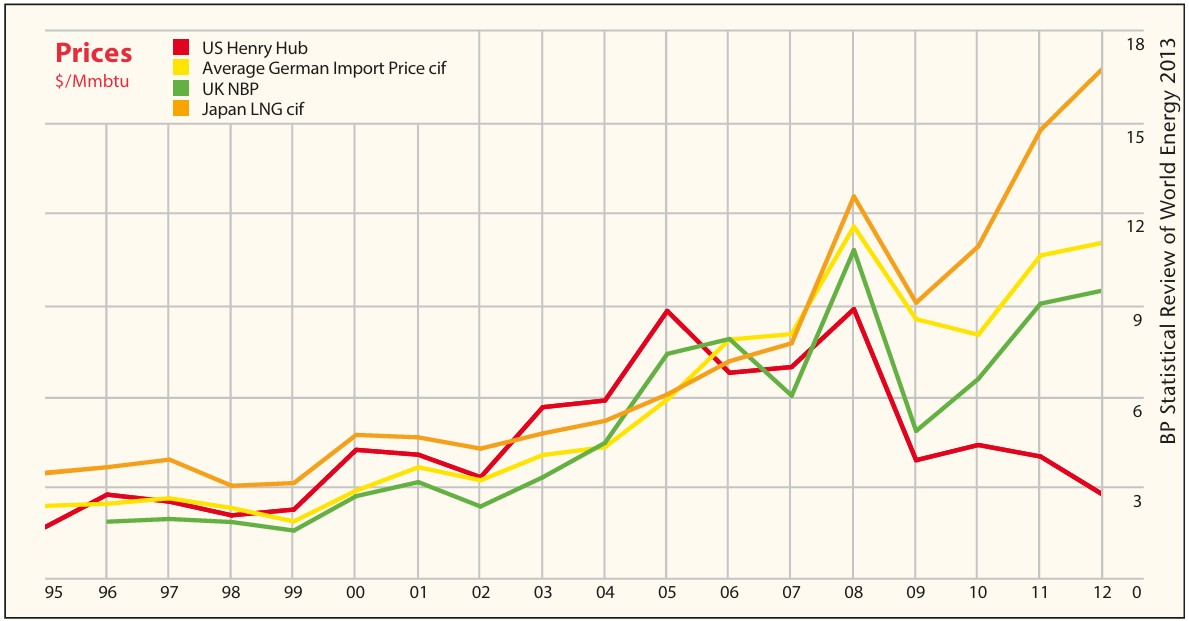

Changes in world gas prices since 1996 (in US$/mBtu).

However, a great deal of the early investment was based on an assumption that the US would be the primary market. It is almost humorous to remember now that, as late as 2003, the US Energy Department was predicting that the country would run out of domestic gas supplies within two decades, and Alan Greenspan was urging Congress to fast-track the construction of LNG import terminals. US shale production has, of course, completely reversed this scenario, with the US overtaking Russia to become the world’s biggest gas producer in 2010. In 2012, oversupply caused the Henry Hub benchmark to crash to a low of less than $2 per million British thermal unit (mBtu).

Suppliers have reacted by shifting their focus to East Asia – specifically to China which is expected to use at least 75% more energy than the US within 20 years and which doubled its gas consumption between 2007 and 2012, and to Japan, which became the highest importer of LNG following the Fukushima disaster of March 2011. However, both markets lack certainty: Japan’s imports of LNG are reported to have cost an unsustainable $33 billion in the first half of 2013, fuelling the government’s determination to return to nuclear power and to investigate further its own methane gas deposits; and China has its own shale reserves, estimated by the Energy Information Administration to be approximately 1.275 Tcfg. Although difficult geology, water shortages and lack of infrastructure appear to be hindering Chinese shale development, the possibility remains that global investments based on this one market may, as with the US, backfire. Gas is a small proportion of China’s current energy mix (approximately 11%) and given the country’s economic slow-down, its massive development of renewables and its reported reluctance to invest in gas turbines, there is room to doubt whether China will fulfil the potential envisaged by all its would-be suppliers.

Worldwide natural gas consumption increased by 2.2%, rising in every region except Europe and Eurasia; the US recorded the largest national increase, while EU consumption fell to the lowest level since 2000.

Sharp falls in demand in Europe are adding to the ‘buyer’s market’ scenario. Although the continent has been searching for alternatives to gas sourced from Russia and the North Sea, weak energy demand generally plus a move towards cheap coal and renewables has made it difficult to attract new investment for expensive infrastructure. Utility companies, which account for more than a third of gas demand, have been cancelling or delaying investment in gas-fired power plants, arguing that they need government guarantees to counter the low carbon price that has made coal particularly attractive, as well as subsidies for renewables. For LNG suppliers, the possibility that Europe will exploit its own shale reserves further complicates the investment picture, as do new pipelines bringing gas from the Caspian and possibly from the so-far unexploited deepwater finds in the Levantine Basin (GEO ExPro, Vol. 10, No. 3).

Lowering the Bar

For companies involved in exploiting expensive stranded reserves in Australia, Africa and the Arctic, among others, investment decisions have been further complicated by the question of whether the US will start to export its shale gas, not only increasing global supply but vastly under-cutting the typical Asian price of $15–18 mBtu and European price of $12 mBtu. Up until 2013, in order to keep domestic prices low and fuel its own economic recovery, the Obama administration had been holding back on export licences to any country with which it does not have an explicit free trade agreement. However, in late 2013 several licences were given consent with the potential that if all are granted, the US could be exporting over 40% of its production – more than 28 Bcfgpd. An example of an early deal that has lowered the bar for other purchasers is the contract agreed between the UK’s Centrica and Cheniere Energy in Louisiana – 89 Bcfg every year for 20 years at a fixed fee of $3 per mBtu plus 115% of the fluctuating Henry Hub price (currently less than $4 per mBtu). Asian buyers in particular are seeking similar deals.

Rig floor of a drillship exploring for gas off Mozambique. Photo: Anadarko Petroleum Corporation. .

Not only is US shale offering a particular ‘carrot’ to buyers but it has added impetus to calls for a more liberalised gas market, specifically a break with oil indexation and an end to ‘take or pay’ contracts that commit buyers to a certain quantity for years ahead. Statoil, which supplies much of northern Europe, has said that it expects 50% of European consumption to be priced off gas indices by the end of the year. Although at present LNG is still more likely to be indexed to oil, an LNG spot market is developing. With high price arbitrage across the globe, this is currently to the advantage of large producer-traders such as BP and Shell who find that trading can be more profitable than actual production. For example, cargoes originally bound for Europe can be diverted to higher paying Asian customers and cheaper supplies bought on the spot market to satisfy original customers. However, the lack of certainty is clearly a barrier to smaller upstream companies faced with high – and rising – capex; moreover, marked price arbitrage between Asia, America and Europe is unlikely to continue should the market become fully liberalised.

Feast or Famine?

Lack of security with regard to cost recovery is holding up investment. The nascent LNG spot market which by 2011 was accounting for a quarter of all supplies is now reported to have days with no trading at all. According to research by consultants Wood Mackenzie, the only LNG projects to reach Final Investment Decision (FID) in 2013 were all in the US and together they will only add 9 million tonnes per annum (mtpa) (86 MMboe) of LNG capacity, a notable slowdown from the 14.1 mtpa (134 MMboe) added in 2012 and the 26.8 mtpa (262 MMboe) in 2011. High among the postponements are the gasfields off the coasts of Mozambique and Tanzania, additional trains from Australia, and Chevron’s Kitimat export facility on the west coast of Canada. Despite several years of impressive gas finds it seems that predictions of a 2020s global gas glut may have been premature: too many market uncertainties prevail.

Qatar – Biggest Supplier of LNG

Since 2006 Qatar has been the world’s biggest supplier of LNG – by a very wide margin. Qatari annual exports of almost 80 million tonnes (mt) (764 MMboe) dwarf those of its nearest competitor, Malaysia, with its mere 23 mt (217 MMboe). However, Australia is set to overtake Qatar by 2020 and although currently secure in its long-term contracts, Qatar is unlikely to be able to re-negotiate them on the same terms in the future.

Pearl GTL plant at night. This is one of the largest and most sophisticated plants ever built in the energy industry. Source: Shell.com.

Qatar’s massive wealth – it has the world’s highest per capita income – comes from the ‘North Field’, the world’s biggest gas reserve, a 9,700 km2 offshore structure shared with Iran. Although Qatar ranks twelfth in terms of world oil reserves, these are declining. Since 2005 there has been a moratorium on further development of the North Field in order to prevent damage, but exploration has continued and a significant new find (544 km2) was announced in 2013. Although Qatar only began gas production in 1991 and LNG exports in 1997, the country has moved fast to develop several gas-related industries such as petrochemicals and aluminium production. Qatar also produces 140,000 b/d of gas-to-liquid products at its Shell-built GTL plant, the world’s largest. Qatar has had to adapt fast to the loss of the US as its main market. Most of its long-term contracts are now with East Asian and some European buyers. These appear to be cushioning the state from current upheavals in the market but even Qatar will not be immune to market uncertainties, including the move away from fixed term contracts towards a liberalised spot market.

However, Qatar has been using its wealth to diversify its economy and invest in human capital projects at home, as well as buy its way to a new international status with a highly independent foreign policy. Qatar has come to the world’s attention, not just through Al Jazeera, its support for Libyan and Syrian rebels and its provision of a base for the US Central Command – all while maintaining good relations with Iran – but also through the deployment of its massive cash surplus, via its highly active sovereign wealth fund, into infrastructure projects and banking in the Global North. In a further attempt to diversify its economy, in 2013 the Qatari stock exchange was upgraded to ‘emerging market’ status, a move expected to attract in capital flows of approximately $430m. Whether such developments will adequately insulate Qatar from its dependence on LNG is unclear but, in the short term, there appear to be few clouds on the Qatari horizon.