A new cycle of exploration

In the North Sea mergers and acquisitions (M&A) market, the window to buy assets at the bottom of the market is closing. There are fewer obvious sellers and the firesales are over. So creating value in the current M&A market is going to be challenging, writes Wood Mackenzie.

On the other hand, exploration is showing signs of a recovery.

According to Wood Mackenzie, the conditions are in place to fuel a recovery in exploration:

First, the economics of exploration have been broken in recent times. A mixture of high costs, low oil prices and underperformance destroyed value. But figures for 2017 are starting to show a return to profitability.

Second, looking at volumes discovered globally, if we factor an average resource creep of 40% onto the 2017 results, we would find that it’s been the best performing year since 2011 in terms of volume per well, and potentially the best since 2008 in terms of discovery costs.

As for UK and Norway, 60 exploration wells were drilled across the UK and Norway in 2013. The oil price was high and the sector was booming. But since then, it’s seen smaller discoveries and declining returns.

But the conditions are right to fuel a recovery, Wood Mackenzie says.

Appetite for risk

Lead times have reduced and costs have diminished through lower rates in the supply chain, improved efficiencies and a new approach to projects.

We are starting to see early signs of a return to high impact exploration as companies increase their appetite for risk.

This is not just more wells in emerging basins, but also new ideas with frontier plays in mature basins.

While there are several good examples of successful near-field exploration, high-impact frontier wells are the ones that move the needle.

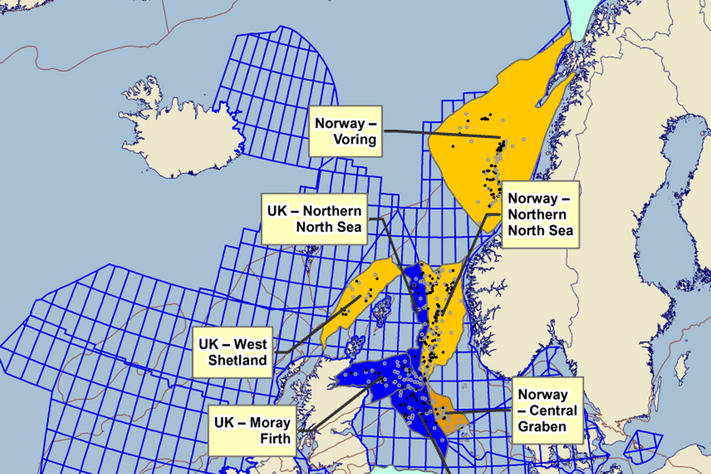

Where is the best place to explore in the North Sea?

Wood Mackenzie has benchmarked the top nine basins in Norway and the UK by their value creation per barrel of oil equivalent prospective resource.

This metric combines a view of the prospectivity of plays in a basin with their potential to create value through exploration.

The map shows value creation per boe overlaid with the location of exploration wells drilled since 2008 in their PetroView product.

This analysis shows that considerable potential remains to create exploration value, even in well-explored basins. The impact of the lower government take in the UK fiscal regime can be seen in the higher potential value creation per barrel in its mature North Sea basins.

Whether an acquisition or an exploration strategy makes sense for individual companies will depend on their expertise and end goals. In reality, a mixture of both will likely be the best strategy, concludes Wood Mackenzie.