Farm-in: a bad choice?

The commercial success rate for farm-in exploration wells is lower than for wells that were not farmed out according to a study from Westwood Global Energy.

David Moseley from Westwood Global Energy presented insights on NW Europe exploration drilling and farm-in performance at Prospex in London.

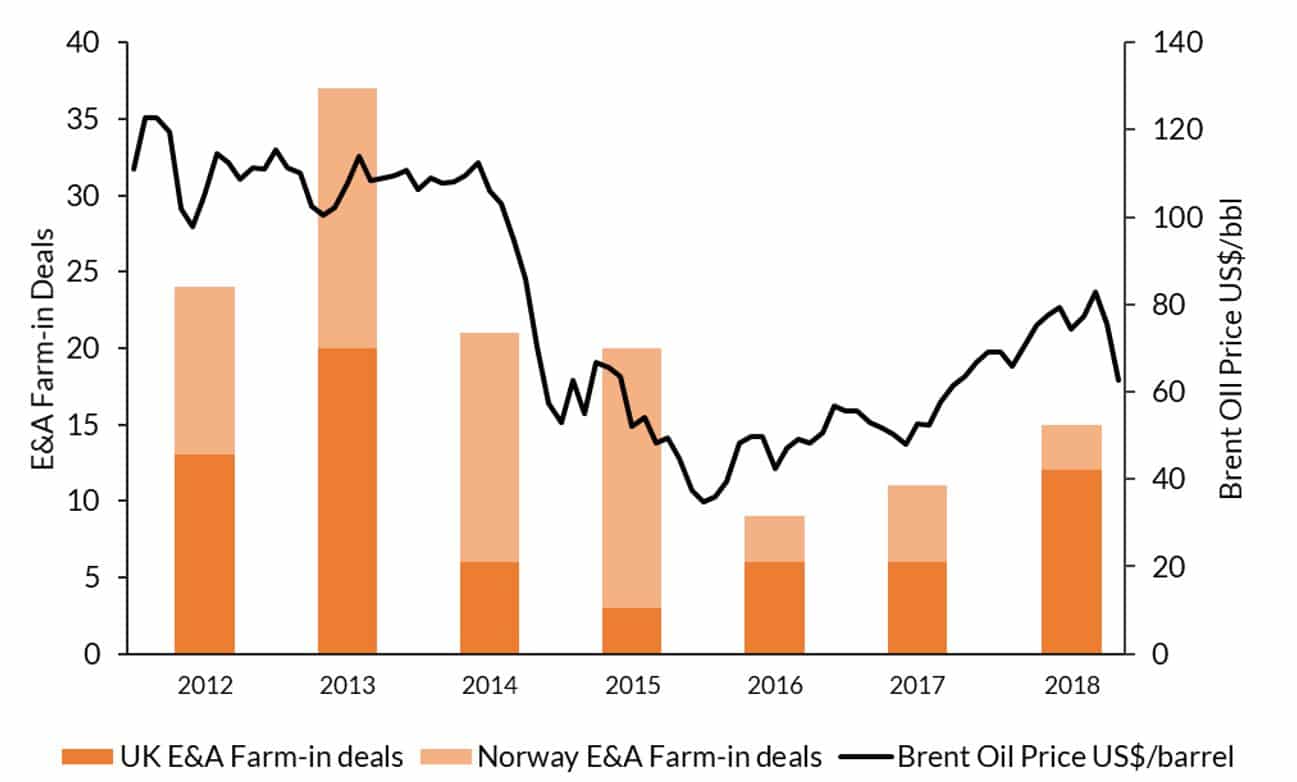

The farm-in market is recovering but Norway seems slower to respond to the oil price (see figure above). In the period from 2012 to 2018, 140 farm-in deals were signed in Norway and UK together. Almost half of them dated from 2012 and 2013 before the oil price crash. 124 of these deals were exploration focused and resulted in 60 exploration wells. The wells with a least one farm-in partner represented 20% of all the exploration wells.

The exploration farm-in performance is quite poor in the UK. Only 2 out of 20 exploration farm-in wells (out of 53 farm-in deals) resulted in a commercial discovery. The CSR of 10% is much lower than the 25% CSR of wells that were not farmed out during the same period.

Norway has performed better with a CSR of 15% for farm-wells versus 19% for wells that not have been farmed out. Out of 69 farm-in exploration deals, 40 exploration wells were drilled resulting in 6 commercial discoveries.

So why do we see these differences in numbers of farm-in deals and especially in performance between Norway and the UK? The higher amount of farm-in deals going on in the UK could be related to the need to farm-out with small companies on the UKCS often starting off with high working interests and needing to farm down to be able to fund the exploration drilling costs.

The lower CSR for farm-in wells in the UK, compared to Norway is not so easy to understand. It must be noted that the dataset of commercial discoveries from farm-in drilling is very small and it would only take a couple of new discoveries from farm-in wells to boost the performance.

David Moseley explains in more detail:

“There are likely to be several factors controlling farm-in drilling performance. Initial analysis shows that of the 13 exploration farm-in wells that were drilled in the U.K. and abandoned as dry holes, seven (54%) were firm commitments. Initial thoughts suggest that being required to drill a well (as opposed to choosing to do so) could have impacted performance. Especially if wells are getting drilled simply because companies are required to do so to honour licence commitments, rather than based on robust prospects… and if these represent a large portion of the available opportunities, then this could be reducing the quality of the farm-in market, and by extension subsequent farm-in drilling performance. Another consideration is the fact that companies may tend toward farming-out the riskier prospects, and so by extension the farm-in market is dominated by wells targeting higher risk prospects.”